The Surat bench of the Income Tax Appellate Tribunal (ITAT) said that the late filing of the audit report in Form No. 10B is not a valid ground to refuse the exemption u/s 11/12 of the Income Tax Act, 1961.

The taxpayer, SUD Education Trust, a public charitable/religious trust registered under section 12AB of the Income Tax Act, submitted its return for AY 2022-23 within the extended deadline, claiming exemption under Sections 11/12 of the Income Tax Act.

However, the audit report in Form 10B was submitted after the mentioned deadline; it was filed before the AO processed the return u/s 143(1) of the Income Tax Act. The AO did not accept the exemption because of the late filing of Form 10B, and the CIT(A) maintained the disallowance.

The problem before the Tribunal was whether the taxpayer remained qualified for exemption under Sections 11/12 of the Income Tax Act even after submitting Form 10B after the deadline but before processing the return.

The taxpayer’s representative argued that the taxpayer should not be denied the legitimate exemption u/s 11/12 of the Income Tax Act, especially since they are genuinely engaged in charitable and religious activities for the welfare of the public.

The taxpayer meets all the conditions required by the income tax law to qualify for this exemption. It was further stated that if the audit report in Form No. 10B, which was submitted by the taxpayer on 02, 11, 2022, is considered, the taxpayer will be eligible for the claimed exemption.

The counsel placed reliance on specific decisions of the High Courts and ITAT Benches wherein it has been stated that the requirement of filing an audit report in time is one of the conditions to avail the benefit of exemption u/s 11/12, but it is a procedural-cum-directory requirement and even if the report is belatedly submitted to the AO, the exemption u/s 11/12 of the Income Tax Act can’t be refused.

The Departmental Representative for the revenue said that the filing of the audit report in Form No. 108 by the deadline is a pre-condition for the allowability of exemption u/s 11/12 of the Income Tax Act. As the taxpayer has not satisfied these conditions, the AO has correctly rejected the taxpayer’s claim of exemption u/s 11/12 of the Income Tax Act.

Also Read: New Audit Report Forms 10B & 10BB for Several Institutions

The Tribunal of Suchitra Kamble, Judicial Member, and B.M. Biyani, Accountant Member, observed that “The delayed filing of the audit report is a mere procedural irregularity, and exemption under Sections 11/12 cannot be denied on this ground. Recently, in CIT (Exemption) vs. Anjana Foundation, the Supreme Court dismissed the Revenue’s SLP and upheld the view that exemption under Sections 11/12 cannot be denied for non-filing of the audit report within the prescribed time.”

The bench concluded, “Hence, in view of above discussions and for the reasoning mentioned therein, the assessee cannot be denied benefit of exemption under Section 11/12 as claimed in return for mere delay in filing of audit report in Form No. 10B. In that view of the situation, we remand this matter back to the file of AO for a fresh assessment after accepting the audit-report filed by assessee, in accordance with law.”

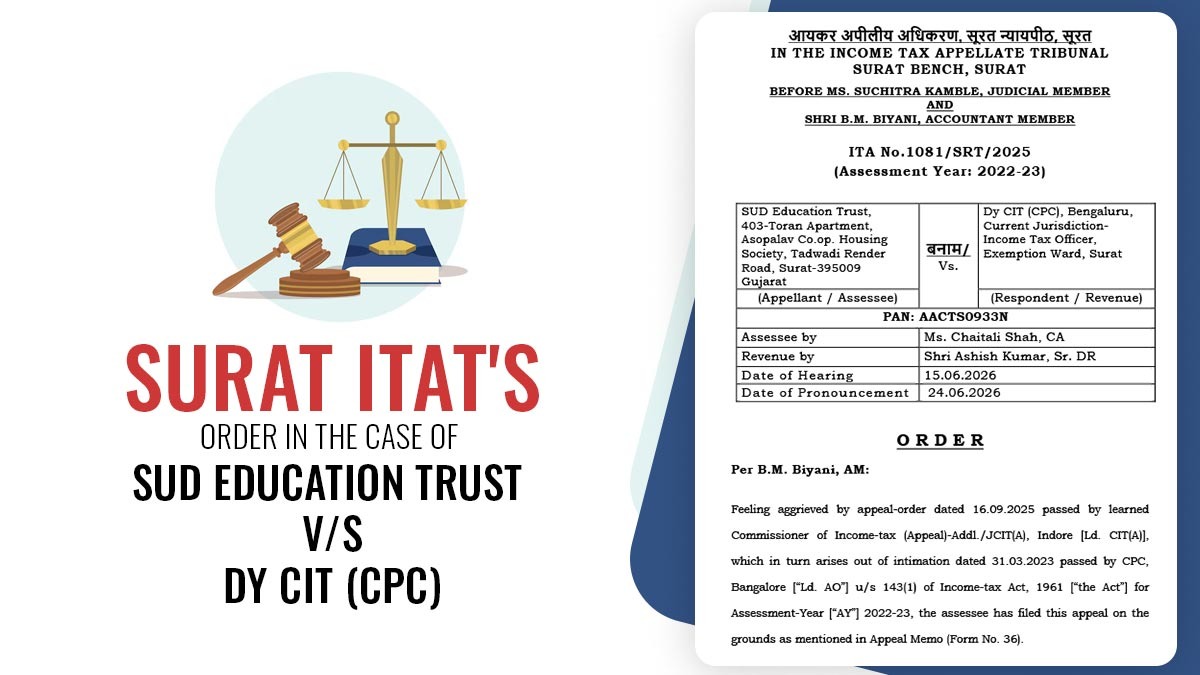

| Case Title | SUD Education Trust Vs. Dy CIT (CPC) |

| Case No. | ITA No.1081/SRT/2025 |

| Counsel For Appellant | Ms Chaitali Shah |

| Counsel For Respondent | Shri Ashish Kumar |

| Surat ITAT | Read Order |