In the questionnaire, it is revealed that the Gujarat government has received more income in terms of indirect taxes after GST implementation.

Powerd By SAG INFOTECH

Notifications can be turned of anytime from browser settings

In the questionnaire, it is revealed that the Gujarat government has received more income in terms of indirect taxes after GST implementation.

In a recent crackdown on the taxpayers for not paying their advance taxes, the tax department had been issuing notices to the defaulting taxpayers and also seeming to take strict actions against them.

Finance Minister Capt Abhimanyu didn’t force any new tax in Haryana’s financial plan. The foremost purpose behind this is the number of income from Haryana’s Goods and Services Tax (GST). After the implementation of GST, Haryana has established a record achievement in the country.

With the implementation of GST, the senior citizens or elderly population of the country are facing additional burden, who is disabled due to advancing age or any other problem and are living in retirement community centres.

The government has finally decided that transaction credit can be claimed by individual firms, after getting criticised by two high courts over the GST working portal

The restaurant industry in Mumbai and Bengaluru feels good after the implementation of Goods and Services Tax (GST) and has been largely positive.

The Income Tax laws in India are very complex. In the last couple of years, passive incomes from freelancing jobs have gained momentum.

Recently the 25th GST council meeting took some better decisions regarding the issues struck regarding various industry of India. Now there is some good news for the home buyers as the government has decided lesser GST on the home which is purchased under the Credit-Linked Subsidy Scheme (CLSS).

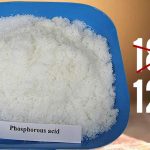

According to ICRA rating agency, the fertilizer manufacturers are likely to be benefited with the reduction in tax rates under the GST as the tax rates on phosphorus acid reduced from 18 percent to 12 percent.