It is the moral duty of every organisation and taxpayer to file an income tax return and pay the taxes. The budget 2020 income tax amendments have stated that the ITR is important to be filed in case the electricity bill is more than 1 lakh and more than 2 lakh for foreign travel expenses.

The income tax return form 7 is to be filed by all the Charitable /Religious trusts u/s 139 (4A), Political party u/s 139 (4B), Scientific research institutions u/s 139 (4C), University or Colleges or Institutions or Khadi and Village industries u/s 139 (4D). These organisations have to file the form for claiming the exemptions.

Latest Update

- The Excel-based utility, JSON schema, and validation files for the ITR-7 form are now available. Download Now

Gen IT Software Free Demo for Filing ITR-7

What is ITR 7 Form?

The Firms, Companies, Local authority, Association of Person (AOP) and Artificial Judiciary Person are eligible for filing Income Tax Return through ITR-7 Form if they are claiming exemption as one of the following categories:

- Under Section 139 (4A)- if they earn from a charitable /religious trust

- Under Section 139 (4B)- if they earn from a political party

- Under Section 139 (4C)- if they earn from scientific research institutions

- Under Section 139 (4D)- if they earn from universities or colleges or institutions or khadi and village industries

Who are Not Eligible to File ITR 7 Form Online?

Taxpayers who are not claiming exemption under Section 139 (4A), Section 139 (4B), Section 139 (4C) or Section 139 (4D) are not liable to file ITR 7 Form for Income Tax Return.

Who is Eligible to File the ITR-7 Form?

- Return under section 139 (4A), filing. Every person in receipt of income derived from property held under trust or other legal obligation wholly for charitable or religious purposes or in part only for such purposes, or of income being voluntary contributions, if the total income in respect of which he is assessable as a representative assessee exceeds the maximum amount which is not chargeable to income-tax

- Return under section 139 (4B), a political party is required to fill out the form in case the income exceeds the maximum amount not chargeable to tax.

- Return under section 139 (4C) is filled by some organisations such as :

- Scientific Research Association ;

- Hospital, Fund, Any Educational Institution or University;

- Association or Institution Referred to in Section 10 (23A);

- News Agency ;

- Institution Referred to in Section 10 (23B);

- Return under section 139(4D), every college or University that is not required to furnish the return of income or loss

- Return under section 139(4D), every college or University is required to fill which who is unable not required to furnish the income tax return or loss under any other provision of this section

- Return under section 139 (4E), Every business trust, which is not required to furnish a return of income or loss under any other provisions of this section, shall furnish the return of its income in respect of its income or loss in every previous year and all the provisions of this Act shall, so far as may be, apply *_ if it were a return required to be furnished

under sub-section (1). - Return under section 139 (4F), Every investment fund referred to in section 115UB, which is not required to furnish a return of income or loss under any other provisions of this section, shall furnish the return of income in respect of its income or loss in every previous year and all the provisions of this Act shall, so far as may be, apply as if it were a return required to be furnished under sub-section (1).

Any taxpayer can use the ITR-7 Form for filing Income Tax Returns if they file as a Trust, Company, Firm, Local authority, Association of Person (AOP) or Artificial Judicial Person and claims exemption under Section 139 (4A), Section 139 (4B), Section 139 (4C)or Section 139 (4D).

What is the Last Date for Filing ITR 7 Form?

The due date for filing the ITR-7 form varies depending on the audit of the accounts. Tax assesses whose accounts are not required to be audited can file till 31st July 2026 for AY 2026-27, while for audit cases, the due date is 31st October 2026.

Read Also: Penalties for Late Income Tax Return Filing in India

Note: ITR-7 form corrigendum via Notification No. 62/2026. Read More

Know the Steps to File ITR 7 Online

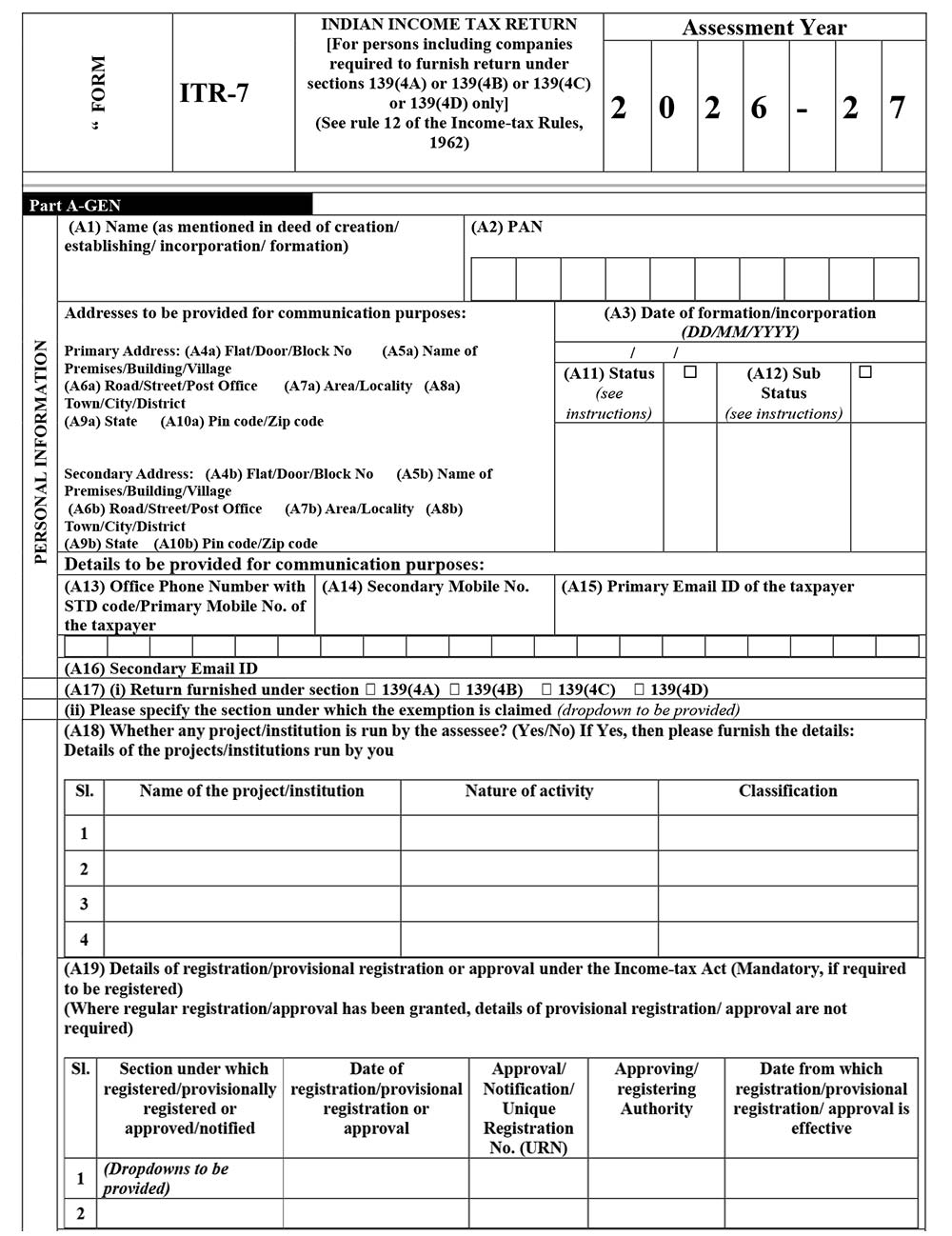

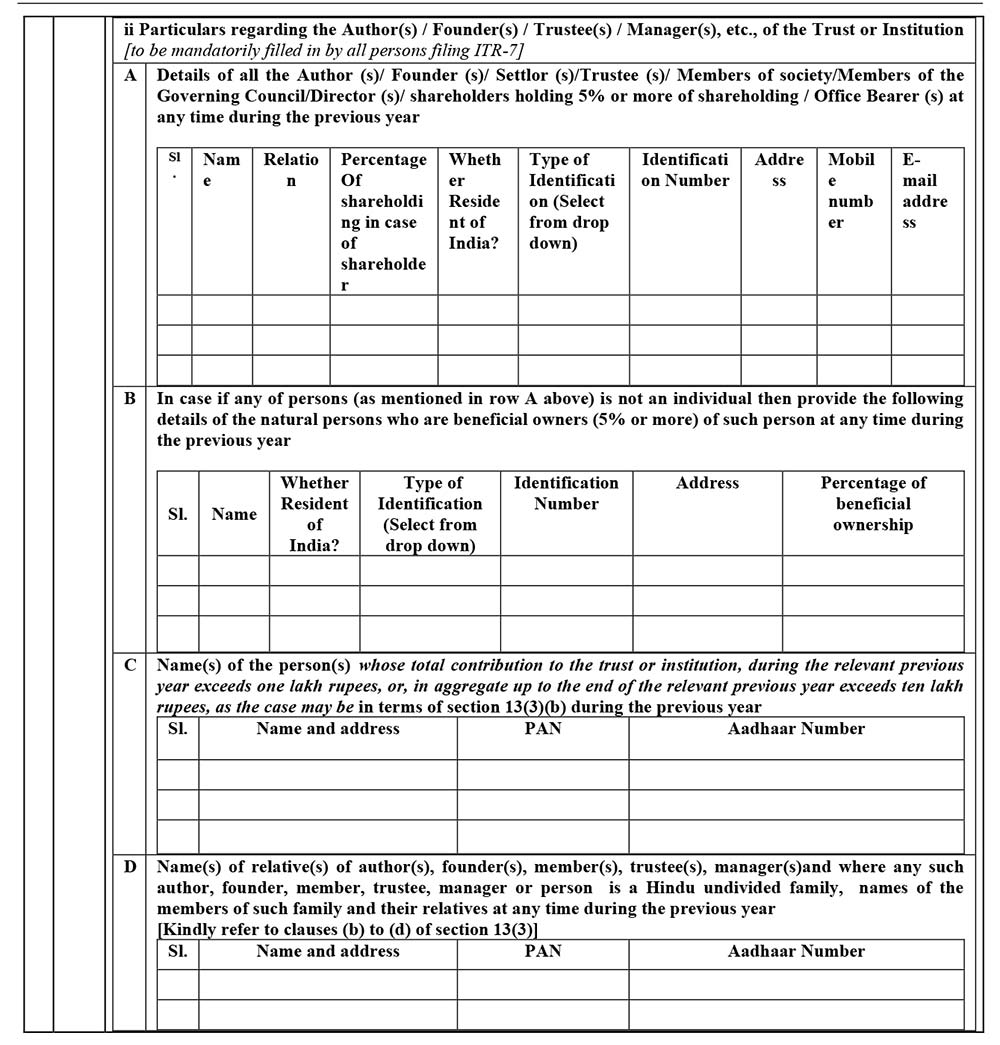

Part A-GEN

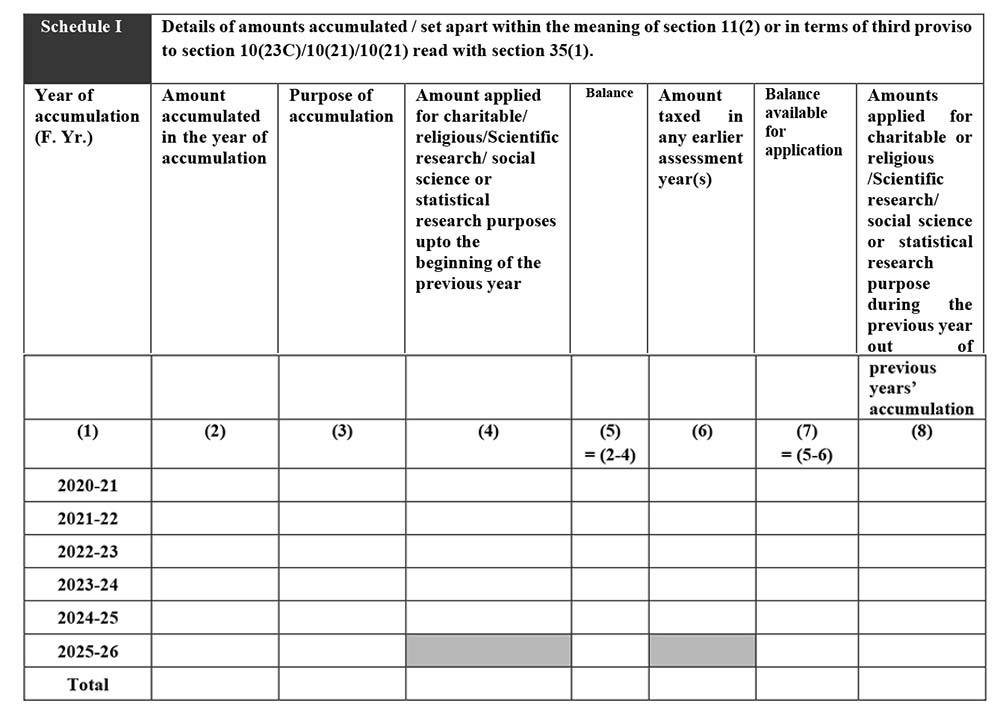

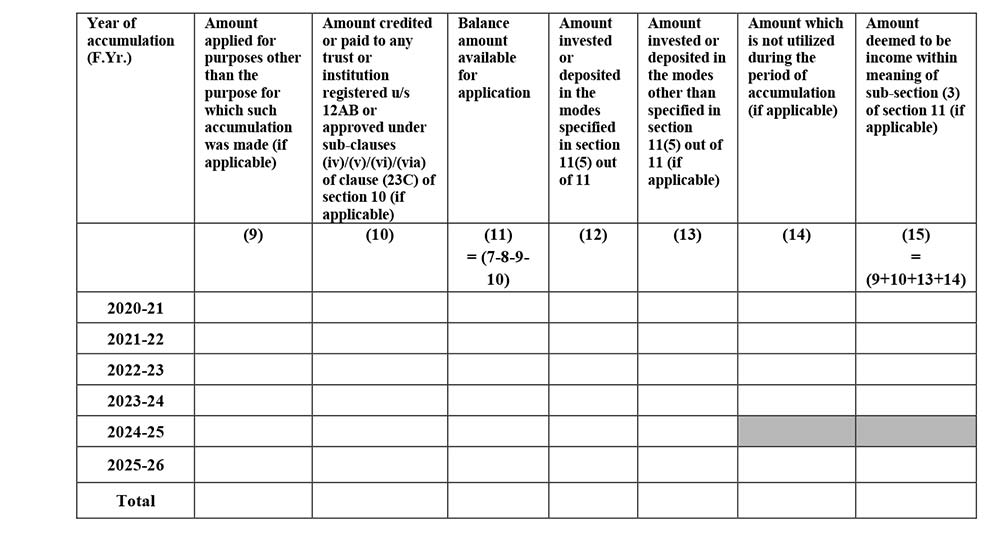

Schedule I

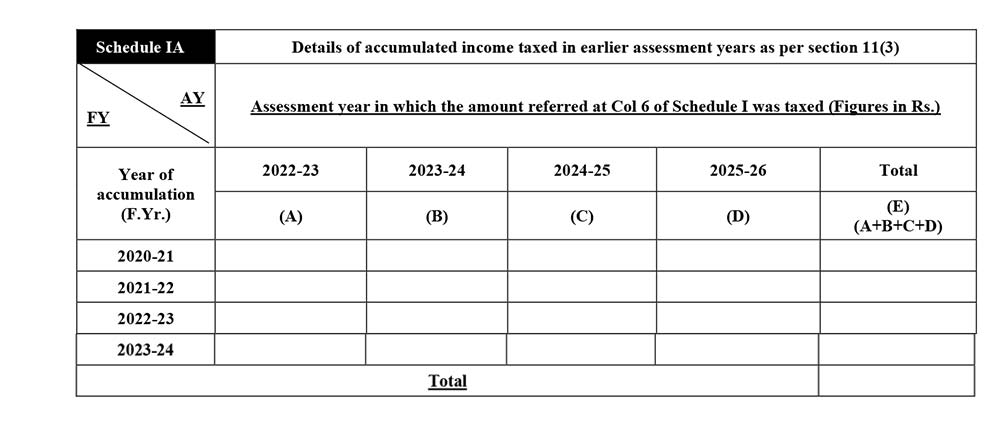

Schedule IA

Schedule D

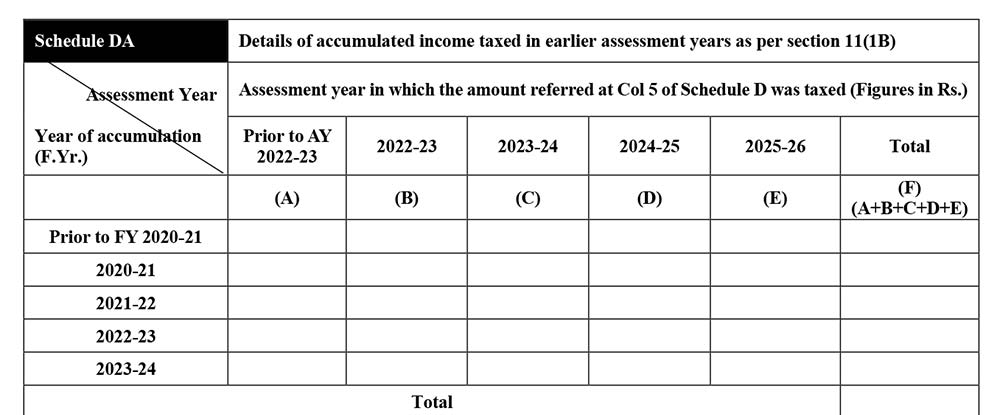

Schedule DA

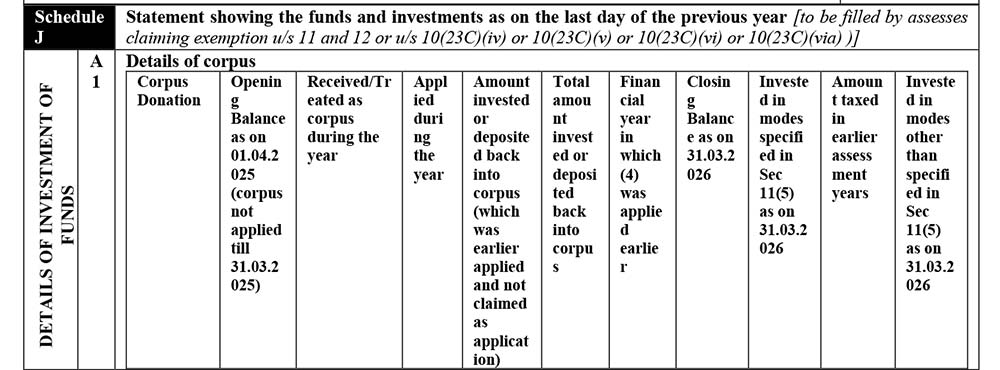

Schedule J

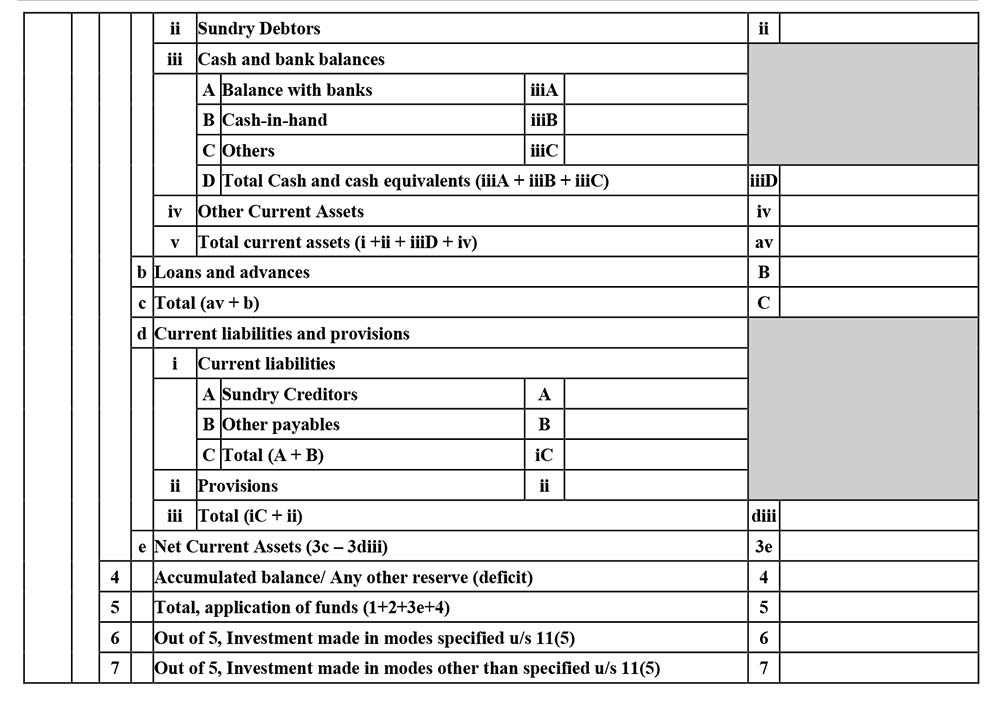

Part-A BS

Schedule R

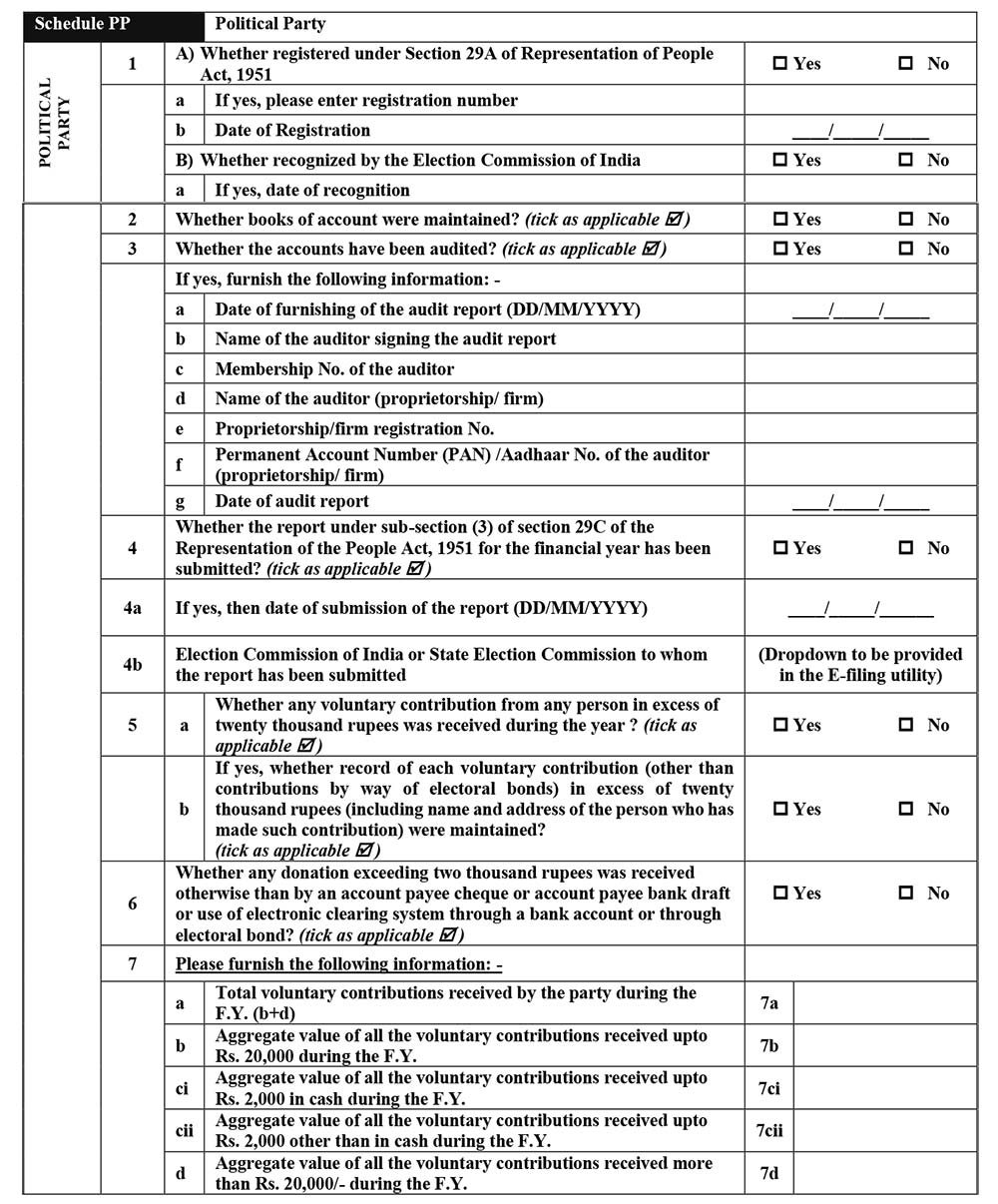

Schedule PP

Schedule ET

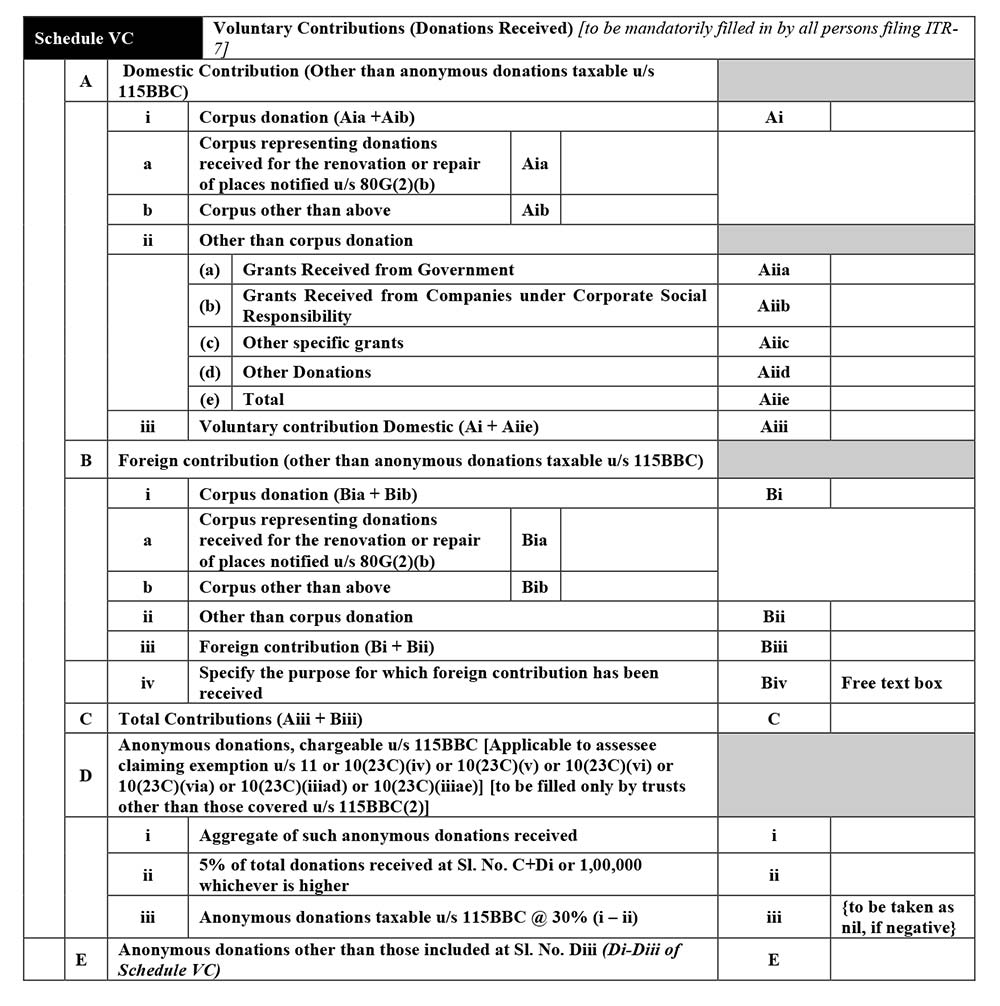

Schedule VC

Schedule AI

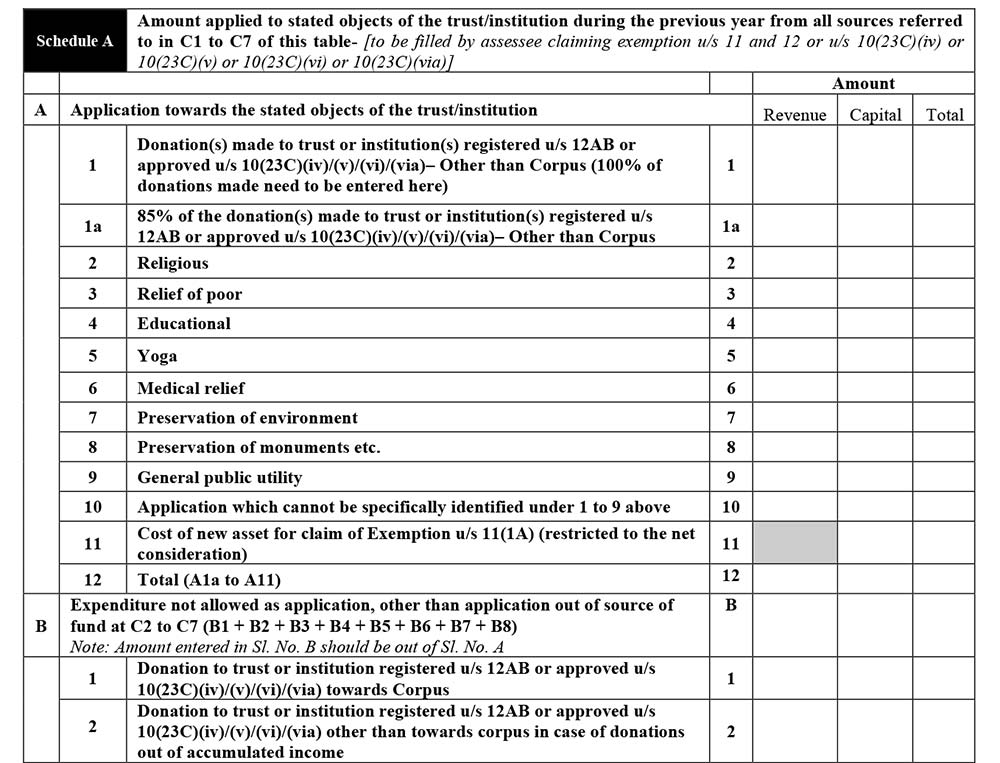

Schedule A

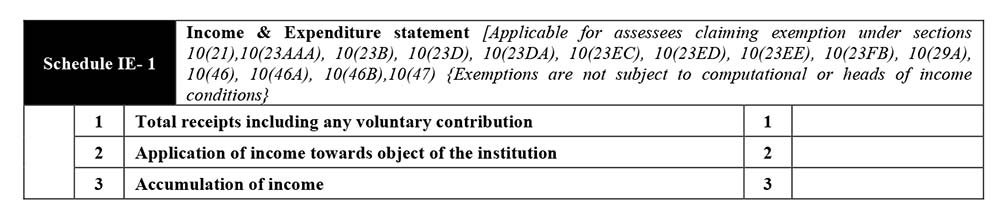

ITR-7 Form Schedule IE-1

ITR-7 Form Schedule IE-2

ITR-7 Form Schedule IE-3

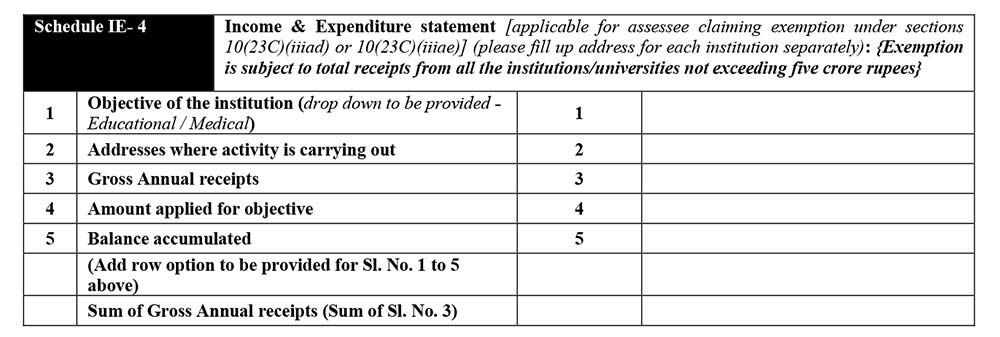

ITR-7 Form Schedule IE-4

Schedule HP

Schedule CG

A. Short-term Capital Gains

B. Long-term Capital Gain

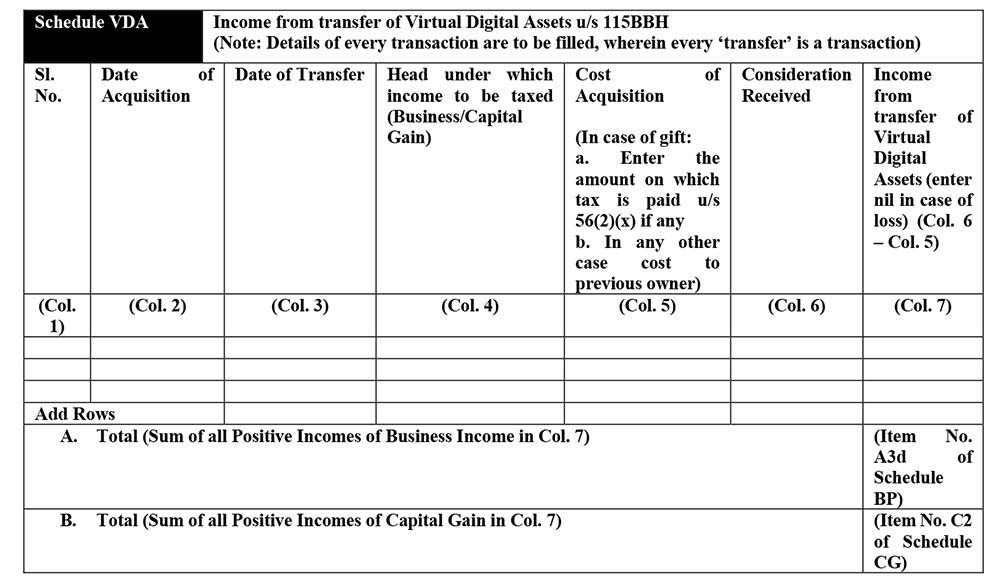

Schedule VDA

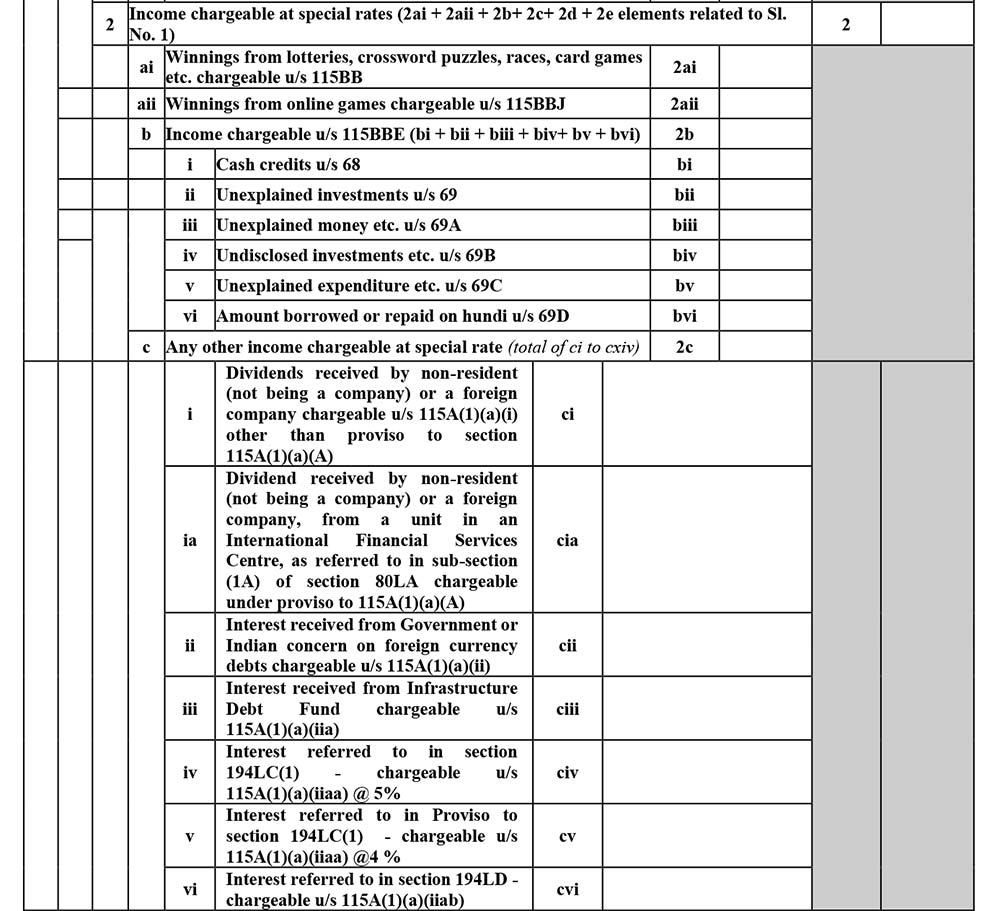

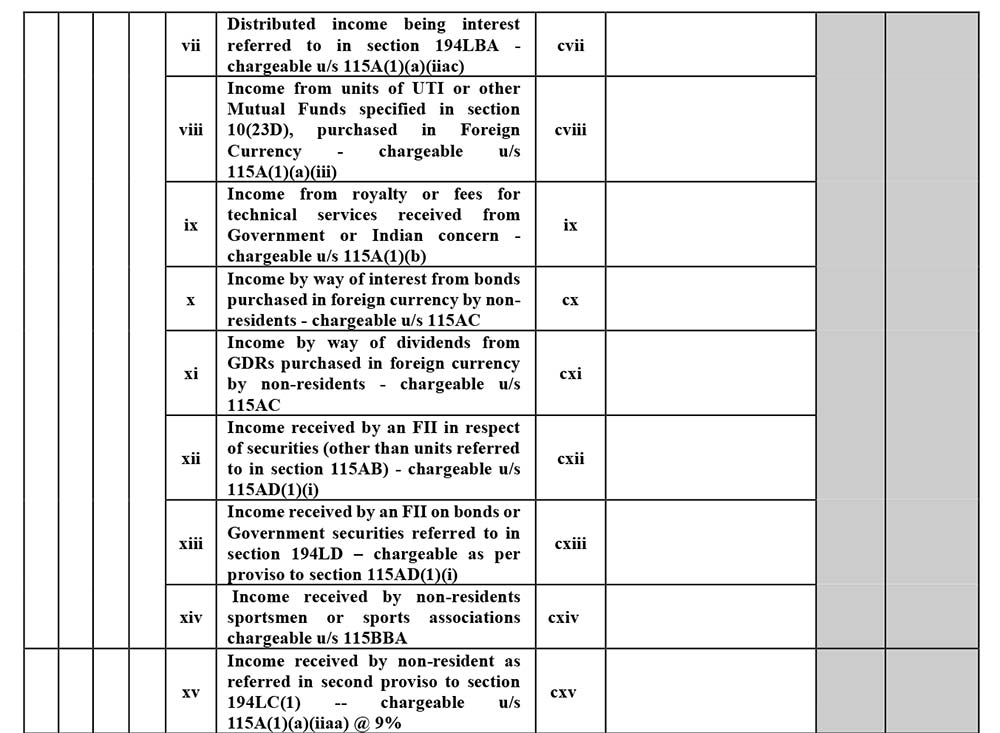

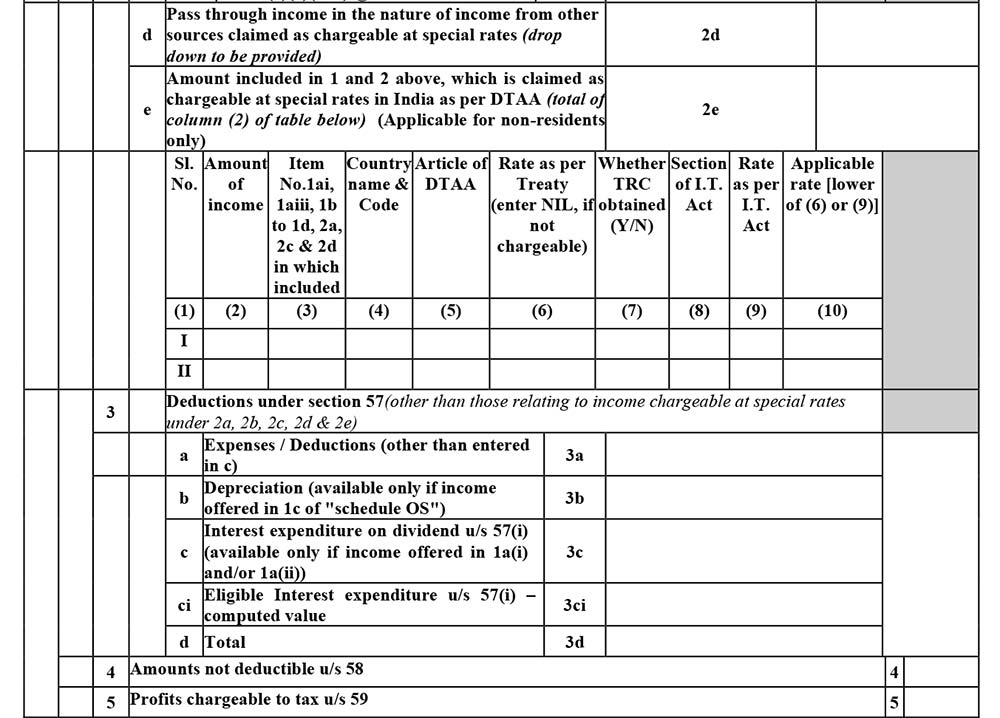

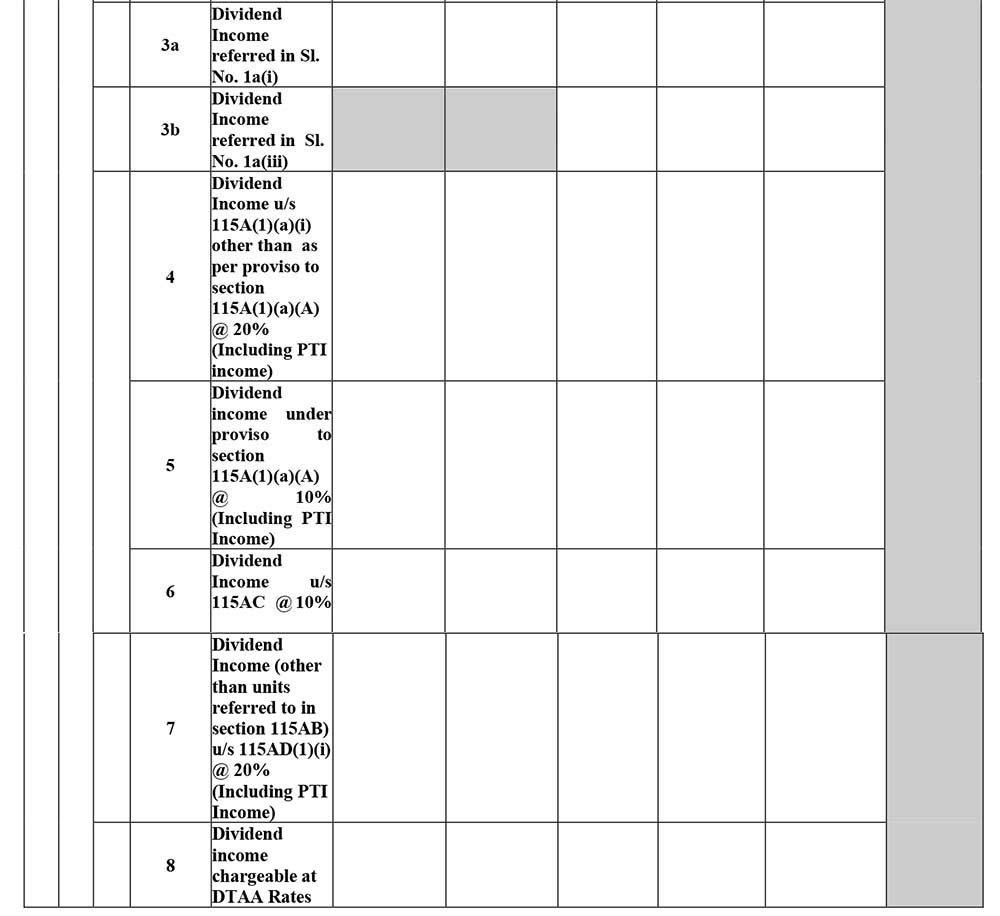

Schedule OS

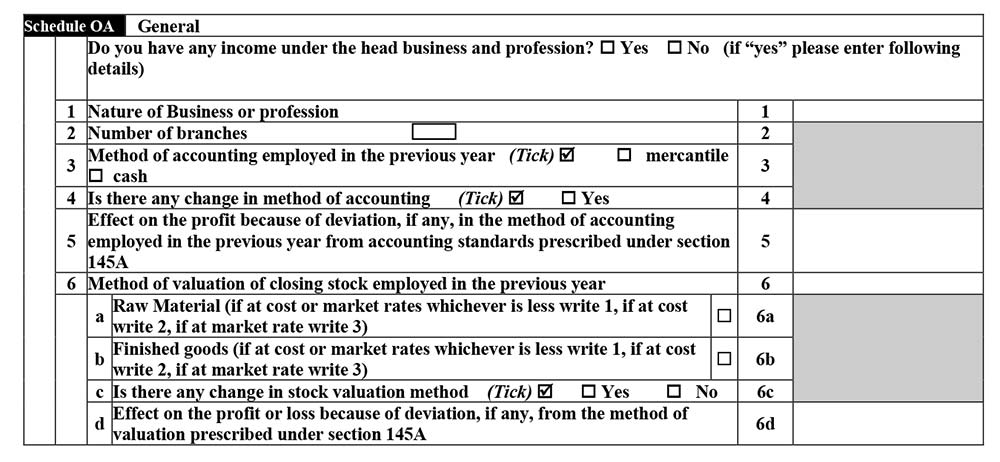

Schedule OA

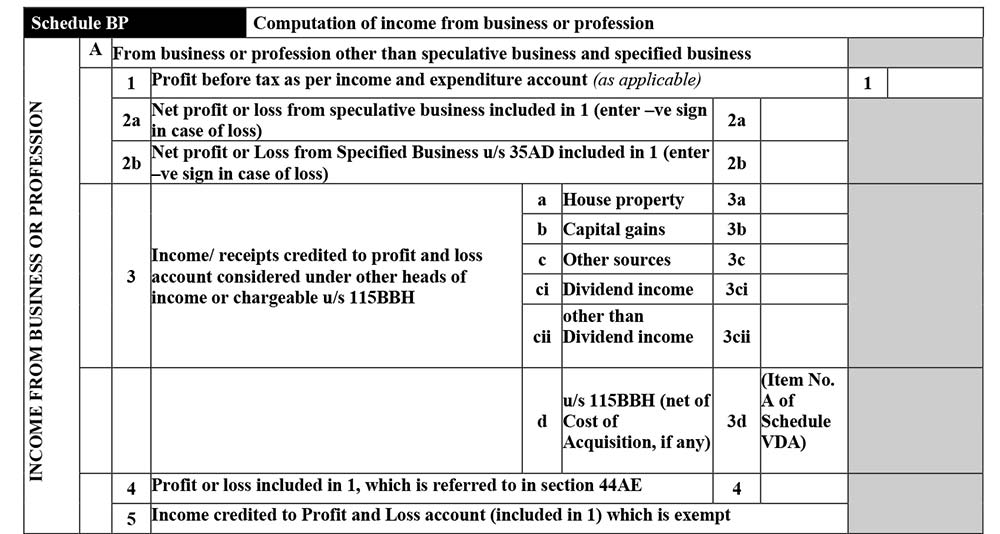

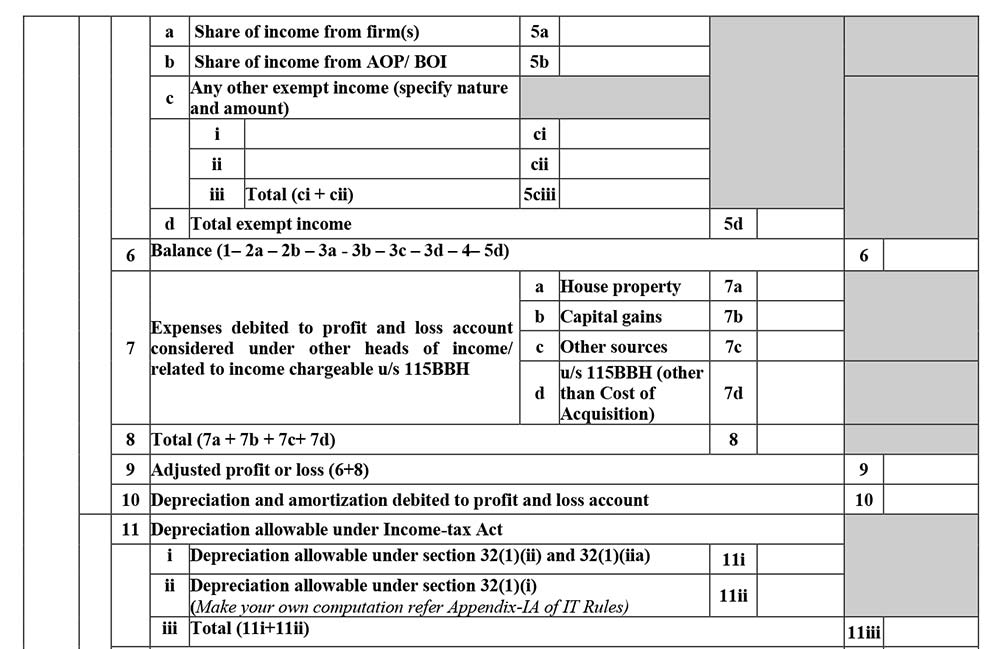

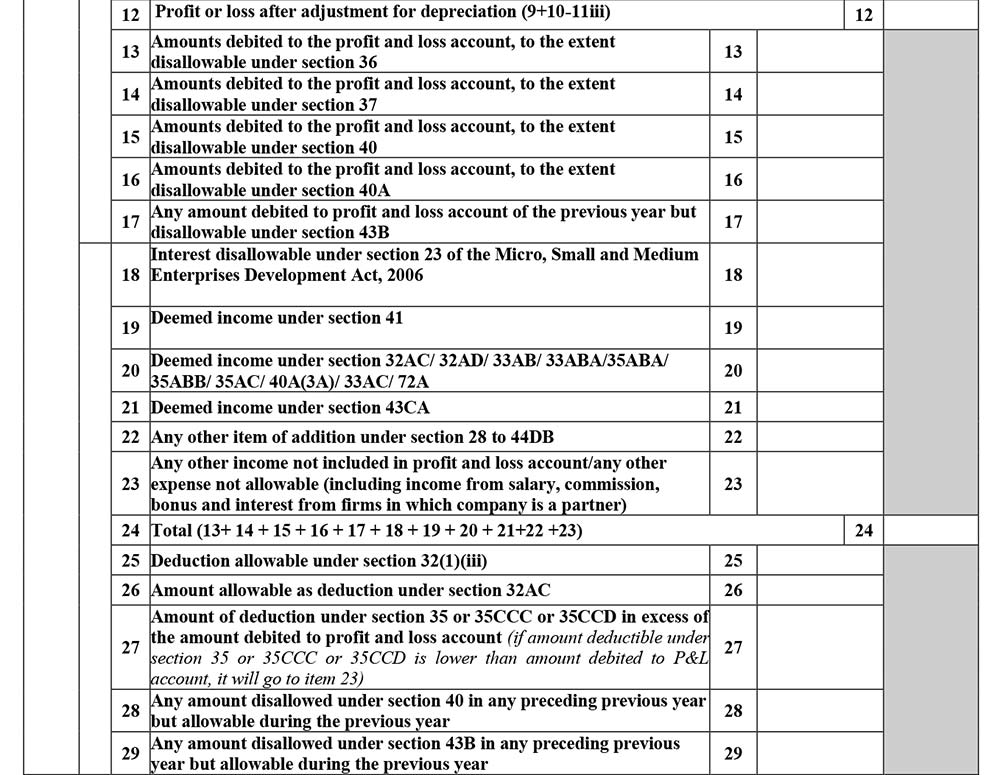

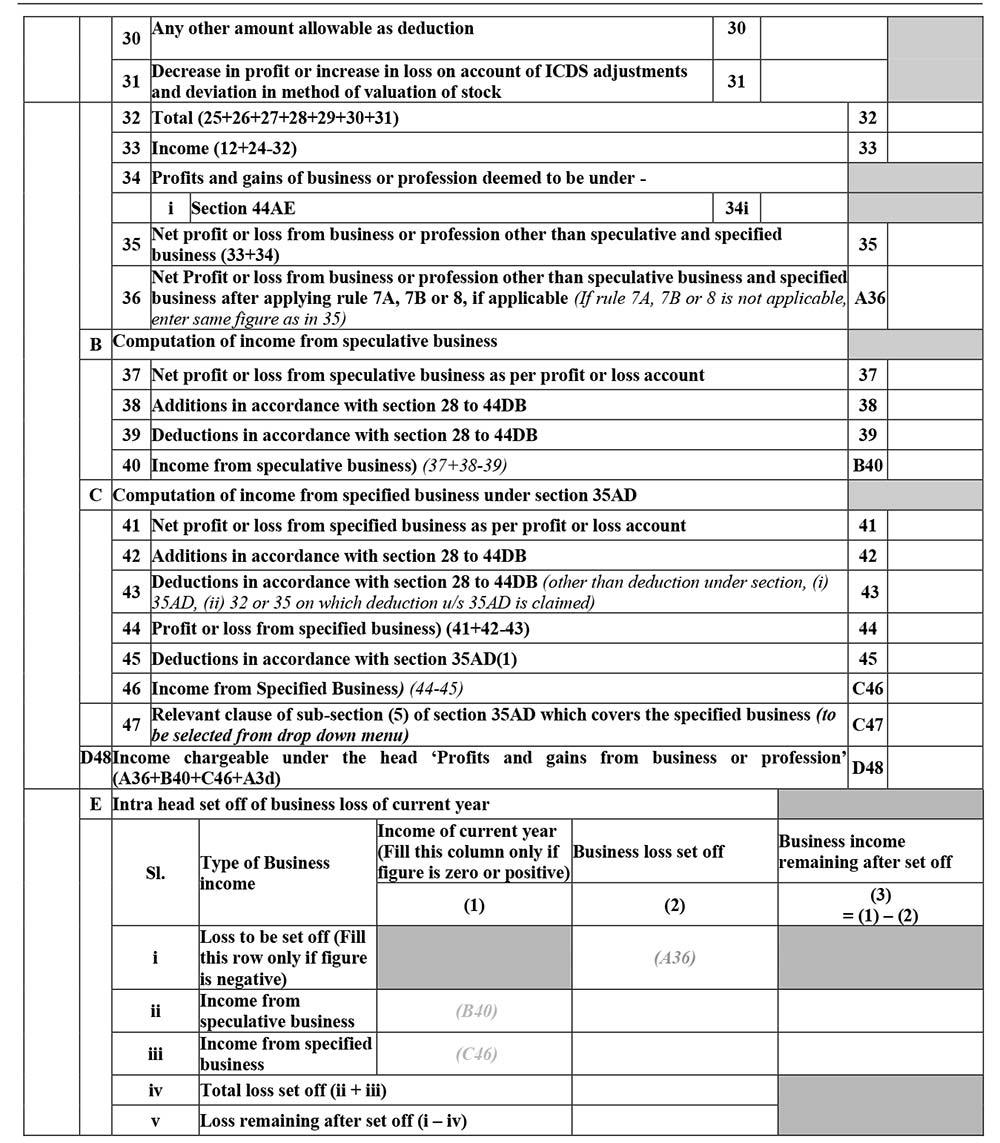

Schedule BP

Schedule CYLA

Schedule PTI

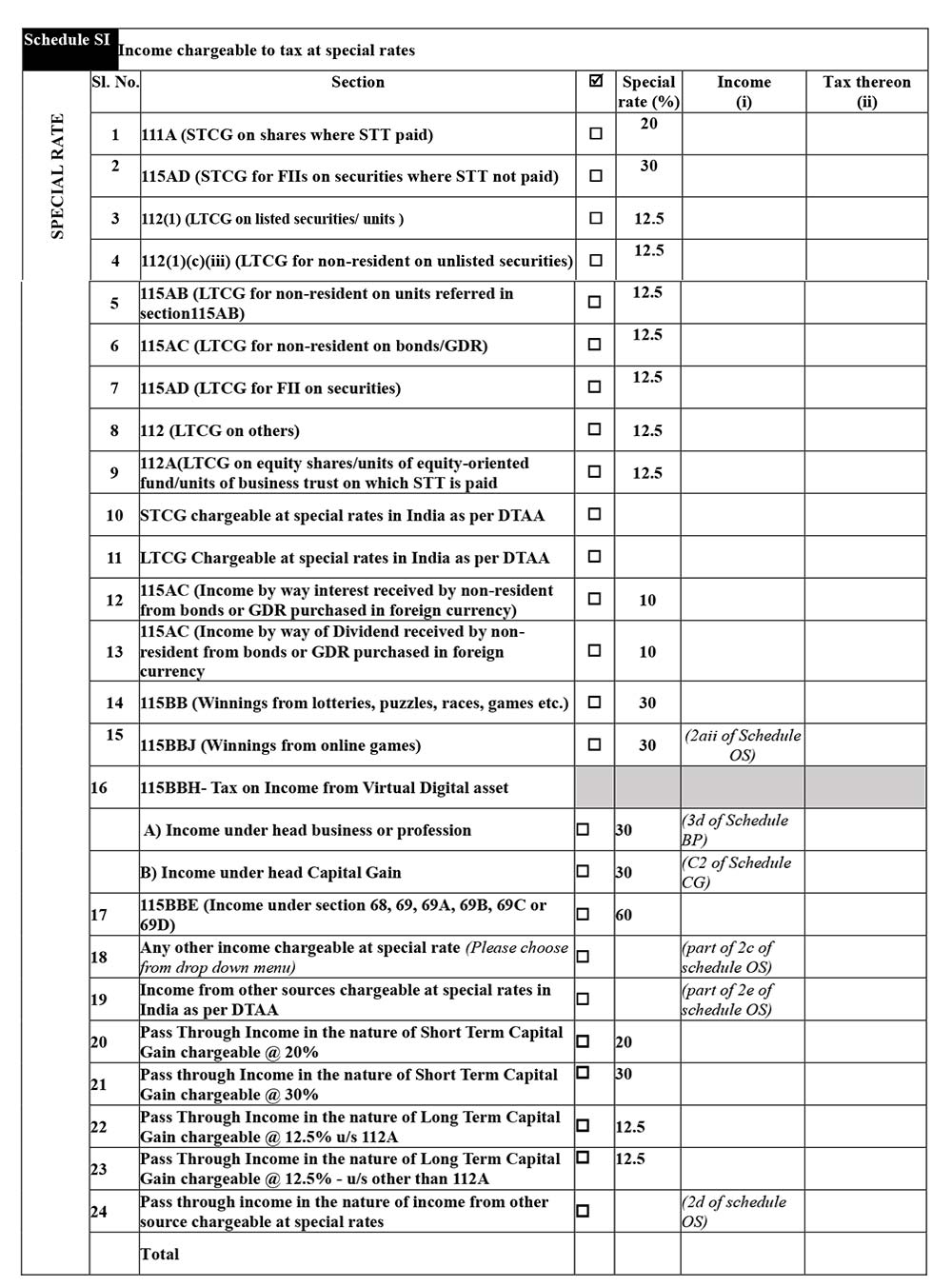

Schedule SI

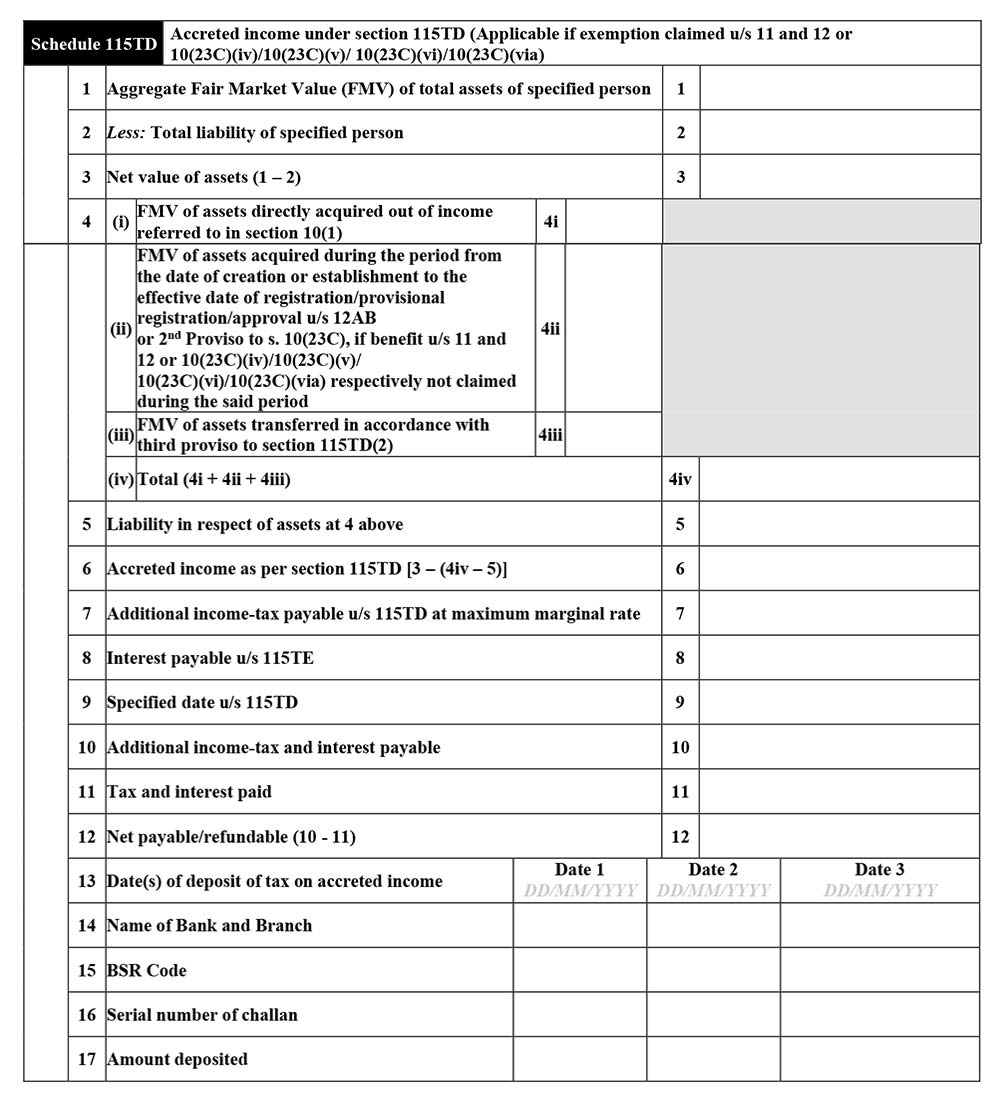

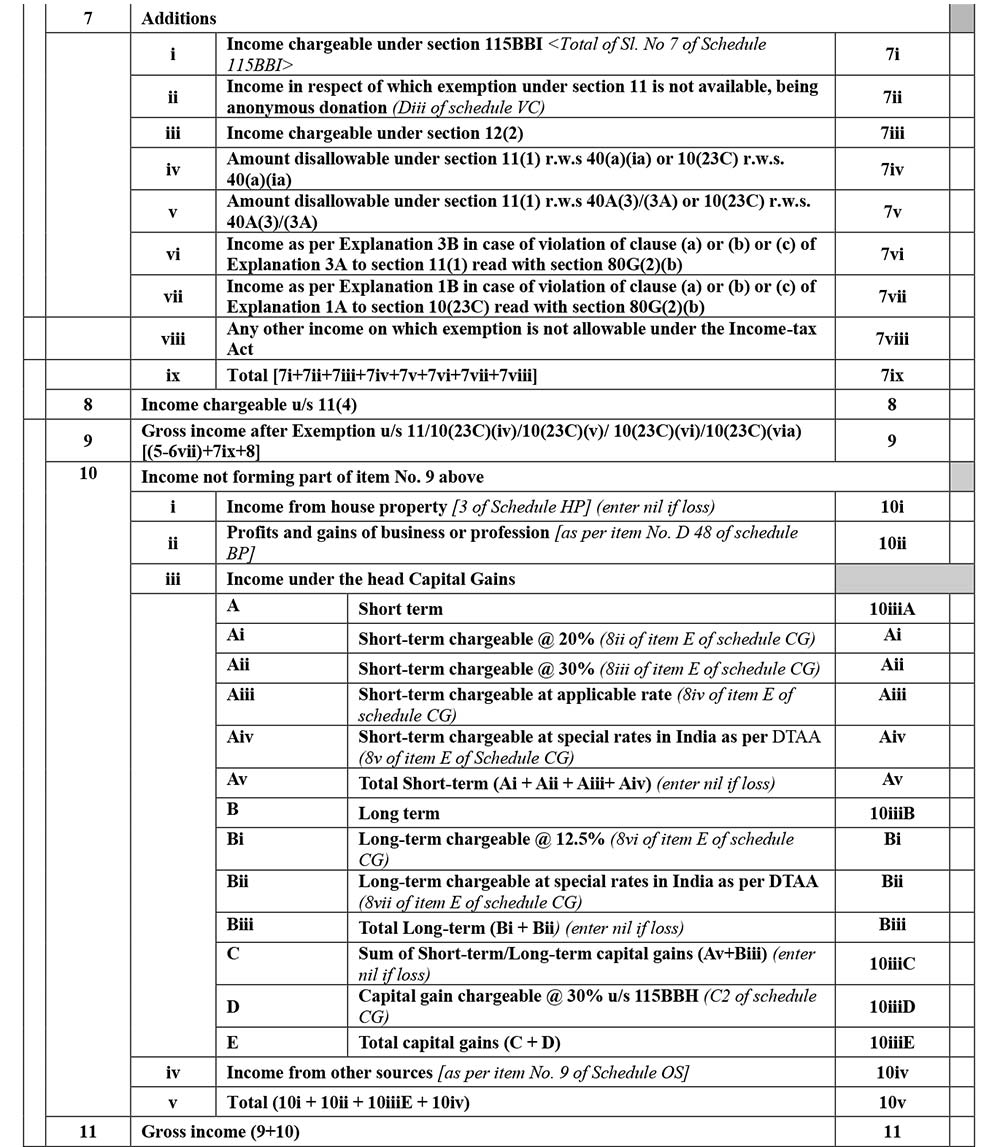

Schedule 115TD

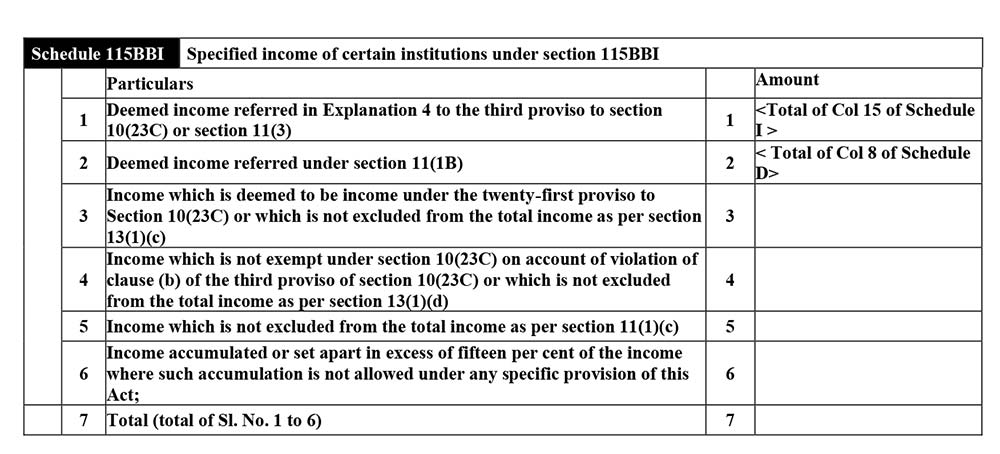

Schedule 115BBI

Schedule FSI

Schedule TR

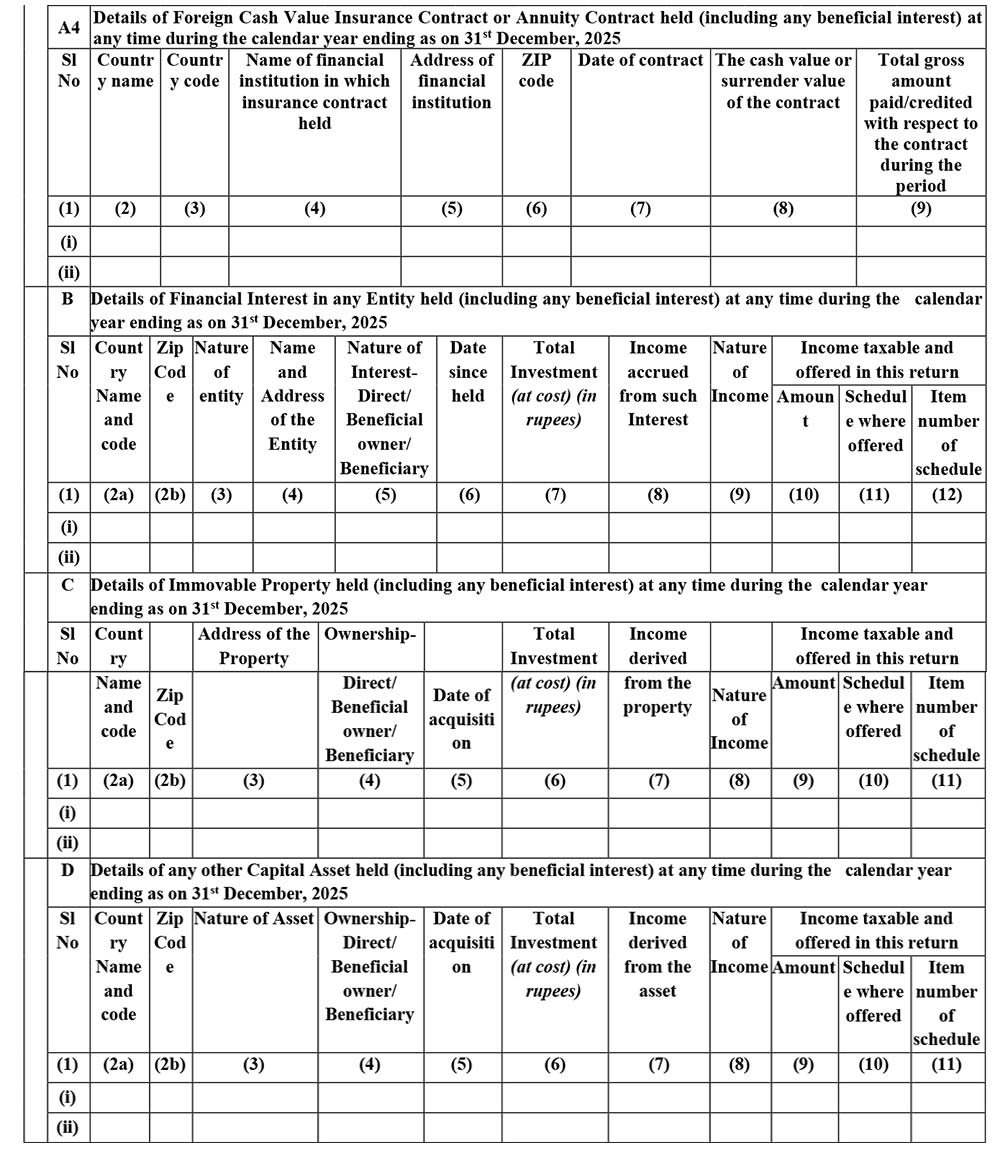

Schedule FA

Schedule SH

Part B – TI

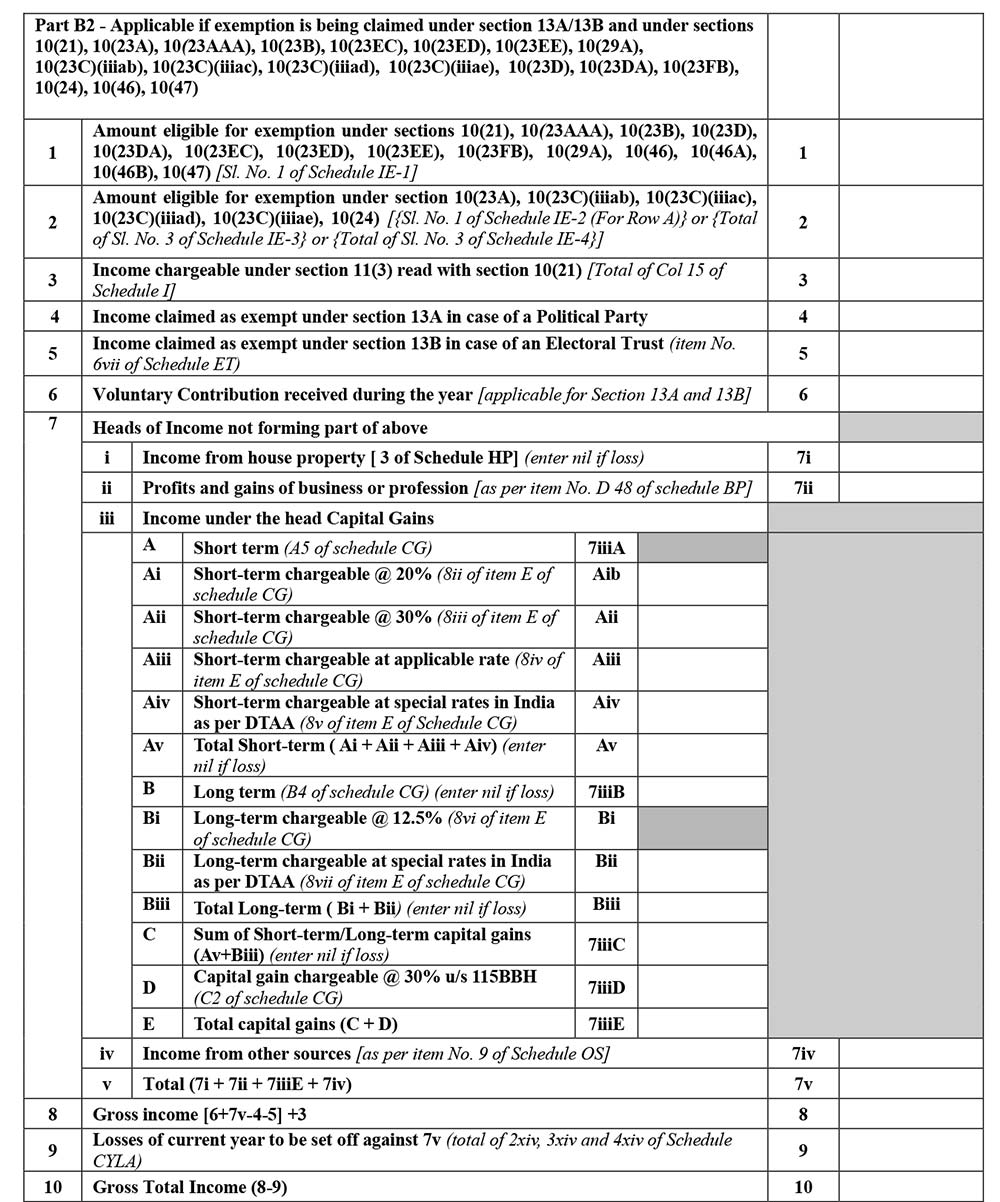

Part B2

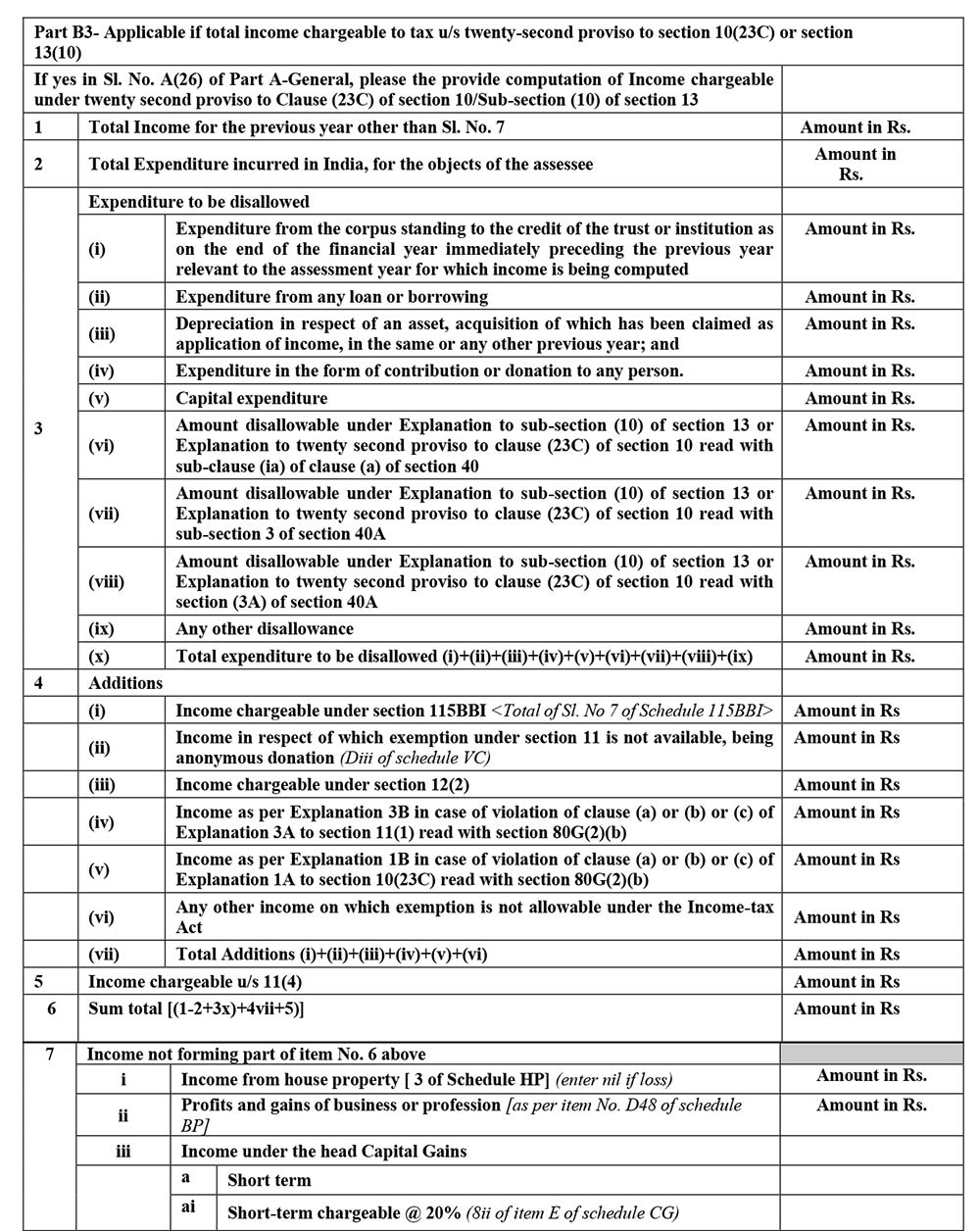

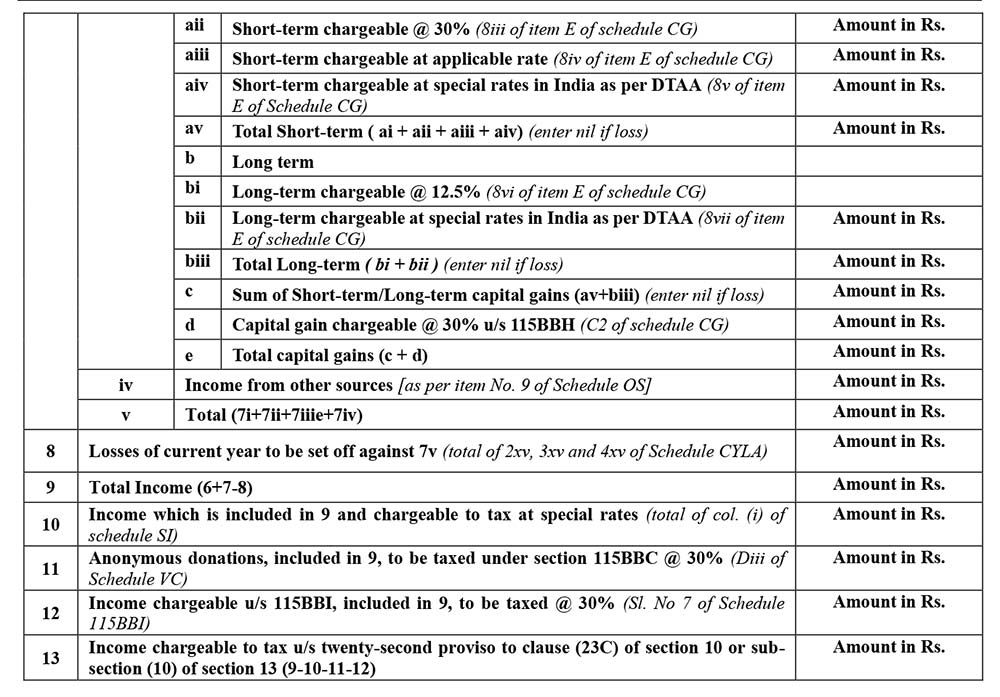

Part B3

Part B2 TTI

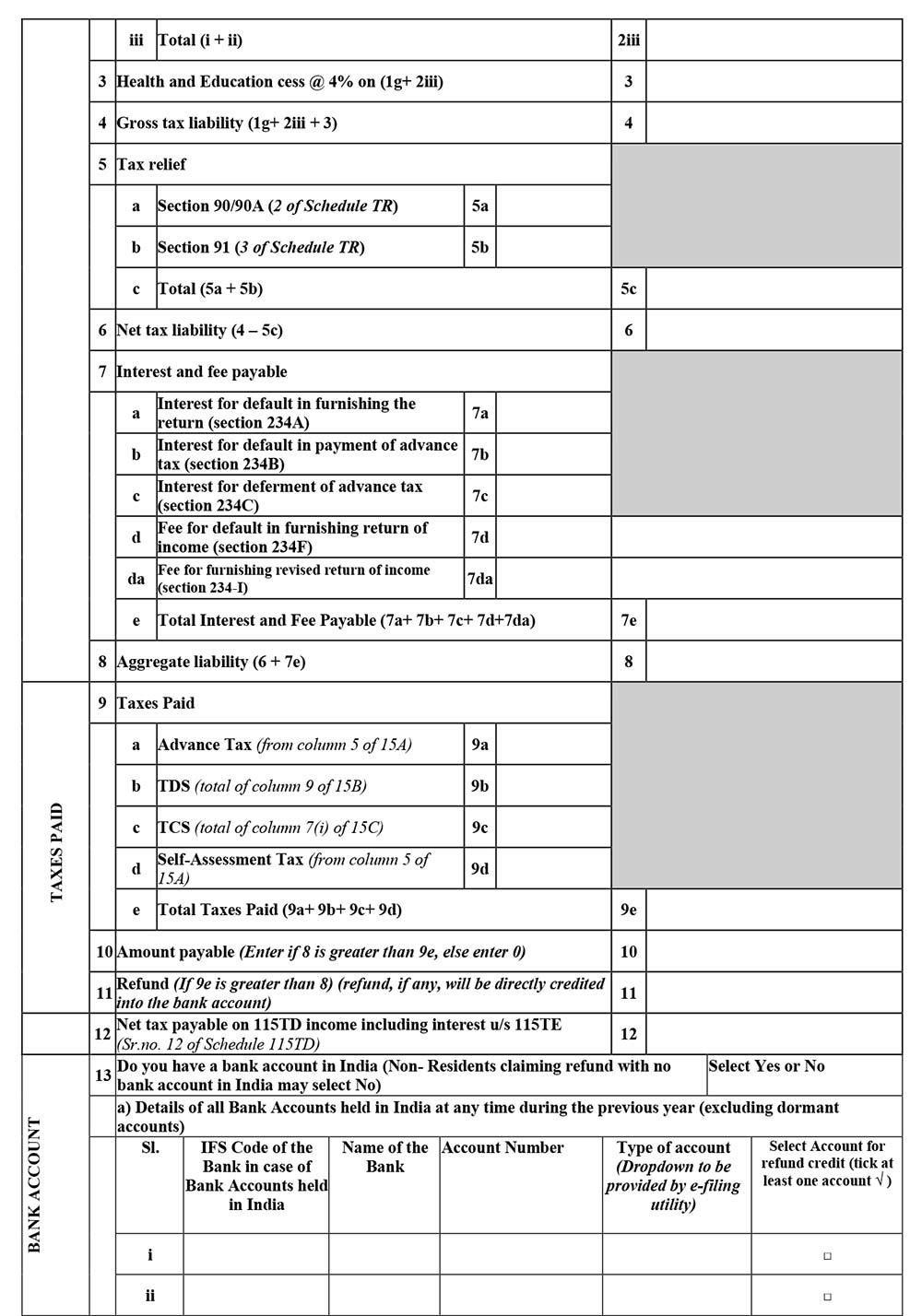

Tax Payments

Verification

Where can i fill additions of Fixed Asset in ITR 7 ?

ITR filing assessment year 2020-21 trust issue the registration section for with exemption we claimed the return

Thank you