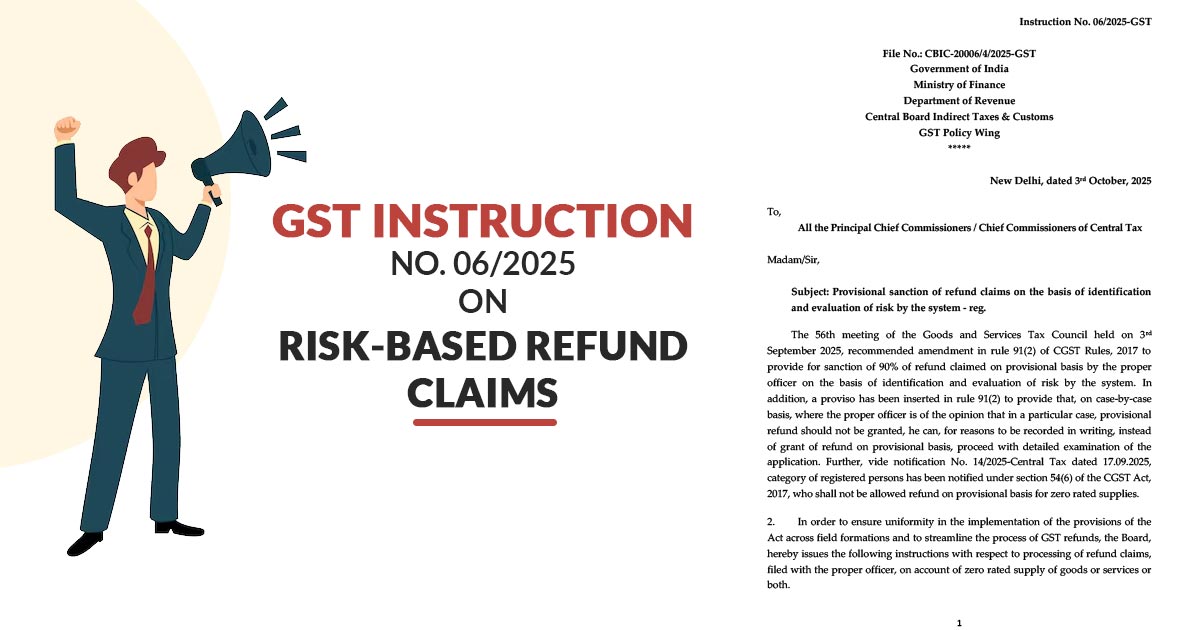

The Central Board of Indirect Taxes and Customs (CBIC) has outlined comprehensive guidelines for the provisional approval of GST refund requests through Instruction No. 06/2025-GST, issued on October 3, 2025. This process is guided by a system-driven identification mechanism and a rigorous risk assessment framework.

The same complies with the decision of the 56th GST Council meeting (September 3, 2025), which instructed an amendment to Rule 91(2) of the CGST Rules, 2017. Under the revised framework, 90% of refund claims can now be sanctioned provisionally in cases categorised as “low-risk” by the system. The motive of the revision is to ease the refund processing, reduce delays, and enhance trade facilitation.

Key Highlights of CBIC Instruction No. 06/2025-GST

- For the issuance of FORM GST RFD-02/RFD-03, refund processing must comply with timelines.

- Refund applications exhibiting as “low-risk” will be qualified for a 90% provisional sanction, as per the evaluation system.

- From October 1, 2025, as an interim measure, refund claims filed under IDS will be eligible for 90% provisional sanction till a formal amendment in Section 54(6) of the CGST Act is legislated.

- For provisional GST refund processing, GSTN has enabled functionality within the new procedure.

- Towards the particular matters where the officers assume the provisional refund must not be allotted, then they may record the reasons in writing and perform an assessment.

- Specific registered persons, notified under Notification No. 14/2025-Central Tax, shall not be qualified for provisional refunds concerning zero-rated supplies.