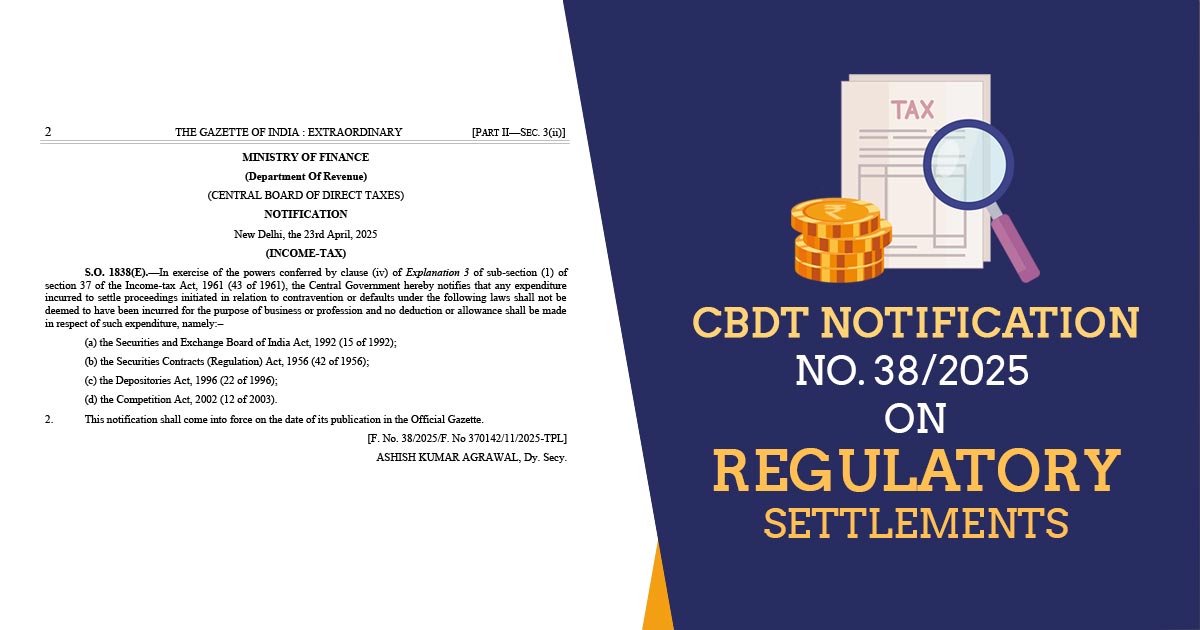

As per Notification No. 38/2025 issued by the CBDT, companies cannot claim tax deductions for money spent on settling cases involving violations of key financial and competition laws.

According to the CBDT, expenses incurred to resolve proceedings under four specific laws will not be considered business expenses.

Such statutes are: the Securities and Exchange Board of India (Sebi) Act, 1992; the Securities Contracts (Regulation) Act, 1956; the Depositories Act, 1996; and the Competition Act, 2002. From April 23, the amendments would come into force.

It is directed that at the time of the computation of an income of the company for tax purposes, the fines, penalties, or settlement amounts paid under these laws shall not be deducted. U/s 37 of the Income-tax Act, 1961, the notification has been issued which deals with the expenses of business.

It cites that these payments are pertinent to the statutory breaches and shall not be regarded as created for the objectives of business or profession.

Heavy fines and higher taxes shall be imposed by the government on the rule breakers. The same amendment restricts companies from tax savings on the money spent to settle cases in which they have broken the law.

A message has been sent by the government, the financial impact shall be drawn on non-compliance it including fines and tax treatment.