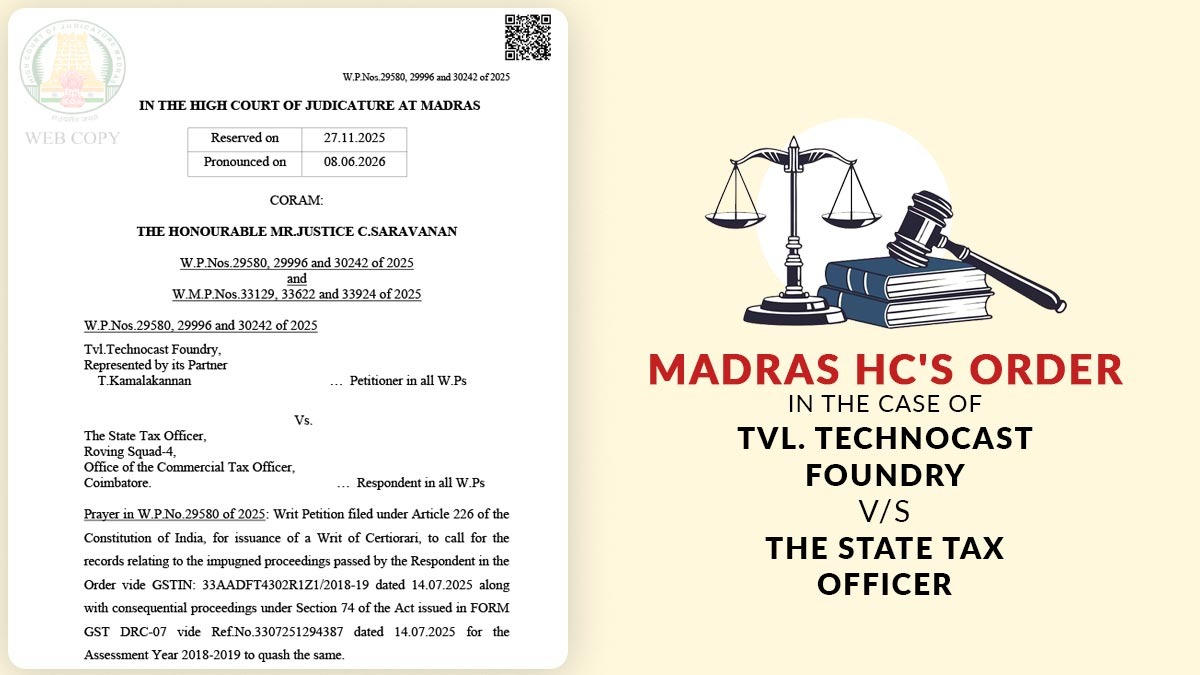

The Madras High Court has given 30 days for a reply to the GST ( Goods and Services Tax) payer who did not establish the return of goods that were sent for job work to a sister concern.

Justice C. Saravanan passed the order while disposing of writ petitions of Tvl. Technocast Foundry, contesting assessment orders passed u/s 74 of the Tamil Nadu Goods and Services Tax Act for the AY 2018-19, 2019-20 and 2020-21.

Under the facts, the GST department performed an inspection in September 2024. The authorities alleged that the applicant had sent goods to its sister concern, Tvl. Unitech Couplers India Private Limited, for job work without keeping the statutory records mandated u/s 143 and Rule 45.

The department mentioned that the applicant did not prove that the goods were received back within the mentioned period and therefore, the transactions were considered to be supplies owed to GST together with interest and penalty u/s 74.

The applicant said that the SCN did not reveal the essential ingredients for invoking Section 74, and thus the proceedings invoking the extended duration of limitation were without jurisdiction.

Technical flaws prevented the applicant from uploading Form GST ITC-04, which is needed for reporting goods sent to and received from job workers under Rule 45 of the GST Rules.

The State said that the notices proposed a charge of tax, interest u/s 50 and penalty u/s 74 for breaching Sections 143(3), 143(4) and Rule 45.

The department stated that the applicant did not keep the documentary proof exhibiting that the goods sent for job work were returned within the regulatory period, and thus the norms for invoking section 74 were fulfilled.

HC discovered that the applicant considered that it did not keep the records needed to prove the movement of goods under the job work provisions.

The Court noted the absence of records indicating that the goods sent to the sister concern had been returned to the applicant and subsequently sold or supplied with the payment of GST. In the absence of such documentary evidence, the statutory deeming fiction under Section 143 was applied, classifying the transaction as a taxable supply.

The bench dismissed the applicant’s claim against the application of Section 74, emphasizing that the Department should rely on the registered person’s records, as the GST system operates on the principle of self-assessment.

Procedures outlined in Section 74 can be initiated if a review of the records reveals errors or omissions. The Court reaffirmed its view, previously expressed in a series of related cases, that only genuine errors may qualify for an exemption from the extended time frame specified in Section 74. Additionally, the criteria for such exemptions are less stringent than those in the earlier indirect tax regulations.

However, the Court mentioned that “considering the fact that the issue could be revenue neutral, I am of the view that the case can be remitted back to the Respondent to verify the same.”

“It is for the Petitioner to establish that the Inputs that were sent to the sister Company for job work have suffered tax either in the hands of the Petitioner or in the hands of the job worker” mentioned by the bench granting 30 days to the applicant for filing a response. It asked the department to pass orders after this verification.

Subsequently, the petition was disposed of.

| Case Title | Tvl.Technocast Foundry vs The State Tax Officer |

| Case No. | W.P.Nos.29580, 29996 and 30242 of 2025 |

| For Petitioner | Mrs.R.Hemalatha |

| For Respondent | Mr.C.Harsharaj |

| Madras High Court | Read Order |