The Gujarat Authority for Advance Ruling (AAR) has mentioned that compensation recovered by a business from transporters for injury, loss, or damage suffered during the transportation of goods is not subject to Goods and Services Tax (GST).

It stated that such recoveries serve to compensate the business for the injury, loss, or damage suffered and are not considered payment for a taxable supply.

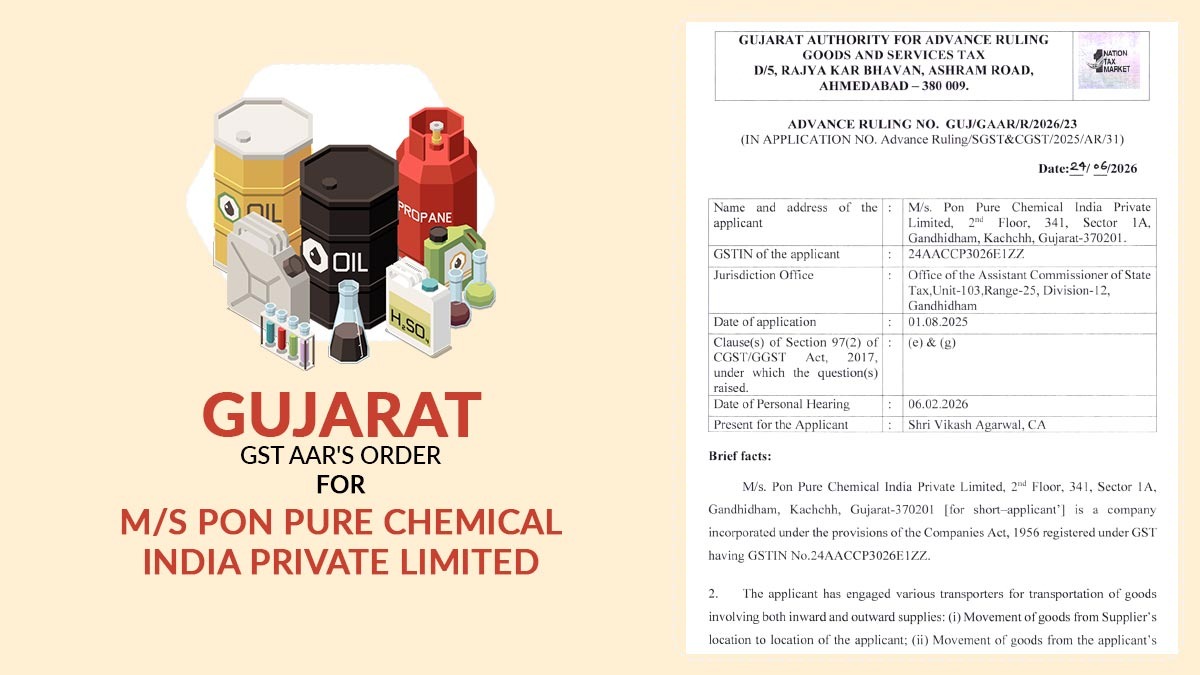

A two-member bench comprising CGST Member Sushma and SGST Member Vishal Malani furnished the ruling on an application filed by Pon Pure Chemical India Private Limited.

Important: How GST Software Helps Transport & Logistics Businesses

While observing that the recoveries were merely compensation for the injury, loss, or damage suffered by the applicant, the authority said that,

“The various circumstances under which the compensation is claimed/received from the transporters reveal that it is only a compensation for the injury, loss or damage suffered by the applicant and payment of such compensation amount does not constitute consideration for a supply.”

Pon Pure Chemical India Private Limited, which deals in chemicals, uses transporters to move goods from suppliers, ports, and its facilities to customers.

The compensation is provided when losses exceed the agreed tolerance limit or when the transporter’s negligence results in shortages during transit, tanker leaks, issues with quality or colour, damage or destruction of goods, theft or pilferage, failure to deliver goods at the designated time and place, or negligence during the handling, loading, or unloading processes.

The company requested an advance ruling to determine whether these compensations qualify as consideration for a supply of services subject to GST.

The authority reviewed the contractual arrangement and noted that compensation is only recovered after actual injury, loss, or damage has occurred. These recoveries serve as compensation for the injury, loss, or damage inflicted due to the transporter’s default.

Additionally, it was noted that there was no explicit or implied agreement whereby the applicant had consented to refrain from an action, tolerate a situation, or take any action in exchange for the compensation.

The authority referred to earlier includes advance rulings and judicial decisions regarding liquidated damages. It concluded that the compensation recovered by the applicant constituted compensation for the injury, loss, or damage suffered because of the transporters’ violation. The amounts did not comprise consideration for a supply.

Also Read: GST Impact on Petroleum Products in India

Therefore, the authority mentioned that compensation recovered from transporters for transit losses and pertinent defaults is not charged to GST.

| Name of the Applicant | M/s Pon Pure Chemical India Private Limited |

| GSTIN | 24AACCP3026E1ZZ |

| Advance Ruling No. | GUJ/GAAR/R/2026/23 |

| Present for Applicant | Vikas Agarwal |

| Gujarat AAR | Read Order |