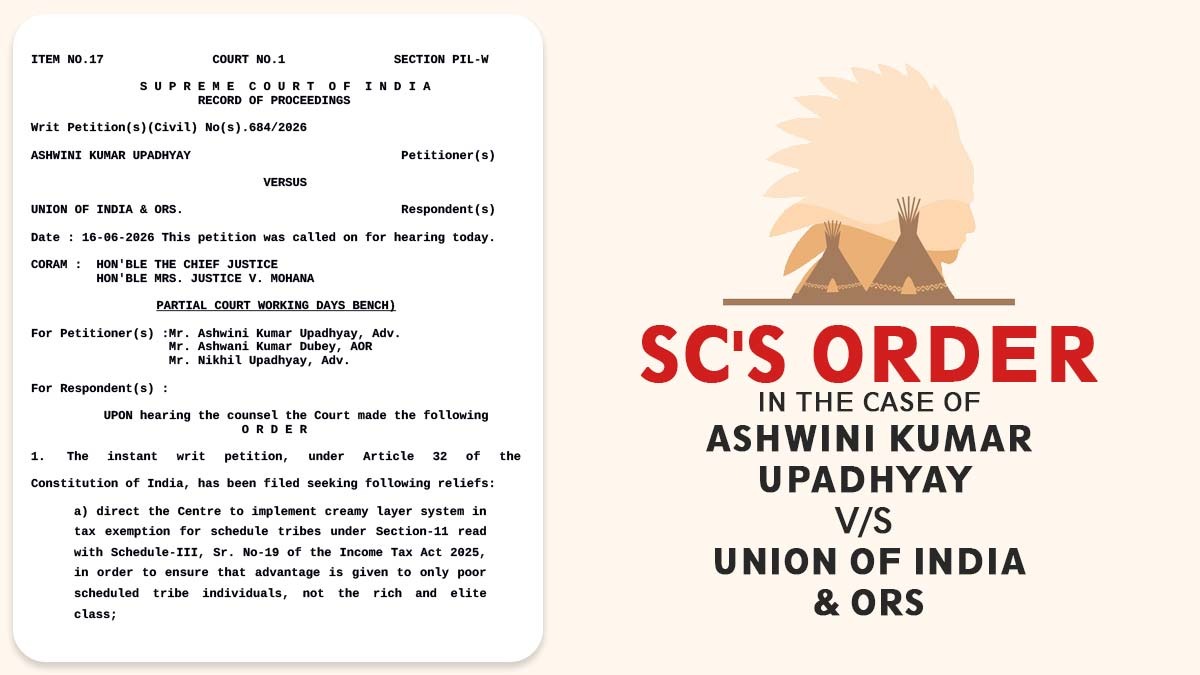

The Supreme Court declined to entertain a petition challenging the income tax exemption granted to Scheduled Tribes residing in specified North-Eastern states and certain other notified tribal areas.

The applicant, Ashwini Kumar Upadhyay, had asked for a direction to the Centre to implement a creamy layer system for income tax exemption for STs in those areas to ensure that the benefit is provided only to poor individuals and not to the rich and elite class.

He said that without setting any upper income limit, furnishing tax exemption is manifestly arbitrary, irrational and breaches various norms of the Constitution.

However, a bench including Chief Justice of India (CJI) Surya Kant and Justice V Mohana furnishes an opportunity to the applicant to approach the Centre and the relevant parliamentary committee on the matter.

It appears to us that the relief sought via the instant petition engages formulation/revision/amendment of legislative/public policies.

Read Also: Supreme Court Dismisses Curative Plea, Upholds Sec 74 Penalty for GST Non-Compliance

Hence, the Court for the aforesaid objective at this phase may not be the correct platform. The Court stated that the applicant may approach the Parliamentary Committee through a comprehensive petition.

The CJI stated that Parliament had formed a committee on petitions before which citizens can ask for the enactment, amendment or repeal of laws.

The applicant, if advised, can submit a detailed petition to the committee on petitions, established by Rule 306 of the Lok Sabha’s Rules of Procedure and Conduct of Business.

The court also permitted the petitioner to forward a copy of the writ petition, in the form of a representation, to the Ministry of Finance, the North-Eastern states, and any other relevant authorities.

| Case Title | Ashwini Kumar Upadhyay vs. Union of India & Ors |

| Case No. | No(s).684/2026 |

| For the Petitioner | Mr Ashwini Kumar Upadhyay, Mr Ashwani Kumar Dubey, and Mr Nikhil Upadhyay |

| Supreme Court | Read Order |