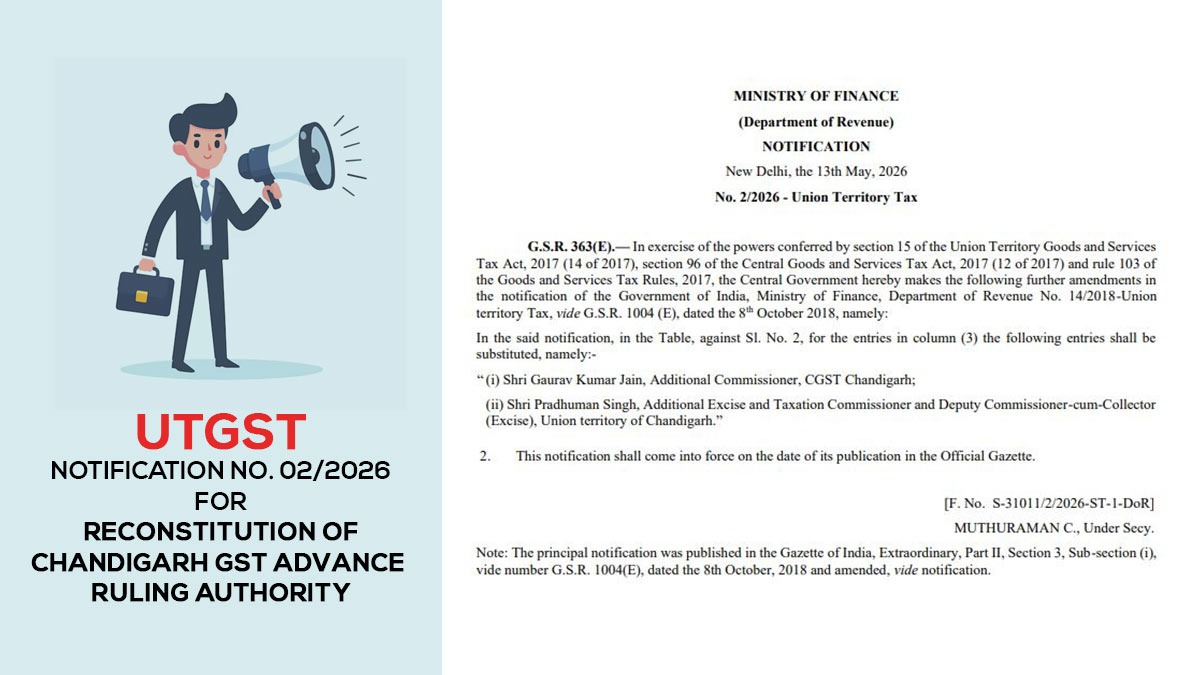

The Ministry of Finance’s Department of Revenue has given a new Notification No. 2/2026 regarding the Union Territory Tax. This update, which comes from May 13, 2026, brings modifications to how the GST authority is structured for the Chandigarh Union Territory.

The notification, published through G.S.R. 363(E), changes the earlier Notification No. 14/2018-Union Territory Tax dated October 8, 2018, which regulates the appointment of members under the Union Territory Goods and Services Tax (UTGST) mechanism.

Major Key Updates Rolled out

The Central Government, under the latest notification, has replaced the existing entries under Serial Number 2 of the previous notification to appoint new officers representing Chandigarh in the concerned GST authority.

The revised composition now includes:

- Shri Gaurav Kumar Jain, Additional Commissioner, CGST Chandigarh

- Shri Pradhuman Singh, Additional Excise and Taxation Commissioner and Deputy Commissioner-cum-Collector (Excise), Union Territory of Chandigarh

Now the officials will serve in place of the earlier entries mentioned in the notification table.

Legal Basis of the Amendment

The Central Government has issued the amendment by exercising powers under:

- Section 15 of the Union Territory Goods and Services Tax Act, 2017

- Section 96 of the Central Goods and Services Tax Act, 2017

- Rule 103 of the Goods and Services Tax Rules, 2017

The main concern of the notification is for the functioning of the administration and constitution of GST-related authorities in Union Territories.

Useful Date

As per the ministry, the amendment will be in force from the date of its publication in the Official Gazette, which implies that the revised appointments are effective immediately.

Importance of This Update

However, the notification does not roll out any revision in GST rates, return filing, or compliance obligations for taxpayers; it is crucial from an administrative and regulatory viewpoint.

These changes confirm that GST adjudication, interpretation, and pertinent administrative functions continue seamlessly under updated official representation.

The revision may be especially pertinent to professionals, tax practitioners, and businesses dealing with GST matters in the Union Territory of Chandigarh, particularly where authority-related proceedings or clarifications are involved.

UT Tax Notification 02/2026