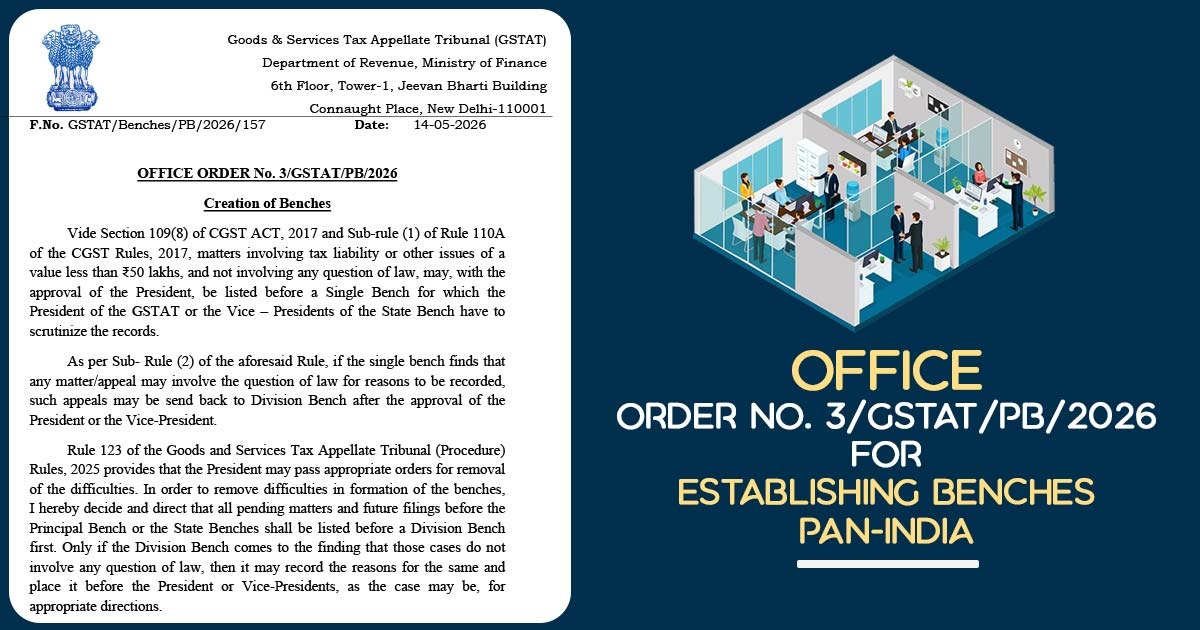

The Goods and Services Tax Appellate Tribunal (GSTAT) has announced that all ongoing cases and new filings must first be reviewed by smaller groups, called Division Benches, before being handled by the main and state teams.

The law allows cases with a tax liability or other issues of less than Rs 50 lakh, not involving any question of law, to be listed before a Single Bench with the President’s approval.

In an office order dated May 14, 2026, GSTAT President Dr Sanjaya Kumar Mishra stated that u/s 109(8) of the CGST Act and Rule 110A of the CGST Rules, such cases may be listed before a Single Bench with the approval of the President.

Although invoking Rule 123 of the GSTAT (Procedure) Rules, 2025, which permits the President to pass orders to eliminate issues, the tribunal stated that all due matters and future filings shall be listed before a Division Bench.

The order stated that, “I hereby decide and direct that all pending matters and future filings before the Principal Bench or the State Benches shall be listed before a Division Bench first. Only if the Division Bench comes to the finding that those cases do not involve any question of law, then it may record the reasons for the same and place it before the President or Vice-Presidents, as the case may be, for appropriate directions.”

The order involves benches across states and categorises disputes into 3 groups for administrative allocation.

Category I comprises disputes that have classification of goods or services, applicability of notifications, valuation, input tax credit, tax liability, registration requirements, and proceedings that include tax short payment or fraud.

Category II includes registration-related disputes, cancellation and revocation proceedings, composition scheme matters, recovery proceedings, assessment orders, and refund-related disputes.

Category III consists of seizure and confiscation matters, rectification orders, provisional attachment, penalty proceedings, compounding matters, and residual disputes.

As per the tribunal, Category III matters shall ordinarily be heard by the bench that deals with the principal dispute from which these consequential proceedings emerge, except at the Karnataka, Guwahati, and Kolkata State Benches.

Benches have been specified across multiple jurisdictions, along with the Guwahati Bench for Assam, Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland and Tripura; the Delhi Bench; the Bengaluru Bench for Karnataka; the Hyderabad Bench for Telangana; the Patna Bench for Bihar; the Raipur Bench for Chhattisgarh; the Ranchi Bench for Jharkhand; and the Srinagar and Jammu Benches for Jammu & Kashmir and Ladakh.

The order furnishes for multiple benches in larger states and regions along with the Chennai, Coimbatore and Madurai Benches, including the Puducherry Circuit Bench, for Tamil Nadu and Puducherry; the Ahmedabad, Rajkot and Surat Benches for Gujarat and the Union Territories of Dadra & Nagar Haveli and Daman & Diu; the Jaipur and Jodhpur Benches for Rajasthan; the Chandigarh and Jalandhar Benches for Punjab and Chandigarh; the Ernakulam and Thiruvananthapuram Benches for Kerala and Lakshadweep; the Mumbai, Nagpur, Pune, Thane, Panaji and Chhatrapati Sambhajinagar Benches for Maharashtra and Goa; and the Ghaziabad, Lucknow, Prayagraj, Varanasi and Agra Benches for Uttar Pradesh.

Read Also: How GST Software Helps Protect Your Business from Cancellation

Also, the order permits members assigned to neighbouring jurisdictions or additional locations to conduct virtual, hybrid, or circuit hearings in consultation with the concerned Vice-Presidents.

Members assigned to neighbouring states or different places of posting shall be qualified to travel and receive daily allowances equivalent to Level 17 Central Government officers, with the concerned benches needed to furnish crucial support for travel and stay.

Read Official Order No. 3/GSTAT/PB/2026