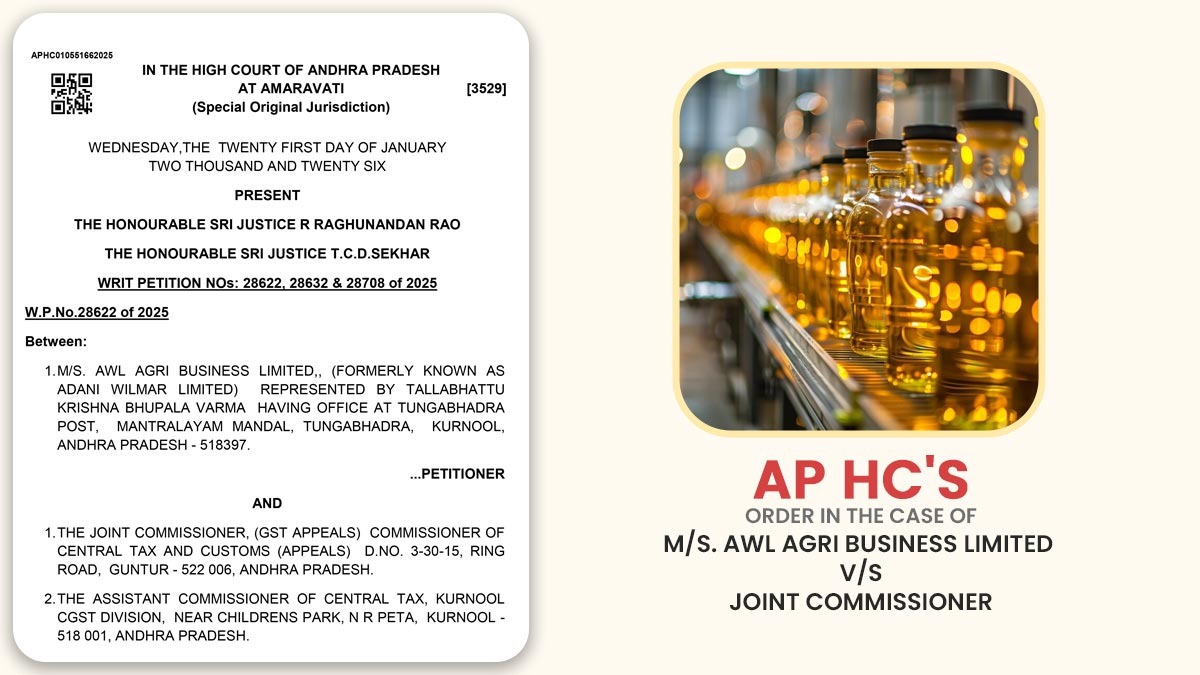

The Andhra Pradesh High Court has stated that the revised formula under Rule 89 (5) of the GST Rules for inverted duty refunds is retrospectively applicable.

The bench of Justice R Raghunandan Rao and Justice T.C.D.Sekhar has cited that the revision to the formula in Rule 89(5) must be considered to be clarificatory in nature and, consequently, would be retrospective. However, the orders of rejection, including the appellate order, were passed before the amendment; the fact is that the applicant had continued to agitate his claims concerning the refund sought by the applicant.

The applicant, M/s AWL Agri Business Limited, is engaged in importing edible oil, refining it, and supplying it in the domestic market after packaging. The company had submitted three separate applications asking for the refund of accumulated Input Tax Credit (ITC) for November 2018, March 2019, and April 2019, citing an inverted duty structure.

Also Read: How GST Software Handles Input Tax Credit (ITC) Tracking

Under Section 54 of the CGST Act, the refund claims were incurred. But, the adjudicating authority denied the applications, keeping that Rule 89(5) of the CGST Rules precluded these refunds under the mentioned formula. Thereafter, the appellate authority dismissed appeals through Order-in-Appeal on February 25, 2022.

The dissatisfied applicant approached the High Court under Article 226 of the Constitution, asking for the quashing of the appellate order and a refund of 48,29,179 for April 2019, along with interest at 6% under section 56 of the CGST Act.

The problem before the Court was whether the revisions to the formula specified under rule 89(5) made as per the deliberations of the GST Council were clarificatory and retrospective in nature, or prospective as claimed by the revenue authorities.

The applicant mentioned that the GST council, in its meeting conducted on June 28th and 29th, 2022, took cognisance of anomalies in the refund formula. The revision was incurred after the observations of the Supreme Court in Union of India vs. VKC Footsteps India Pvt. Ltd. (2022) 2 SCC 603. The revision was effective and must be applied retrospectively. As the refund claims were under challenge, the changed formula must be applied.

On November 10, 2022, the department relied upon Circular No. 181/13/2022-GST, which specified that the amendment would operate prospectively w.e.f July 5, 2022. It was claimed that, as the rejection and appellate orders were passed before the amendment, the benefit could not be extended to the applicant.

The applicant put reliance on the judgment of the Gujarat High Court in Tirth Agro Technology Pvt. Ltd. v. Union of India(2025), where the High Court had set aside the circular to the scope it declared the amendment to Rule 89(5) as prospective.

The Andhra Pradesh High Court stated that once a circular is set aside by an HC, it shall not be considered in the nation.

The Division Bench said that the amendment to the formula under Rule 89(5) should be acknowledged as clarificatory in nature. Thereafter, it shall function retrospectively. However, the original denial and appellate orders were passed before the revision; therefore, the applicant had started pursuing its claims. Hence, the applications should be reconsidered by applying the revised formula.

Read Also: GST Refund Claim on Input Services U/S 54 of CGST Act

The Court permitted the writ petitions and set aside the primary denial orders on June 9, 2021; January 13, 2021; and March 24, 2021; set aside the appellate order on February 25, 2022; and directed the primary authority to reconsider the refund applications afresh by applying the revised formula under Rule 89(5).

| Case Title | M/s. Awl Agri Business Limited vs. Joint Commissioner |

| Order No | W.P.No.28622 of 2025 |

| Counsel for the Petitioner | Karan Talwar |

| Counsel for the Respondent | Santhi Chandra |

| Andhra Pradesh High Court | Read Order |