In the first ruling of the GST Appellate Tribunal (GSTAT), Principal Bench, it has ruled that where differences between GSTR-1 and GSTR-3B emerge due to credit notes, advances, and timing adjustments duly recorded in the books, the taxpayer should be allowed to revise their returns.

The bench of S.K. Mishra, President, in the case of M/s Sterling & Wilson Pvt. Ltd. vs Commissioner, Odisha, has stated that the First Appellate Authority (FAA) could not itself convert proceedings from Section 74 to Section 73 of the GST Act, 2017 and determine liability. The tax redetermination should be accomplished only by the Proper Officer u/s 75(2).

The appellant is an EPC services company registered under GST, encountered a demand for FY 2018-19 on the ground that the output tax liability declared in GSTR-1 exceeded the tax paid through GSTR-3B by about Rs 27 lakh.

The department considered the difference as a short tax payment and issued proceedings u/s 74 alleging suppression. A demand for tax, interest and equal penalty was raised.

The Appellate Authority in the first appeal accepted that no fraud or suppression intent was there, yet kept the tax and interest and converted the matter to Section 73 from Section 74. It limits the penalty at 10% u/s 73(9).

The case was contested by the taxpayer before the GSTAT.

Taxpayer, the mismatch was because of timing differences, credit notes, debit notes, and advance adjustments concerning different tax periods, which could not be revised in GSTR-1 due to system limitations prevalent in the early GST years.

Reconciliation statements were filed related to the differences in customer-wise credit notes, advance tax adjustments, and prior-period corrections, all duly recorded in books and reflected in GSTR-3B.

It claimed that no revenue loss and no purpose to evade tax was there, and thus demand based on return mismatch without reconciliation verification was not sustainable.

But the revenue countered the appeal, claiming that the returns are self-assessed declarations and mismatches should be rectified under the GST Act.

It mentioned that the credit notes were furnished after the timelines u/s 34(2), revisions were not carried out in GSTR-1, and reconciliation was shown improperly in GSTR-9 and GSTR-9C.

It said that the taxpayer loses to establish the ITC reversal via receiver wherever credit notes were claimed, thereby justifying confirmation of demand and interest.

The objection of the revenue has been denied by the GST appellate tribunal that the factual re-appreciation was barred.

The Tribunal mentioned that no fraud, wilful misstatement, or suppression was discovered on the part of the appelate authroty amd that the transactions were kept by debit and credit notes and accurately recorded in the books of account.

The bench observed that concerning the legal matter of transitioning from Section 74 to Section 73, according to Section 75(2) and the guidelines outlined in the CBIC Circular, if the allegations of fraud do not hold, the re-evaluation under Section 73 must be conducted by the Proper Officer rather than the Appellate Authority.

Also Read: How GST Software Resolves GSTR-3B & 2A/2B ITC Mismatches

The actions of the First Appellate Authority in directly transitioning the case to Section 73, along with the confirmation of the demand and the reduced penalty, were deemed unsustainable.

The bench cited that “CGST / SGST Act is a relatively new Act and professionals may not be thorough in the filing of returns for the relevant period, together with the fact that, at that particular time, most ofthe returns were being filed manually and the technique of auto-population and full online filing was not operational to the fullest extent as it is now. There were chances of human error. To obviate any such human error, the matter should be reconsidered by the learned Proper Officer.”

Read Also: Recent High Court Ruling on GST Return Mismatch Cases

Therefore, the principal bench set aside the order to the scope they considered the matter u/s 73 and validated the demand. It kept the finding that section 74 was not attracted.

For fresh consideration u/s 73, the case was remanded back to the proper officer, granting the taxpayer to submit the revised application and reconciliation materials within 1 month.

The department was asked to determine the case post proper hearing and acknowledge the genuineness of debit /credit notes.

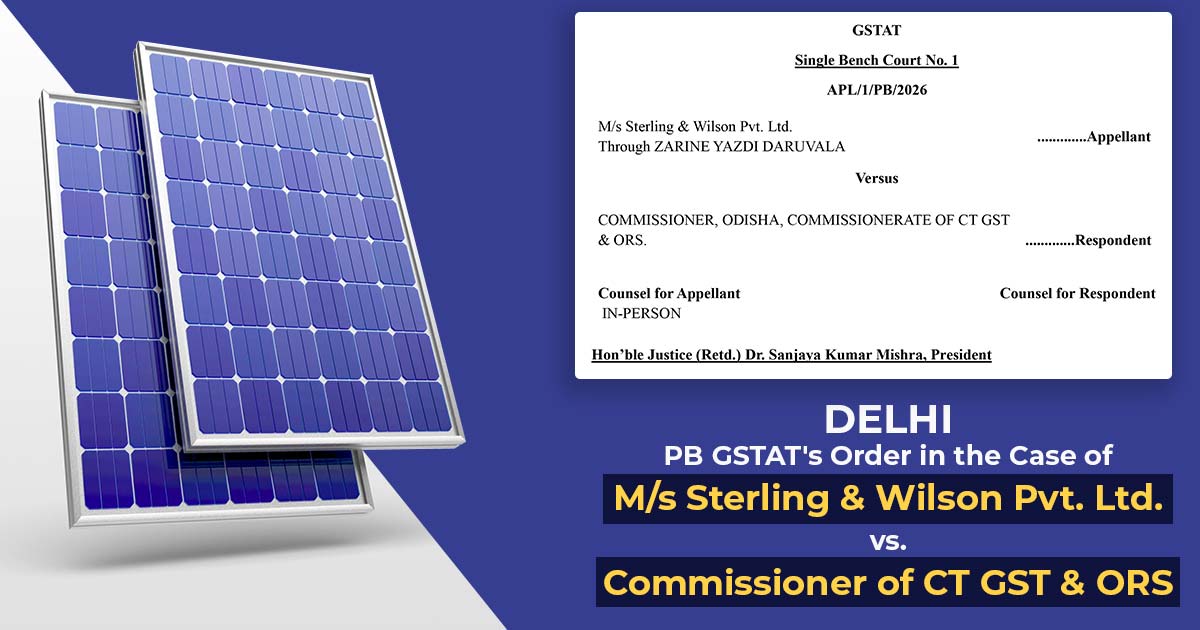

| Case Title | M/s Sterling & Wilson Pvt. Ltd. vs. Commissioner of CT GST & ORS |

| Case No. | APL/1/PB/2026 |

| Name of the Appellant | Zarine Yazdi Daruvala |

| Name of the Respondent | Sanjukta Gantayat |

| Delhi PB GSTAT | Read Order |