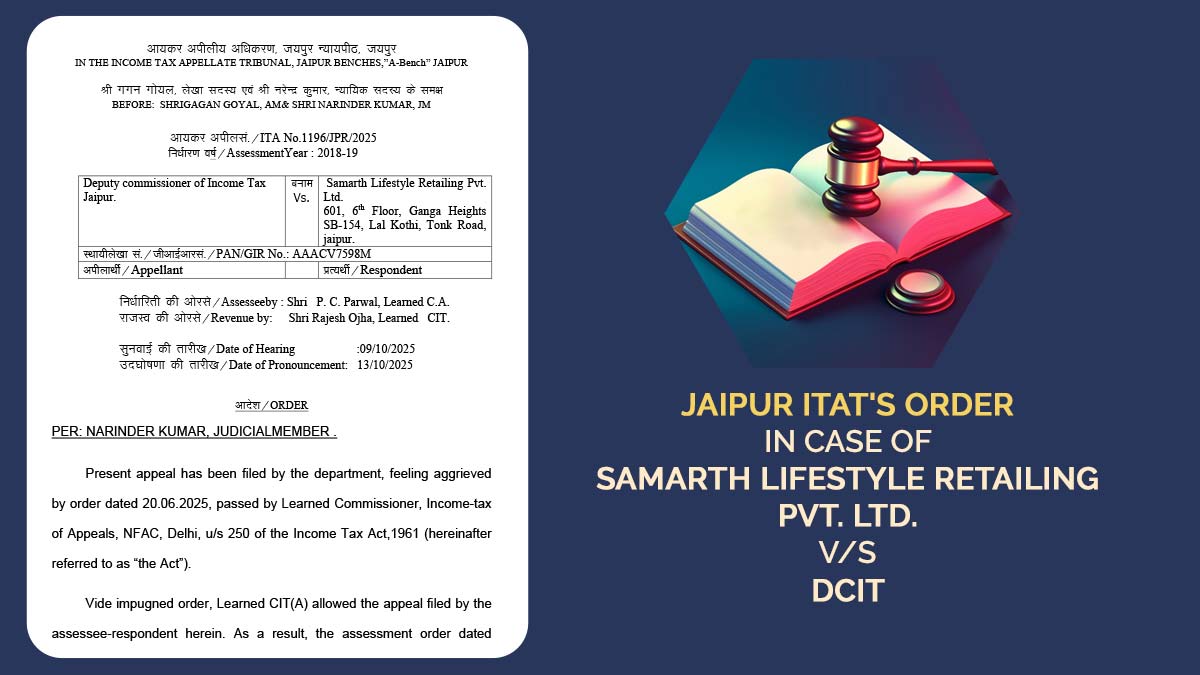

The Jaipur Bench of the Income Tax Appellate Tribunal (ITAT) validated the deletion of an addition of ₹2,16,27,822 made u/s 69A of the Income Tax Act, 1961, due to a mismatch between the commission and other income reported in the books and the figures specified in Form 26AS.

The taxpayer, Samarth Lifestyle Retailing Pvt. Ltd., a private limited company, was chosen for scrutiny for the AY 2018-19, partly on the problem of low income compared to large commission receipts. The assessing officer witnessed a discrepancy of ₹2,33,29,736 in commission income compared to the figures shown in Form 26AS and issued a show cause notice.

A detailed reconciliation has been provided by the taxpayer, elaborating that the whole receipts showing in Form 26AS were incorporated and declared in the audited financial statement under the head “Commission and other income” and “Rent and CAM income.”

Party-wise explanations have been provided by the taxpayer, marking that in specific matters, the TDS deductor had incurred mistakes in reporting the section (e.g., reporting under Section 194-I instead of 194-C or 194-H) or the reported amount in 26AS was false. AO denied the detailed reconciliation as the taxpayer is not able to furnish opposite confirmations from the deductor parties and does not file enough supporting proof for the transactions.

Under Section 69A of the Act, AO proceeded to make an addition of ₹2,16,27,822 and treated the cash deposits/receipts as unexplained income, without addressing the detailed reconciliation provided for the Form 26AS mismatch.

The taxpayer is dissatisfied with the order of the AO and submitted an appeal to the Commissioner of Income Tax (Appeals) [CIT(A)]. The CIT(A), the taxpayer specified the source of its receipts, citing that all the transactions were reported in the books of account, which were duly audited under section 44AB of the Act.

The CIT(A) said that the receipts source that includes cash was fully explained as cash obtained via work function and cash received from debtors. CIT(A) concluded that the addition and treating the receipts as unexplained u/s 69A of the Act was unexplained when the amounts were previously accounted for in the audited books.

The department is dissatisfied with the CIT(A) order, and it has submitted a plea to the ITAT. Department, the CIT(A) had made a mistake by removing the addition without calling for a remand report on the new explanations/material.

Read Also: Taxpayer Relief: ITAT Mumbai Strikes Down ₹1 Crore Demand Over TDS Error

The two-member bench, Gagan Goyal (Accountant Member) and Narinder Kumar (Judicial Member), ensured that the taxpayer had explained the total receipts, and the addition was made only based on a mechanical mismatch with Form 26AS entries, overlooking the audited financial statements.

The tribunal stated that when all transactions are recorded in the books of account, and the books are audited, an addition under section 69A (unexplained money) cannot be made because of reconciliation issues with Form 26AS entries.

The removal of the addition has been kept by the tribunal. Therefore, the department’s submitted appeal was dismissed.

| Case Title | Samarth Lifestyle Retailing Pvt. Ltd. vs. DCIT |

| Case No. | ITA No.1196/JPR/2025 |

| Assessee by | Shri P. C. Parwal |

| Revenue by | Shri Rajesh Ojha |

| Jaipur ITAT | Read Order |