The Allahabad High Court has stated that the expiration of an e-way bill due to a vehicle breakdown does not constitute an attempt to evade tax under the Goods and Services Tax (GST) Act.

The court has overturned the seizure and penalty orders, emphasising that technical issues arising from unforeseen circumstances should not be viewed as instances of tax evasion.

The applicant, Trimble Mobility Solutions India Pvt. Ltd., is in the business of furnishing vehicle tracking services across India and holds valid GST registrations in multiple states, including Uttar Pradesh, Haryana, Maharashtra, and Tamil Nadu.

The company has entered into a contract with the Surveyor General of India, specifically the National Geo-Spatial Data Centre, to supply and install GPS tracking devices. This collaboration aims to enhance geospatial data capabilities and improve tracking services.

In device transportation, a vehicle breakdown takes place while the goods are in transit. The e-way bill that contains the consignment was valid for 12 days and lapsed dated 20 December 2022 because of the delay. The driver, without notifying the applicant, has tried to repair the vehicle and thereafter has transferred the goods into another vehicle to finish the journey.

The goods dated 22 December 2022 were intercepted by the tax authorities based on the fact that the e-way bill had lapsed. The applicant has generated a fresh e-way bill on the same day at 11:30 a.m., before the passing of a seizure order by the authorities.

Even after this, the authorities moved to levy a penalty and seize the goods u/s 129(3) of the CGST Act. On 17 June 2023, the appeal of the applicant was rejected by the appellate authority.

The applicant claimed that the delay was not intended and was caused because of the mechanical breakdown of the vehicle. No tax evade attempt was there since a valid tax invoice and e-way bill were initially issued, and a new one was generated before the seizure order.

Read Also: Allahabad HC: Clerical GST E-way Bill Errors Alone Do Not Justify Penalty or Seizure

The petitioner put reliance on several precedents, including the Supreme Court’s decision in Assistant Commissioner (ST) v. Satyam Shivam Papers Pvt. Ltd. and Allahabad High Court rulings in Ashoka P.U. Foam (India) Pvt. Ltd. v. State of U.P. (2024), Riadi Steels LLP v. State of U.P. (2024), and Globe Panel Industries India Pvt. Ltd. v. State of U.P. (2024), all of which held that mere expiry of an e-way bill without intent to evade tax does not justify penalty proceedings.

As the e-way bill had lapsed when the goods were intercepted, the applicant breached the GST provisions, the State claimed. It stated that even if the vehicle broke down, the applicant was required to generate a new e-way bill before continuing transportation.

Justice Piyush Agrawal said that the facts were correct, that the goods were being transported under a valid tax invoice and e-way bill, which lapsed due to the vehicle breakdown.

The court said that the applicant generated a new e-way bill before the issuance of the penalty order, and no proof of tax evade intent was there.

The bench stated that the expiry of an e-way bill alone cannot be interpreted as evidence of tax evasion, especially when the movement of goods and tax documentation is otherwise bona fide.

The court, while setting aside both the seizure and penalty orders on 27 December 2022 and 17 June 2023, ruled that the proceedings u/s 129(3) were not sustainable in law. It quashed the impugned orders, permitting the writ petition.

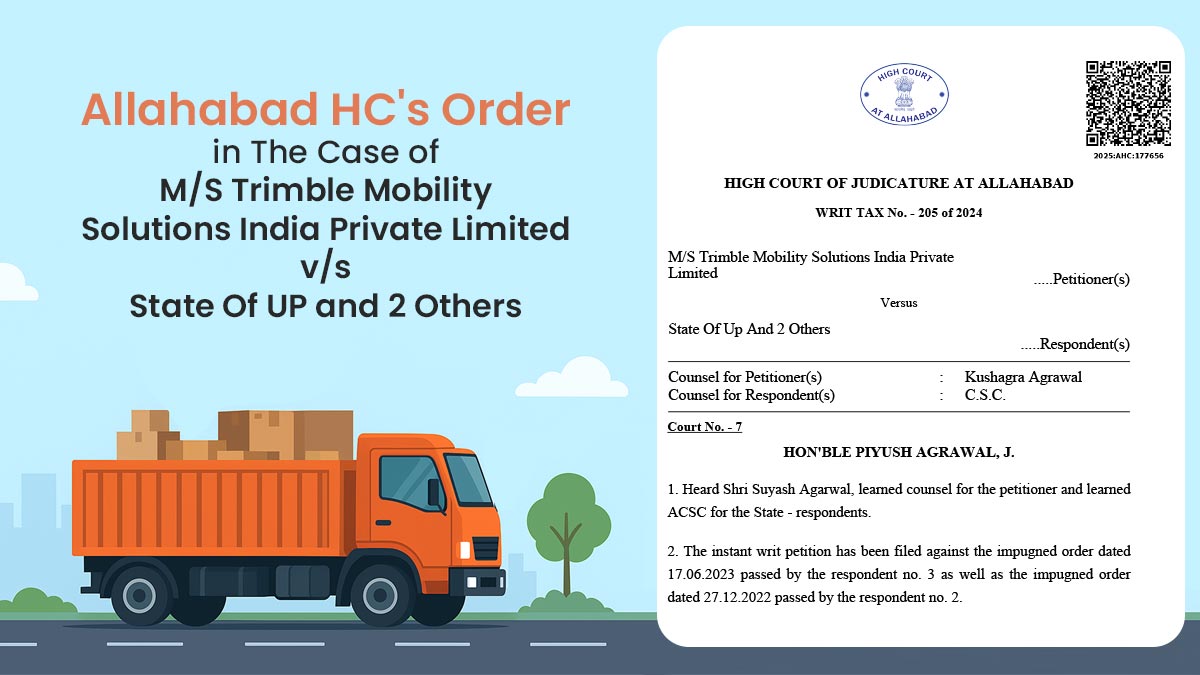

| Case Title | M/S Trimble Mobility Solutions India Private Limited vs. State Of UP and 2 Others |

| Case No. | WRIT TAX No. – 205 of 2024 |

| Counsel for Petitioner | Kushagra Agrawal |

| Counsel for Respondent | C.S.C. |

| Allahabad High Court | Read Order |