The Apex court is to decide whether the time limit for adjudicating the show cause notice and passing an order could be extended via the issuance of the notifications u/s 168-A of the CGST Act. The same provisions provide the authority to the government to issue the notification for extending the time limit specified under the act which could not be complied with as of the force majeure.

The Bench of Justices J.B. Pardiwala and R. Mahadevan said that “the issue that falls for the consideration of this Court is whether the time limit for adjudication of show cause notice and passing order under Section 73 of the GST Act and SGST Act (Telangana GST Act) for the financial year 2019-2020 could have been extended by issuing the Notifications in question under Section 168-A of the GST Act.”

It is relevant to cite that Section 168 (1) reads as:

“168A. Power of Government to extend time limit in special circumstances.— (1) Notwithstanding anything contained in this Act, the Government may, on the recommendations of the Council, by notification, extend the time limit specified in, or prescribed or notified under, this Act in respect of actions which cannot be completed of complied with due to force majeure.”

A batch of petitions were filed before the Telangana High Court in its writ jurisdiction. Therein, among others, they had contested the legality, validity, and propriety of notification Nos.13/2022, dated 05.07.2022, 9 and 56/2023, dated 31.03.2023 and 28.12.2023, respectively.

Before the HC it was claimed that the SCN was issued dated 31.05.2024. But an order was passed dated 29.08.2024 post the maximum period of limitation as provided u/s 73 of the act. It was furnished by the applicant that no force majeure norms existed. No notification can have been passed in the absence of these conditions. Beyond the same, they claimed that even the COVID-19 relaxations/extensions are not available since the same lasted until 28.02.2022.

The decision of Several High Court were mentioned to support their arguments. In the case of Graziano Transmissions v. Goods and Services Tax, the Allahabad High Court, inter-alia, opined that orders of the Supreme Court in suo motu jurisdiction relaxing limitation are not applicable for proceedings under the GST Act.

The applicant placing reliance on the same ruling also specified that the court marked that the impugned notification was issued as per the decision of the GST implementation committee and not via the GST council. However, it fails to address the difference between the ‘recommendation of committee’ and ‘ratification by Council’.

The Gauhati High Court in M/s. Barkataki Print and Media Services, Dhrubajyoti Barkotoku v. Union of India, opined that the recommendation of the GST Council is sine qua non for exercising power u/s 168A of the Act.

The HC in the case of the problem of suggestion and ratification noted that the suggestion of the council does not provide any room as a condition precedent before the government furnishes a notification.

Notification No. 56/23 was issued without there being any suggestion from the Council. Based on the Implementation Committee’s decision the same was passed. Therefore, ‘ratification’ accomplished after issuance of Notification No.56/2023 will not furnish vitality to Notification No.56/2023., it added and reasoned:

“The purpose behind using the phrase ‘on the recommendation of Council’ is to equip the Government with the expert opinion of an expert constitutional body i.e., GST Council. This enables the Government to take an informed decision based on such opinion of Council. Since all the States have participation in the Council, the recommendation of Council will certainly be in consonance with doctrine of cooperative federalism.”

Read Also: Supreme Court Denies Retrospective Benefit for Jeevan Adhar Policy Deposits

The court adverting to the Apex court orders relaxing limitation cited that the directions applied to the laws which stipulated a limitation period and Section 73 was one such provision. The court after scrutinizing the directions passed noted that it can not be cited that the limitation extension was not applicable in the existing proceedings.

Section 168A furnishes for time extension ‘in respect of actions’ which cannot be completed due to force majeure.

“In the manner statute i.e., Section 168A is worded, there is no cavil of doubt that the Law makers intended to give it a broader umbrella to bring within its shadow, such actions which could not be completed or complied with, due to force majeure…The COVID-19 Pandemic created extraordinary difficulties which could not have been anticipated, measured and solved with mathematical precision. Thus, hair-splitting in many aspects must be eschewed…While dealing with such an extraordinary crisis, Government’s action must be viewed in a broad perspective.”

It relied on the Patna High Court decision in M/s Barhonia Engicon Private Limited v. The State of Bihar wherein rejected a petition contesting the notifications extending the timeline for issuance of Orders u/s 73 of the Act.

The High Court in the perspective while disposing of the present set of petitions, noted-

“Thus, the question of validity of notifications pales into insignificance. Since the period between 15.03.2020 to 28.02.2022 stood excluded for the purpose of counting limitation by an order which became law of the land, the remaining argument relating to validity of notifications became academic in nature.”

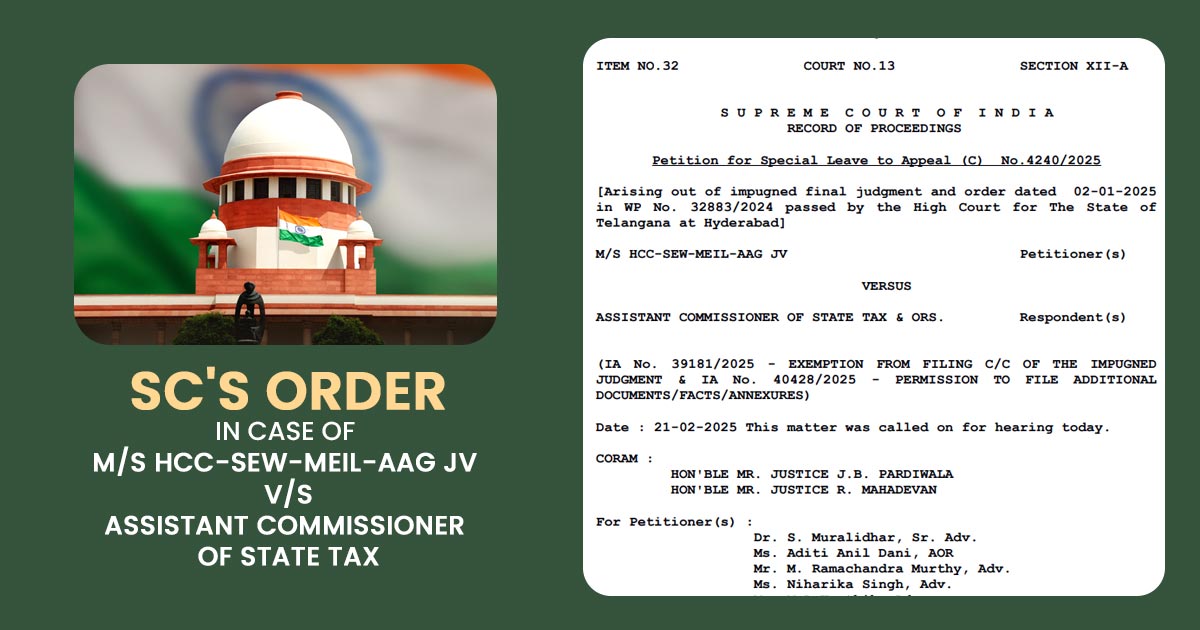

The present petition filed a special leave petition against the same ruling. At the time of the hearing, Senior Advocate Dr. Muralidhar pointed out that there is a cleavage of opinion among different High Courts of the country. Notice was issued by the Apex court to the respondents, returnable dated 07.03.2025.

Appearance for petitioner:

Dr. S. Muralidhar, Sr. Adv. Ms. Aditi Anil Dani, AOR Mr. M. Ramachandra Murthy, Adv. Ms. Niharika Singh, Adv. Mr. M A Karthik, Adv. Mr. Maitreya Subramaniam, Adv. Ms. Pallak Bhagat, Adv.

| Case Title | M/S HCC-SEW-MEIL-AAG JV vs. Assistant Commissioner of State Tax |

| Citation | WP No. 32883/2024 |

| Date | 02-01-2025 |

| Counsel For Appellant | Dr. S. Muralidhar, Sr. Adv. Ms. Aditi Anil Dani, AOR Mr. M. Ramachandra Murthy, Adv. Ms. Niharika Singh, Adv. Mr. M A Karthik, Adv. Mr. Maitreya Subramaniam, Adv. Ms. Pallak Bhagat, Adv. |

| Counsel For Respondent | Advocate K. K. Maiti |

| Supreme Court | Read Order |