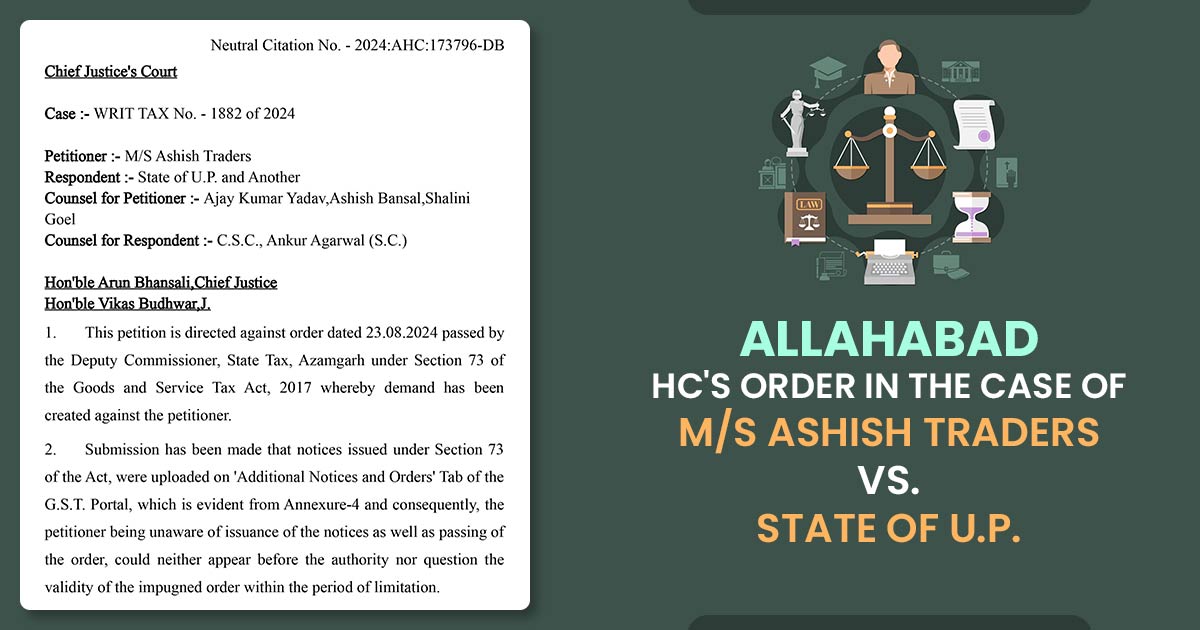

The Allahabad High Court has ruled that fresh notices can be issued to a taxpayer for unpaid taxes under Section 73 of the GST Act, 2017. This can apply only if the taxpayer did not properly understand or miss the initial notices.

This decision, made by a division bench consisting of Chief Justice Arun Bhansali and Justice Vikas Budhwar, refers to the ruling in Ola Fleet Technologies Pvt. Ltd. vs State of UP (2024), in which the court granted the taxpayer a “benefit of the doubt.”

In that case, the initial notices issued did not appear in the expected “view notices and orders” section of the taxpayer’s portal. It raised issues about proper communication.

In the present case, the petitioner questioned a tax demand order issued under Section 73, arguing that the notices had been uploaded in the “Additional Notices and Orders” section of the GST Portal, rather than the standard notices tab. The petitioner claimed, that this made them unaware of both the issuance of the notices and the tax demand order.

In the referenced case of Ola Fleet (supra), the court had remanded back to the authority citing the same facts. In that, the Department argued that the Assessing Officer lacks the ability to control how orders appear under specific tabs visible to the taxpayer.

However, the Allahabad High Court emphasized the importance of appropriate communication, noting that the issue at hand was due notice of the disputed order dated July 12, 2023.

The petitioner claimed the order was not visible in the “view notices and orders” tab but appeared under “additional notices and orders,” which supported the claim for the ‘benefit of the doubt’.

Following this, the court granted the petition in the current case and ordered the Assessing Officer to issue a new notice to the petitioner. This notice must provide at least 15 days’ clear notice and be communicated in accordance with the law.

| Case Title | M/S Ashish Traders vs. State of U.P. |

| Citation | Writ Tax NO. – 1882 Of 2024 |

| Date | 06.11.2024 |

| Counsel for Petitioner: | Ajay Kumar Yadav, Ashish Bansal, Shalini Goel |

| Counsel for Respondent : | C.S.C., Ankur Agarwal |

| Allahabad High Court | Read Order |