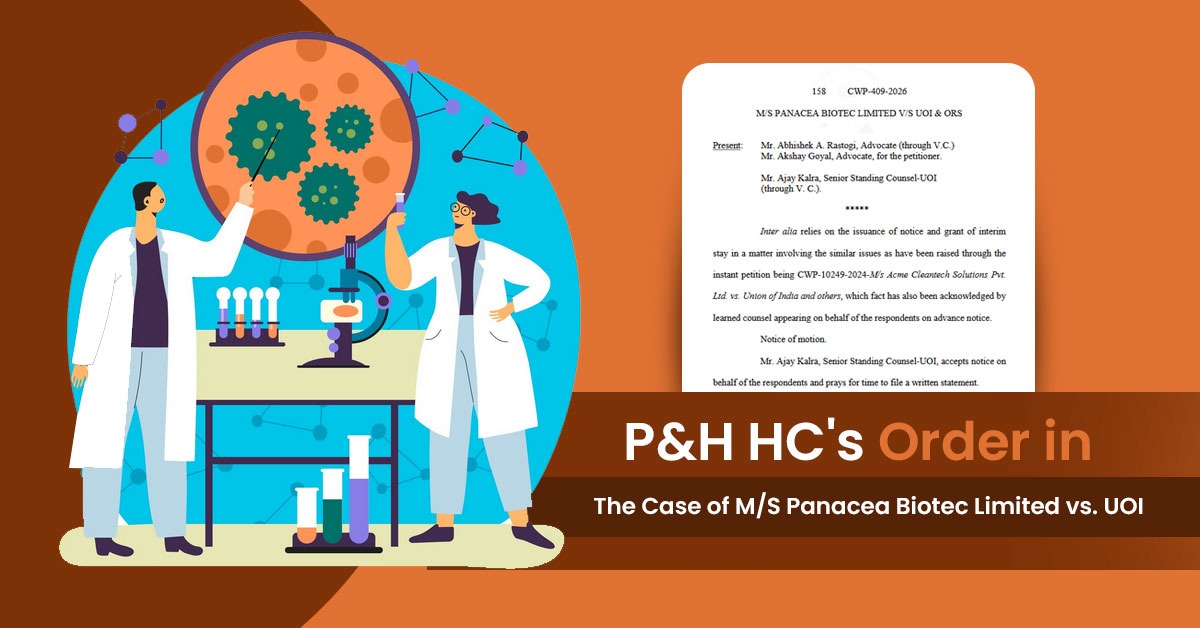

The Punjab and Haryana High Court has provided interim relief in a case that questions the imposition of Goods and Services Tax (GST) on corporate guarantees. This decision has temporarily prevented any coercive measures from being taken against the petitioner involved in the case.

Asking for relief, Panacea Biotec approached the High Court. The applicant’s representative, Abhishek A Rastogi, advocate, along with Akshay Goyal, while Ajay Kalra, senior standing counsel, represented the Union of India.

The legal case currently under consideration addresses the question of whether Goods and Services Tax (GST) can be applied to corporate guarantees that were issued before the amendment of Rule 28(2) of the CGST Rules. This amendment, which was implemented following recommendations from the GST Council, introduces a deemed valuation mechanism that limits the GST charge to 1% of the guaranteed amount.

Rastogi, appearing for the applicant, said that the revision to Rule 28(2) is prospective and could not be applicable to corporate guarantees issued before its legislation. He stated that any attempt to charge GST for an earlier duration shall be beyond legislative competence and executive authority.

Also, he mentioned that in this case, the tax authorities had asked to value the alleged service at 2.5%, which is higher than the 1% cap subsequently proposed via the GST council. He stated that the same approach was arbitrary and unreasonable, both because it sought to tax transactions that consist of no consideration and because it charged a valuation higher than what the GST framework now identifies as relevant.

The Court acknowledges a similar case pending before it, submitted via Acme Cleantech Solutions, where the notice had earlier been given and interim relief granted. The bench issuing the notice of motion asked that no coercive measure be opted against Panacea Biotec in the circumstance that a final assessment order is passed or a demand is raised.

Also Read: Madras HC Quashes GST Demand on Corporate Guarantee Over Ignored CBIC Circulars

The court has postponed the case until May 5, allowing the Union of India time to submit its response. Tax experts believe that this order provides necessary clarity on a controversial issue that has imposed significant compliance and financial burdens on businesses, especially in cases concerning related-party transactions where corporate guarantees are provided without consideration.

The interim stay offers immediate relief to multinational corporations and corresponding entities that regularly extend corporate guarantees to their affiliates.

The Court, restraining the coercive measure, has recognised serious legal concerns of the retrospective GST application, particularly for guarantees issued before the amendment of Rule 28(2), when no valuation structure existed, he added. The rollout of the deemed valuation procedure, capped at 1%, could not automatically explain the tax demands for earlier transactions.

Read Also: Punjab & Haryana HC Directs GST Officials to Record Statements on Premises with Counsel Present

The case specifies the requirement for certainty and consistency in GST valuation rules, especially for intra-group arrangements that are more like shareholder support than a commercial supply.

| Case Title | M/S Panacea Biotec Limited vs. UOI |

| Case No. | CWP-409-2026 |

| For Petitioner | Mr Abhishek A. Rastogi, Mr Akshay Goyal |

| P&H High Court | Read Order |