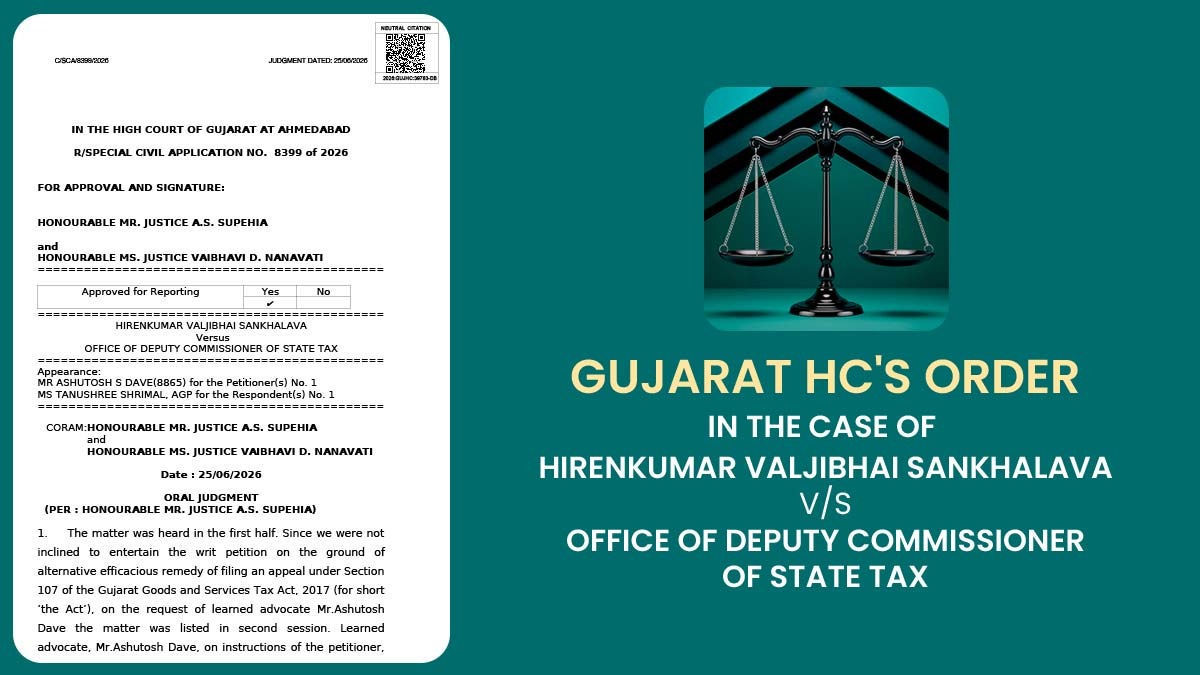

On 25 June, the Gujarat High Court ruled that a taxpayer cannot seek a refund of GST, interest, and penalty voluntarily paid during search proceedings by alleging coercion nearly two years later.

The Court observed that the delayed allegation was merely an afterthought intended to secure a refund. It further held that the delayed issuance of Form GST DRC-04, which acknowledges voluntary payment, did not invalidate the search proceedings or the payment made by the taxpayer.

A Division Bench of Justices A.S. Supehia and Vaibhavi D. Nanavati quashed the writ petition of the proprietor of Alpha-1 Tuition Classes and Hostel contesting the rejection of his refund claim of Rs 1.96 crore u/s 54 of the Gujarat Goods and Services Tax Act, 2017. The Bench said that:

“The conduct of the petitioner during the search proceedings, which went from 06.10.2023 till 10.10.2023, and subsequently demonstrates that he has alleged coercive recovery of tax by the GST Officials as an afterthought in order to claim refund.”

Read Also: Voluntary GST Deposit After Audit Not Enough to Escape Section 74 Action: Patna HC

The proprietor of Alpha-1 Tuition Classes and Hostel contested the rejection of his refund application, claiming that GST authorities had recovered the amount under duress at the time of the search.

Between 6 October 2023 and 10 October 2023, a search was performed by the GST authorities. In the search, they seized documents, recorded statements, and accepted payment of Rs. 1.96 crore towards tax, interest, and penalty through a temporary GST registration.

Approximately two years later, the applicant applied for a refund, alleging that the authorities had extracted the payment via threats and coercion.

The petitioner then said that the authorities denied his refund application without initiating proceedings under Sections 73 or 74 of the Gujarat Goods and Services Tax Act, 2017.

These sections provide for the determination of tax that was not paid, underpaid, or wrongly availed of the input tax credit. He claimed that the authorities issued Form GST DRC-04 almost two years after he made the payment, which rendered the proceedings illegal.

The State mentioned that the panchnamas and statements recorded at the time of the search exhibited that the applicant had voluntarily considered his tax liability, requested a temporary GST registration to make the payment, and never complained of coercion until he submitted the refund application nearly two years later.

The HC, considering the submissions of the State, said that the applicant had acknowledged collecting fees partly in cash without getting GST registration, accepted the quantified tax liability, and said that he had made his statement voluntarily without any pressure, threat, or coercion.

The Court said that such contemporaneous records undermined his allegation of coercive recovery. On the problem of late issuance of Form GST DRC-04, the Bench said that.

“The issuance of FORM DRC 04 under Rule 142 of GST Rules is an acknowledgement of voluntary payment of outstanding tax liability. There is no specific time limit provided under the Rules for issuance of DRC 04.”

Thereafter, the Court said that Section 54 of the Act allows a refund merely where tax was not payable or where the taxpayer paid tax in excess. It was observed that the applicant had opted to seek a decision on the merits rather than claiming the statutory appellate remedy u/s 107 of the Act.

Subsequently, the HC set aside the writ petition, holding that the applicant had voluntarily released his acknowledged tax liability and hadn’t proved any entitlement to a refund.

| Case Title | Hirenkumar Valjibhai Sankhalava vs. Office of Deputy Commissioner of State Tax |

| Case No. | APPLICATION NO. 8399 of 2026 |

| For Petitioner | MR Ashutosh S Dave |

| For Respondent | MS Tanushree Shrimal |

| Gujarat High Court | Read Order |