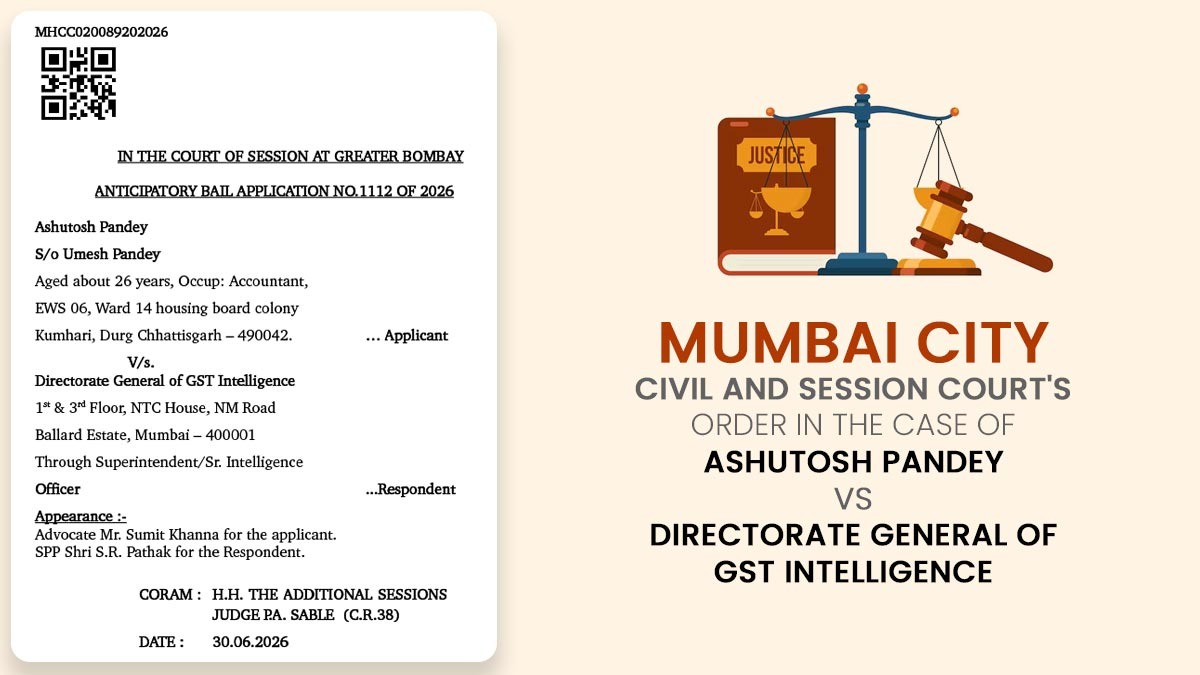

The Court of Session at Greater Bombay has not accepted the anticipatory bail appeal of an accountant in a bogus GST ITC case under section 132 of the CGST Act, 2017.

The Court said that criminal liability under the CGST law is not confined only to directors or people handling the company when the material collected in the investigation displays active participation in the alleged offence.

Also Read: Easy to Understand 21 Offences, Penalties and Appeals Under GST

Under section 482 of the Bharatiya Nagarik Suraksha Sanhita, 2023, applicant Ashutosh Pandey asked for anticipatory bail. The applicant said that he was not the director of Drishti Steel Company or SKDK Steels Private Limited.

He stated he was just working as an accountant-support staff with Drishti Steel Company and had no position in the company’s management or decision-making.

The counsel said that no vicarious criminal liability can be levied on an employee just because of his employment. They claimed that the applicant had not done any illegal act and that no custodial interrogation was needed.

The Directorate General of GST Intelligence countered the appeal. The prosecution claimed that the investigation was pertinent to the fake claim and usage of ITC and was not confined only to SKDK Steels Pvt. Ltd.

They said that statements of witnesses display that the petitioner managed buyer verification, transportation arrangements, maintenance of sales records, and OTP-based GST and banking transactions.

The prosecution stated that the investigation revealed a well-organised network where invoices were generated without any actual movement or supply of goods. It was also claimed that numerous suppliers and intermediary businesses had acquired GST registrations by submitting forged electricity bills and other fabricated documents.

The Court said that the applicant was engaged in buyer verification, sales records, transportation arrangements, GST registration activities, and banking operations via OTP authentication. Such operations had a direct link with the transactions under investigation.

Additionally, the court noted that the allegations involved fake GST Input Tax Credit (ITC) amounting to approximately Rs. 20.30 crore, stemming from fake invoices of over Rs. 100 crore. It emphasised that economic offences impact the financial interests of the State and should be treated with utmost seriousness.

The Court said that the investigation was in an important phase and custodial interrogation was required to discover the role of each person, the creation of alleged fake firms, and the trail of fraudulent ITC. The court therefore ruled that the applicant had not presented a sufficient argument for anticipatory bail and denied their request.

| Case Title | Ashutosh Pandey vs Directorate General of GST Intelligence |

| Case No. | Anticipatory Bail Application No.1112 of 2026 |

| For Petitioner | Mr Sumit Khanna |

| For Respondent | SPP Shri S.R. Pathak |

| Mumbai Sessions Court | Read Order |