The Bangalore bench of the ITAT (Income Tax Appellate Tribunal) stated that the tax credit refusal only on the basis that it was not availed in the original income return is unsustainable in law.

The taxpayer, Vinayaka S Veerabasappa, filed an income return for AY 2020–21 reporting income of Rs 17,78,409. During return filing, the taxpayer did not claim credit for tax deducted at source (TDS), which produced a demand of Rs. 3,31,870 being raised by the Centralised Processing Centre (CPC) under section 143(1) of the Income Tax Act.

Consequently, the taxpayer submitted a rectification application under Section 154 of the Income Tax Act, requesting the approval of the TDS credit. The Assessing Officer subsequently recalculated the income in accordance with Section 143(1) of the Income Tax Act and issued a rectification order.

The Commissioner of Income-tax (Appeals), on appeal, said that the rectification order did not improve the income or change the refund evaluated u/s the Commissioner of Income-tax (Appeals) and thus, the appeal was not kept u/s 246A of the Income Tax Act. The dissatisfied taxpayer has filed an appeal before the Tribunal.

The taxpayers said that they did not claim credit for tax deducted at source (TDS) by the employee at the time of filing the original income return u/s 139(1) of the Income Tax Act. The TDS related to the claim is duly reported in Form 26AS for the relevant assessment year.

The taxpayer cited that it had submitted a rectification application u/s 154, asking for the correction of the intimation issued u/s 143(1), wherein the TDS credit was claimed afterwards. It was argued that the revenue does not dispute that the income on which TDS was deducted was duly offered to tax in AY 2020–21. Also, there is no dispute about the availability of the related tax credit in Form 26AS.

The income on which TDS was deducted was earlier offered to be taxed in the return, and thus, a credit refusal only because of the omission in the return shall not be correct. Reliance was placed on the decision of the Co-ordinate Bench in DCIT v. Ravi Integrated Logistics (India) Pvt. Ltd.

Read Also:- Bangalore ITAT Grants INR 1.82 Crore Relief to Seller on Mango Sale

The bench of Balakrishnan S, Accountant Member and Soundararajan K, Judicial Member, said that “Since the assessee has not claimed while filing the original return of income, the tax credit cannot be denied to the assessee who has claimed while filing the rectification petition under section 154 of the Income Tax Act. The Revenue cannot be unjustly enriched by denying the tax credit to the assessee, which violates Article 256 of the Constitution, which prohibits the levy of tax collected except by authority of law”

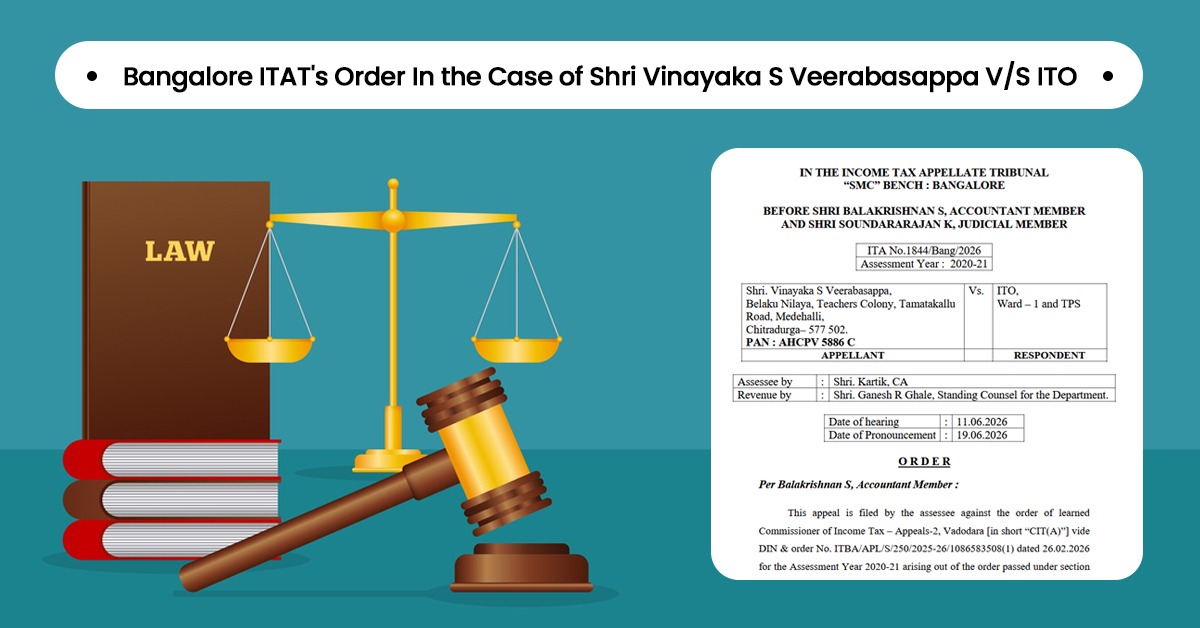

| Case Title | Shri Vinayaka S Veerabasappa V/S ITO |

| Case No. | ITA No.1844/Bang/2026 |

| Counsel For Appellant | Shri. Kartik, CA |

| Counsel For Respondent | Shri. Ganesh R Ghale |

| Bangalore ITAT | Read Order |