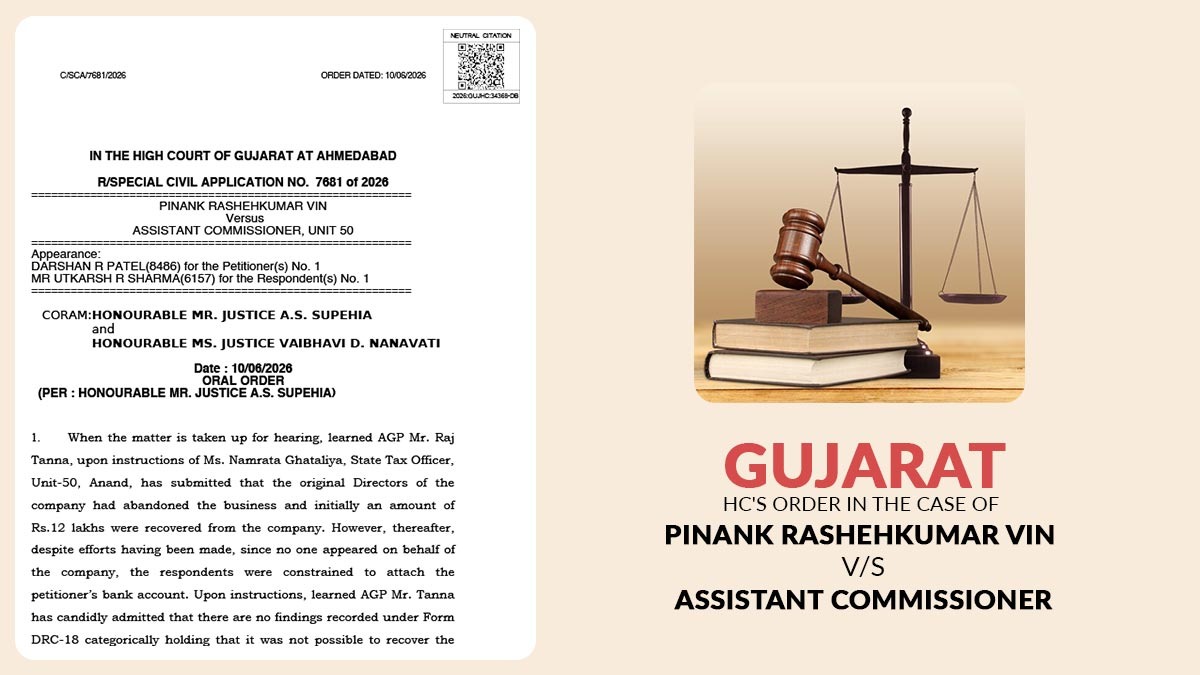

The Gujarat High Court has set aside the GST Department’s bank attachment, holding that recovery cannot be made from a director without prior notice under Section 89 of the CGST Act.

The bench of Justice A.S. Supehia and Justice Vaibhavi D. Nanavati asked the State GST authorities to release the bank accounts, fixed deposits, and demat account of an individual taxpayer, after determining that the department did not record the required findings before commencing recovery proceedings against him for the dues of a company. If there was no categorical determination that recovery from the company itself was impossible, the attachment could not be kept.

The case emerged when the recovery proceedings had started by the GST authorities against a company whose directors had allegedly abandoned the business. Before the Court, the submissions specified that the department had initially recovered nearly Rs 12 lakh from the company. The additional attempts to recover the outstanding dues did not succeed, and no counsel has supported the company; the authorities moved to attach the bank account and other financial assets of the applicant.

Read Also: Andhra Pradesh HC: GST Recovery via Bank Allowed Without Notice if Dues Finalised

The applicant contested the attachment before the Gujarat High Court via a Special Civil Application, claiming that the recovery action against him was opposite to law.

The State’s counsel, following the State Tax Officer’s directions, acknowledged a key point in court.

The department considered that no findings were recorded in Form GST DRC-18, particularly citing that recovery from the company was not feasible and that the authorities were thus forced to recover the amount from the applicant. The State then said that a chance must be provided to the authorities to opt for proper legal recourse against the responsible directors if needed.

The same admission became important as GST recovery proceedings against directors or other persons related to a company need compliance with regulatory safeguards and appropriate recording of reasons before shifting liability beyond the company itself.

The bench, after observing the admission of the department, stated that the requisite findings had not been recorded before proceeding against the applicant.

As per the facts, the Court determined it correct to grant relief to the applicant and asked for the immediate release of the attached financial assets.

The HC ordered the GST authorities to release within 2 days the attachment over: the applicant’s bank account maintained with Kotak Mahindra Bank; two fixed deposits; and the demat account of the applicant.

The direction of the court restored the applicant’s access to his financial assets, which had been frozen under recovery proceedings.

Important: How GST Return Software Handles Notices & Hearings Easily U/S 73

The court granted relief to the applicant and mentioned that its order shall not prevent the GST authorities from seeking lawful recovery measures subsequently.

The Bench granted liberty in the department’s favour to opt for the correct measure in accordance with law for recovery of the outstanding dues from the company itself or from the responsible directors, if legally allowable.

| Case Title | Pinank Rashehkumar Vin Versus Assistant Commissioner |

| Case No. | 681 of 2026 |

| For Petitioner | Darshan R Patel |

| For Respondent | Utkarsh R Sharma |

| Gujarat High Court | Read Order |