In an advisory dated August 28, 2025, the Goods and Services Tax Network (GSTN) stated that the GST system has been enhanced to allow taxpayers to claim refunds when individual components (minor heads) of a GST demand column show negative balances, provided the overall cumulative balance is zero or positive.

Advisory helps small businesses and others by unlocking capital locked in the GST system, as they can not get a refund.

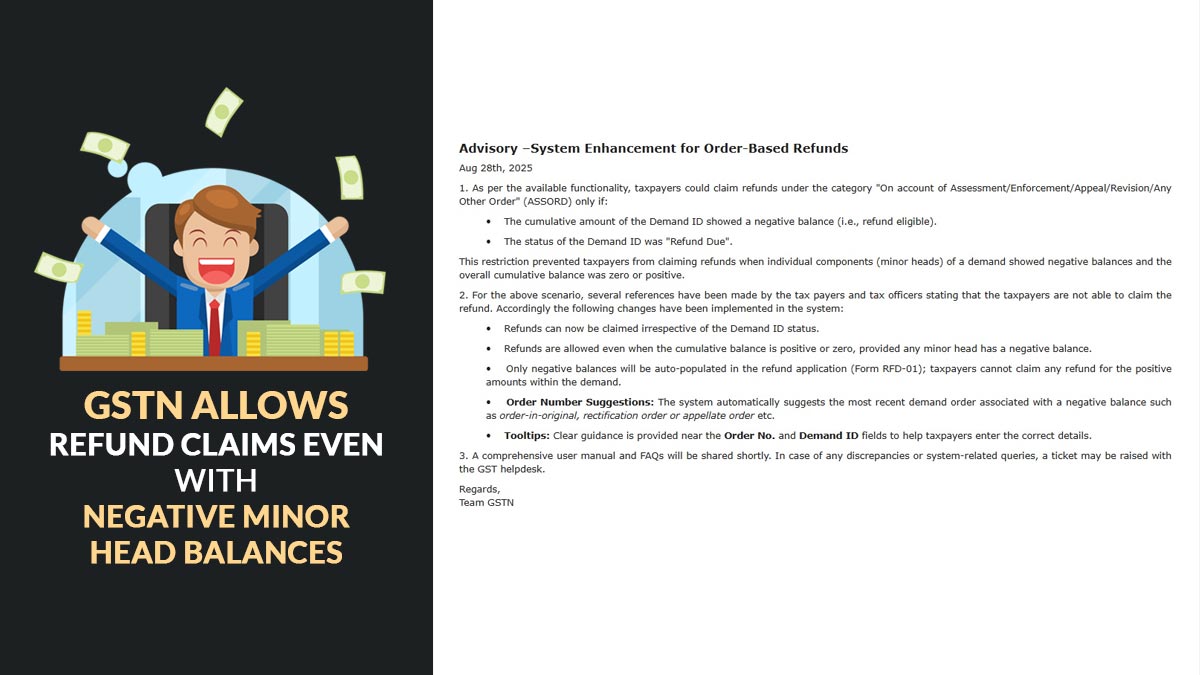

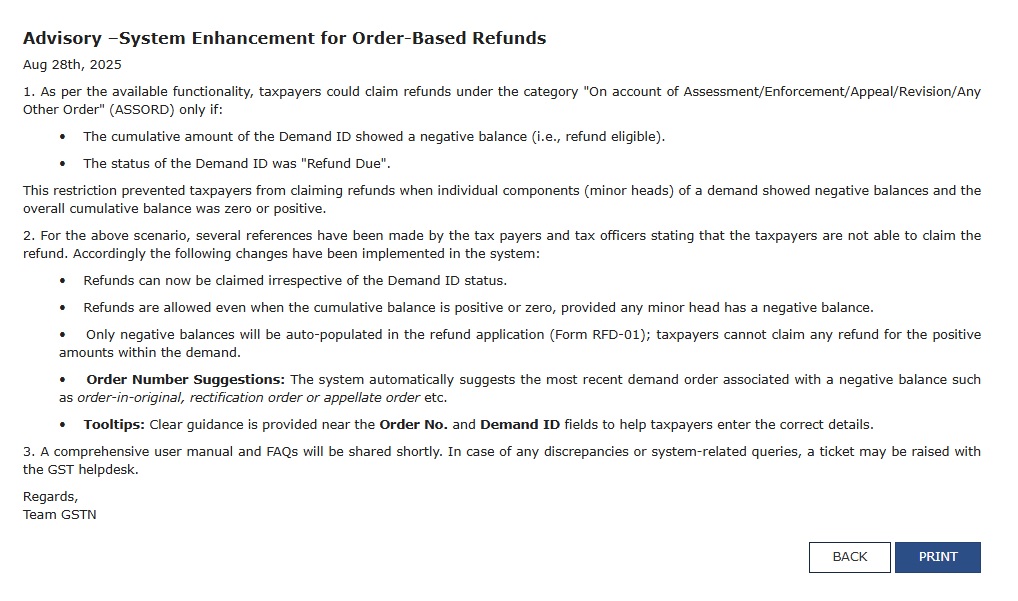

GSTN Advisory About GST Refunds

On August 28, 2025, GSTN in the advisory cited that-

1. Under available functionality, taxpayers can claim GST refunds under the category “On account of Assessment/Enforcement/Appeal/Revision/Any Other Order” (ASSORD) only if:

- The cumulative amount of the Demand ID showed a negative balance (i.e., refund eligible).

- The status of the Demand ID was “Refund Due”.

Taxpayers cannot claim the refunds from this restriction, as when individual components (minor heads) of a demand indicated negative balances and the overall cumulative balance was zero or positive.

2. Towards the cited cases, the taxpayers and tax officers have made distinct references, citing that the taxpayers are unable to claim the refund. As per that, the below-mentioned amendments have been executed in the system-

- Refunds can now be claimed irrespective of the Demand ID status.

- Refunds are permitted even when the cumulative balance is positive or zero, given that any minor head has a negative balance.

- Exclusively negative balances will be auto-populated in the refund application (Form RFD-01); taxpayers cannot claim any refund for the positive amounts within the demand.

3. Order Number Suggestions: The system automatically recommends the recent demand order of the negative balance, like the order in the original, rectification order, or applicable order, etc.

Tooltips- Clarity has been furnished near the Order No. and Demand ID fields to support taxpayers in entering the appropriate details.

GSTN cited that: “A comprehensive user manual and FAQs will be shared shortly. In case of any discrepancies or system-related queries, a ticket may be raised with the GST helpdesk.”

The refund expectation when the individual components (minor heads) of a GST demand column specified negative balances, and the overall cumulative balance was zero or positive, was an anticipation of the trade for a long time. Because of the technical constraint, despite positive orders, a significant amount was blocked. The same advisory and system amendments shall support the trade by eliminating the excessive working capital blockage. The manual and FAQs will be shared as soon as possible.

What Issues with GST Refunds Does This Advisory Address?

The GST refunds issue was when the minor heads of the GST demand (like CGST, SGST, IGST, etc) exhibited a negative balance, i.e, had a tax demand, though the other heads of the GST demand had a positive (refund) or zero balance, then the portal was not permitting the GST refunds for the positive balance.

For instance, if a taxpayer had a Rs 110 positive balance in a head of GST demand, but in one of the heads, it was a Rs 20 tax demand, so the portal was not allowing a GST refund for the Rs 110 amount.

Eligibility for GST Refund

As per the GST Council brochure, below are the conditions when you can claim a GST refund:

- A refund claim may arise towards

- Finalisation of provisional assessment;

- Refund of pre-deposit;

- Tax paid in excess/by mistake;

- Export of goods or services;

- Refund of taxes on purchases made by the UN or embassies, etc., under Section 55 of the CGST Act, 2017;

- Supplies to SEZ units and developers;

- Supply of goods regarded as Deemed Exports;

- Refund arising on account of judgment, decree, order or direction of the Appellate Authority, Appellate Tribunal or any court;

- Refund of accumulated GST Input Tax Credit on account of inverted rate structure;

- Refund on account of any other reasons.

- Refunds to International tourists of GST paid on goods in India and carried abroad at the time of their departure from India (not notified yet);

- Refund of tax paid in the wrong head under Section 77 of the CGST Act, 2017 & Section 19 of the IGST Act, 2017 (treating the supply as intra-State supply which is subsequently held as inter-State supply and vice versa);

GST Council’s brochure stated: “Thus, practically every situation is covered. The GST law requires that every claim for refund be filed within 2 years from the relevant date.”