As per the Delhi High Court, an Assessing Officer (AO) cannot compute the other taxpayer’s income in a matter where no addition is made on account of the causes for which the reassessment under section 147 of the Income Tax Act 1961 was initiated.

Section 147 provides the authority to the AO to calculate or reassess the income and any additional income when he has the cause to assume that any income leviable to tax has not undergone the assessment for any assessment year.

In grudge in the case emerges concerning to power to assess any other income. Explanation 3 to the provision, inserted by the Finance Act, 2009, states that the Assessing Officer(AO) might assess or reassess the income that he observed in the course of the proceedings, in spite that the reasons for these issues were not comprised in the reasons recorded.

In this matter, the taxpayer claimed that the addition of Rs 6,01,00,000 as a security premium to its Income was unsustainable as the reassessment notice furnished to it merely related to the transaction in which the taxpayer has allegedly obtained a sum of Rs 88,00,000 from distinct entities though no addition was made concerning that by the AO.

In the favour of the taxpayer, ITAT ruled. Therefore the revenue has preferred the same appeal. The taxpayer argued that no addition has been incurred for the causes on the grounds of which the assessment reopening was upheld, no additional addition was allowed.

Read Also: No Reopening of Assessment if Limitation Expired Before Timeline Extension

It laid on the Ranbaxy Laboratories Limited v. CIT (2011) where the High Court interrupted the import of the word “and also any other income chargeable to tax” and had concluded that additional income can be drawn to tax furnished an addition was made based on which the assessment was reopened.

Agreeing, the division bench of Justices Vibhu Bakhru and Swarana Kanta Sharma observed, “It is well established that Section 147 of the Act enables the reopening of concluded assessments only in exceptional cases, where there the AO has reason to believe that Assessee’s income for the relevant period has escaped assessment. It is a trite law that concluded assessment should not be lightly interfered with. If the ground on which the concluded assessment is sought to be re-opened, cannot be sustained, there would be little rationale for expanding the reassessment proceedings. In our view, it would not be apposite to accept an expansive interpretation of the provision of Section 147 of the Act. Given that the nature of the proceedings is to unsettle concluded assessment, a strict interpretation of the plain language of Section 147 of the Act, is warranted. “

It mentioned ATS Infrastructure Ltd. vs. ACIT (2024) in which it was carried that if in the course of proceedings u/s 147 the assessing officer arrived at the conclusion that certain items did not undergo assessment, then despite those items were not comprised in the reasons to assume as recorded for initiation of the proceedings and the notice he shall be qualified to perform the assessment of such items.

But the legislature cannot be assumed to have intended to provide the blanket powers before the assessing officer that on assuming the jurisdiction u/s 147 for the assessment or reassessment of the escaped income he shall maintain on making roving inquiry and hence comprising the distinct items of the income not linked or pertinent with the causes to assume, based on which he assumed jurisdiction.

Subsequently, the court proceeded to regard Explanation 3 and observed that it just specified that the AO shall compute or reassess the income for the issue that has not undergone assessment and these additional problems that came to the notice thereafter.

Read Also: Quick Guide to Income Tax Section 148A with New Changes

It also mentioned that the cited explanation does not regulate the import of the plain language of section 147 of the act.

The court marked that “Explanation 3 to Section 147 of the Act, merely clarifies that the jurisdiction of the AO was not confined to assessing or reassessing of the income of an Assessee only in respect of the issue, which formed a part of the reasons recorded for reopening the assessment. The said explanation cannot be interpreted to mean that the AO could assess other incomes of the Assessee even in cases where no addition is made on account of the reasons for which reassessment was initiated.”

It laid on Commissioner of Income Tax v. Jet Airways (I) Limited (2011) where the Bombay High Court carried that Explanation 3 does not and cannot override the prerequisite of satisfying the conditions set out in the substantive part of section 147. Elaboration to a legal provision is objected to explain its contents and could not be interpreted to override the same or direct the substance worthless.

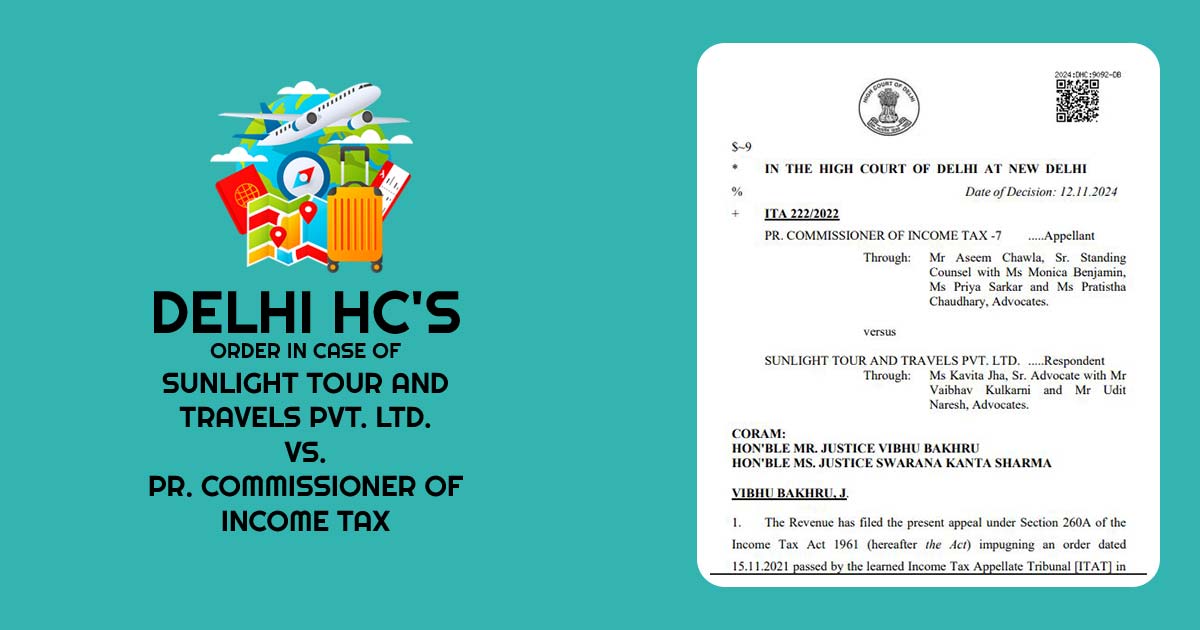

| Case Title | Sunlight Tour and Travels Pvt. Ltd. vs. Pr. Commissioner of Income Tax |

| Citation | ITA 222/2022 |

| Date | 12.11.2024 |

| Petitioner by | Mr Aseem Chawla, Ms Monica Benjamin Ms Priya Sarkar, Ms Pratistha Chaudhary |

| Respondents by | Ms Kavita Jha, Mr Vaibhav Kulkarni, Mr Udit Naresh |

| Delhi High Court | Read Order |