The High Court of Punjab and Haryana, in a ruling, invalidated tax notices issued to the taxpayer, stressing that circulars along with tax authorities guidelines could not override the legal provisions of the Income Tax Act, 1961.

The petitioner-assessee Anju Arora, filed a writ petition contesting the issuance of notices and orders by the Jurisdictional Assessing Officer ( JAO ).

Both counsels agreed that the problem in question had been fully examined earlier and then concluded by this Court in two recent matters: Jasjit Singh vs. Union of India and others ( CWP No. 21509 of 2023 ) decided on 29.07.2024 and Jatinder Singh Bhangu vs. Union of India and others ( CWP No. 15745 of 2024 ) decided on 19.07.2024.

Read Also: Punjab & Haryana HC Cancels Tax Notice for Non-Compliance U/S 144-B(6)

In the Jasjit Singh case, the Court determined that the circulars or directives from the Board should not override statutory provisions or make them ineffective.

It stresses that financial legislation is required to be complied with and that no powers are to be used by the authorities that violate these provisions since the same can cause confusion to assessees and require them to do the hardship.

Directing sections 119, 120, and 144B (7 & 8) of the I Act, it marked that the issuance of the notices by the JAO without the needed faceless assessment u/s 144B was opposite to the act.

Subsequently, in the matter of Jasjit Singh the Court annulled multiple notices and orders that were issued without following these regulations. As per the ruling, it stresses that the board’s instructions and circulars are referred to support and implement the legal provisions rather than override them.

The Court Applying the findings from Jasjit Singh to the present case set aside the notice furnished before the applicant by the JAO u/s 148A(b) dated 21.03.2023, the order under Section 148A(d) dated 07.04.2023, and the notice u/s 148 on 07.04.2023.

The Court ruled that these notices and proceedings were deemed invalid because they did not adhere to the mandatory faceless assessment requirement outlined in Section 144B of the Act.

The court said that the revenue authorities have the freedom to comply with the proper legal procedures under the act if regarded as important. All the due applications were indeed disposed of under the main order.

The Division Bench of Sanjeev Prakash Sharma (Judge) and Sanjay Vashisth (Judge) applied the observations and conclusions from the decision of Jasjit Singh, mutatis mutandis to show the matter permitting the writ petition in the taxpayer’s favour.

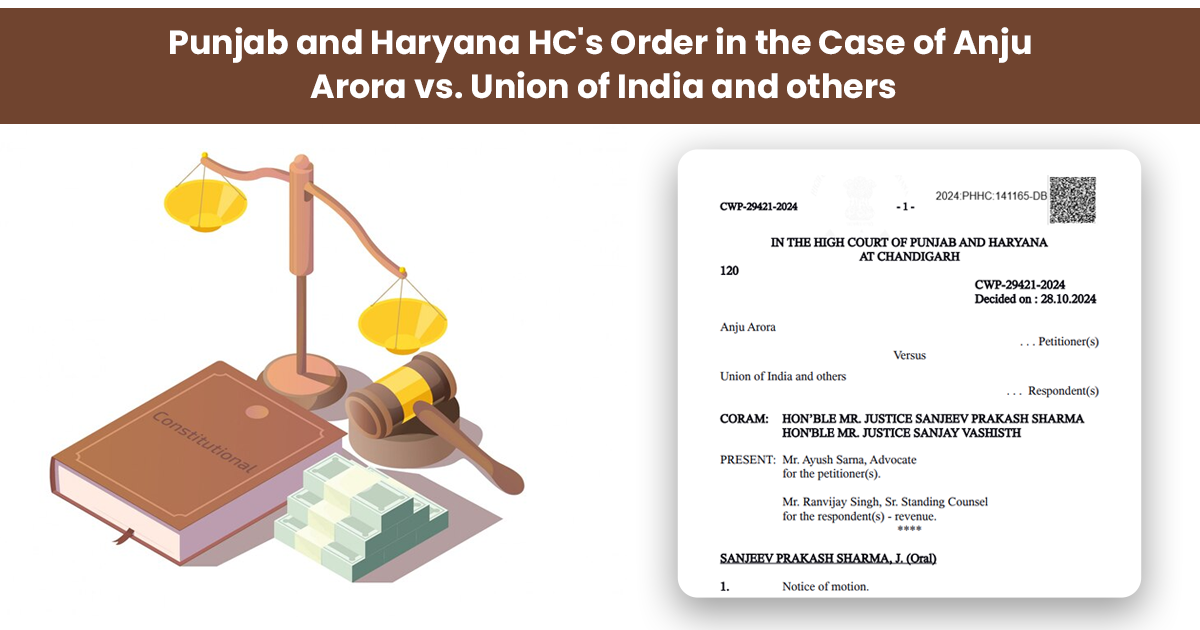

| Case Title | Anju Arora vs. Union of India and others |

| Citation | CWP-29421-2024 |

| Date | 28.10.2024 |

| Counsel For The Petitioner | Mr. Ayush Sarna |

| For the Respondent | Mr. Ranvijay Singh |

| Punjab and Haryana High Court | Read Order |