The new Forms 10B and 10BB that charity or religious trusts, institutions, universities, or other educational institutions must file in line with Sections 10(23C) and 12A of the Income Tax Act have been released by the Central Board of Direct Taxes (CBDT).

Latest Update

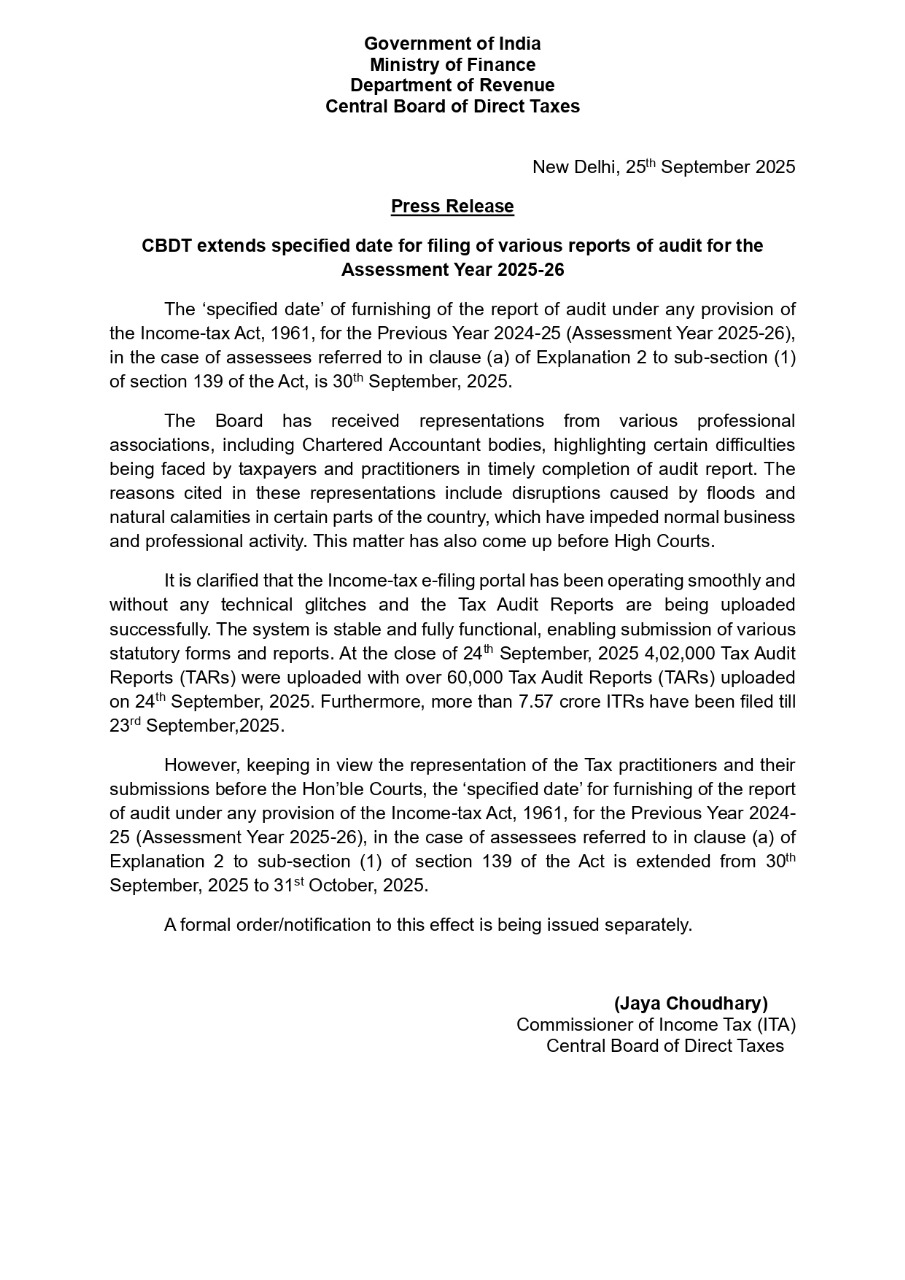

- The CBDT has extended the due date for Forms 10B and 10BB till 31st October 2025. Read More

- Recently, CBDT has given circular No. 16/2024, which allows the filing of forms 9A, 10, 10B and 10BB for condonation of delay. Read circular

- The due date for income tax audit report forms 10B and 10BB is 30th September 2025 for AY 2025-26.

{kind=link}

The income tax amendment (3rd Amendment) rules 2023 would have been notified by the board and it shall come into force from 1st April 2023.

Under Section 12A of the Income-tax Act, 1961, Form 10B is concerned with audit reports, towards the case of fund, trust, or institution, any university or other educational institution, or any hospital or other medical institution.

The audit report of the accounts of a trust or institution would be in e-filing 10B form, which is needed to get filed under subclause (ii) of clause (b) of sub-section (1) of Section 12A.

Form No.10B comprises the total income of the trust or institution excluding providing effect to the provisions of sections 11 and 12 of the act which surpasses Rs 5 cr in the previous year, or these trust or institution has made any contributions from foreign over the previous year or these trust or institution has applied any portion of its income outside of India in the previous year.

Under clause (b) of the tenth proviso to clause (23C) of section 10 and section 12A(1)(b)(ii) of the Income-tax Act, 1961, Form 10BB prescribes for the audit report for the case of the fund, trust, or institution, or any university or other educational institution, or any hospital or other medical institution that is needed to get filed under clause (b) of the tenth proviso to clause (23C) of section 10 or trust or institution which is needed to get filed under section 12A(b)(ii).

In a significant move to ease the process of audit reporting, the income tax department has re-notified Form 10BB with the issuance of notification No. 7/2023 on 21st February 2023.

The same blog furnishes a detailed resolution for the common issues concerning the applicability, filing procedure, and the additional important aspect of Form 10BB for the AY 2023-24 and the next years.

Tax Form 10BB Applicability

From the AY 2023-24 the re-notified Form 10BB is applicable according to notification no. 7/2023 on 21st February 2023.

Previous 10BB Form is Available

- The current Form 10BB is available on the e-filing portal.

- The users could access the same for filings up to the assessment year 2025-26.

Conditions for Tax Filing Form 10BB

Form 10B needs to be filed from AY 2023-24 onwards. If any of the below conditions are satisfied-

- Total income is more than 5 crores Total income is more than 5 crores without giving effect to the provisions of Section 10(23C) (iv), (v), (vi) and (via) the previous year

- The auditee has obtained foreign contributions

- The auditee has applied to any portion of its income outside India

For other cases, the re-notified Form 10BB is applicable. Direct to Rule 16CC and Rule 17B of the Income Tax Rules, 1962 for more information

Implementation of Form 10BB (A.Y. 2023-24 Onwards)

The process of filing comprises the steps for both the assessee and the Chartered Accountants (CAs). It contains assignment, acceptance, and verification. Confirm timely filing to avoid late filing issues.

Overview of Auditee

The term auditee is directed to any fund, institution, trust, university, educational institution, hospital, or medical institution cited in particular clauses of section 10 or sections 11 and 12 of the Income Tax Act.

A Brief Explanation of Foreign Contribution

The term “foreign contribution” in the context of re-notified Form 10BB is directed to the definition given in the Foreign Contribution (Regulation) Act, 2010.

Submission Deadline for Tax Form 10BB

Form 10BB should be filed before the defined date mentioned in section 44AB, i.e., one month before the last date to file the return under section 139(1).

Fulfilment of Tax Form 10BB Filing

Filing is deemed complete if the assessee accepts the form uploaded by the CA and verifies it with an active Digital Signature Certificate (DSC) or Electronic Verification Code (EVC).

Verification Methods for Tax Form 10BB

Distinct verification modes are available for CAs and assessee, including DSC and EVC options established on the type of entity.

Applicability of Form 10B and 10BB from A.Y. 2023-24

The amendment rules specify that starting from Assessment Year 2023-24, Form 10B and 10BB are applicable, regardless of the form submitted in the preceding assessment years.

Records Options with Add Details and Upload CSV Format

Clear instructions are outlined for managing schedules containing tables. Users have the flexibility to choose between table or CSV formats for records up to 50, while records exceeding 50 are limited to CSV format.

Modification Option for Form 10BB

Yes, the amendment choice is available to file Form 10BB.

Policies to File Tax Form 10BB

An instruction file can be downloaded by a Chartered accountant at the time of the form-filing procedure under their ARCA login.

Document Required to Attach Tax Form 10BB

Necessary attachments consist of the Income and Expenditure Account/Profit and Loss Account, as well as the Balance Sheet. An optional section for “Miscellaneous Attachments” is provided.

Considering Filed Details in Tax Form 10BB

Details of the filed form can be observed in the e-File tab on the Income Tax portal, accessible for both Chartered Accountant (CA) and taxpayer logins.

Downloading Offline Utility

You can obtain the offline utility for Form 10BB from the Income Tax Department’s website. Make sure to utilize the most recent version accessible on the e-filing portal.

Form Filing Via Third-Party Software

Form 10BB could be filed via ERIs via the “Offline” filing mode.

Applicability of Form 10BB Below Basic Exemption Limit

Refer to pertinent provisions for the applicability of Form 10BB, regarding the basic exemption limit.

Select the Type of Organisation on Tax Form 10BB

Form 10BB offers choices such as fund, trust, institution, university, educational institution, hospital, or medical institution for selection, depending on the nature of the auditee.

Handling the Recommendation Errors

Ensure complete profiles for both assessees and CAs, delete old drafts, and reattempt filing.

Mandatory Info for Spoke Persons in Section 13(3)

Information for the said persons in Sl. No. 28 of form 10BB and Sl. No.41 of form 10B is mandatory, according to Circular No. 17/2023, even if specific conditions in section 13 do not apply.

Generating UDIN for Form 10BB

Starting from Assessment Year 2023-24, generate a UDIN by choosing the relevant Form name on the UDIN portal.

This comprehensive guide seeks to answer diverse queries concerning the re-notified Form 10BB, offering clarity on its applicability, filing procedure, conditions, and other crucial aspects. Taxpayers and Chartered Accountants are urged to follow the guidelines and stay abreast of any updates from the Income Tax Department.