GST composition scheme was implemented under the respective State VAT Laws with conditions applied on eligibility for the scheme accordingly. GST composition scheme assures greater compliance without the requirement of maintaining records. This system is missing in Service Tax laws.

Latest Update

13th October 2022

- The ICAI has shared the second edition of the handbook on the composition scheme for Chartered Accountants. Read PDF

09th July 2022

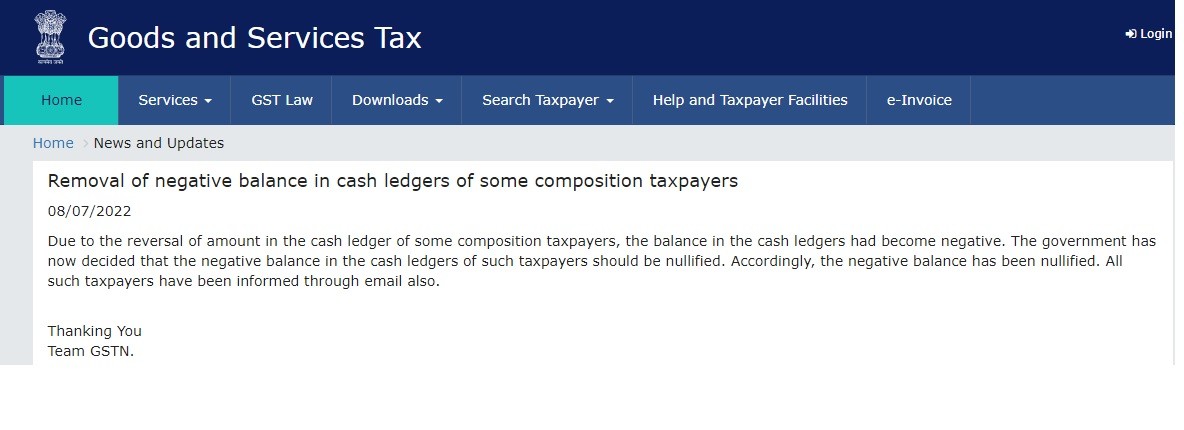

- The important message for some composition taxpayers regarding the negative balance removal is that the process has been completed by the government. read more

09th May 2022

- The Maharashtra Authority of Advance Ruling (AAR) has issued the order for the M/s. KPC Projects Ltd. In the order, Shri T.R.Ramnani and other members said the 18% GST has to be paid for the composite supply of construction hospital works. Read More

GST Software Demo for Composite Taxpayers

32nd Council GST Meeting for Composition Traders

- The annual turnover limit increased by GST council to 1.50 Crores, effectively from 1 April 2019

- Annual filing of GSTR 4 return instead of quarterly. Also, tax is paid to be deposited on a quarterly basis.

- 6 percent GST rate applicable to the Composition scheme for service providers and turnover up to 50 lakh per annum

Note:

- The above amendments shall be applied after the official government notification.

- More: 32nd GST Council Meeting Updates for Composition Traders

Every taxation system has some prescribed rules or regulations which must be followed by individuals, taxpayer or business owners. Maintaining records properly, submission or filing returns timely, simplified generation, and periodic payment of taxes are some of the essential elements of the taxation system for corporate taxpayers. However, business enterprises and owners are facing difficulties to cooperate with such responsibilities of law. It happens just because of a lack of knowledge and the majority of people is not aware of the taxation system.

In 28th GST council meeting, the FM has decided to extend the threshold limit of composition scheme taxpayers from 1 crore to 1.5 crores. Also, included the 10% provision of normal taxpayer annual turnover within the composition scheme if in case the given 10 percent is provided as the service.

Key Features of GST Composition Scheme

Eligibility: – Everyone is not eligible to register under the GST composition scheme. Taxpayers or people whose annual turnover is up to INR 1.5 crore in a financial year. Turnover for special category States, except Jammu & Kashmir and Uttarakhand, the limit is now increased to Rs 75 Lacs. While the turnover threshold for Jammu & Kashmir and Uttarakhand will be Rs 1 crore must register under the GST composition scheme. The small traders should fill up GST CMP-01 form to accept the scheme.

Special Eligibility:- The GST council has included normal taxpayers within the composition scheme in case 10% of annual turnover is provided as a service.

Quarterly Filing Returns: – Instead of submitting returns 3 – 4 times in a month, taxable persons or registered taxpayers will be required to submit or filing tax returns only one time in every quarter under the GST composition scheme.

Intra- State Supplies: – Local suppliers, who supply goods or services within a state can take advantage of the GST composition scheme. Inter-state suppliers will come under the regular GST laws.

Bill of supply, not tax invoice: – Registered taxpayers under the GST composition scheme will be required to show the bill of supply instead of tax invoice to the tax authorities. A person paying taxes under the composition scheme can issue a bill of supply instead of an invoice. Exemptions up to 5 lakhs for services under the composition scheme are also available.

Not Eligible for Input Tax Credit: – According to section 16, goods and services on which composition tax has already been paid (under section 8) do not apply for Input Tax Credit.

Tax Rate: – Manufacturers – 1% ( .5% central and .5% state), Restaurants services – 5% ( 2.5% central and 2.5 state ), Composition levy eligible – 1% ( 0.5% central and 0.5% state )

GST Only on Taxable supplies: – Earlier it was a provision to pay composition GST even on the exempted goods but now after 1st January 2018, the GST will be only payable on the taxable goods.

Penalty: – If the taxable person is not eligible for the GST composition scheme, then the tax authorities can charge a penalty equal to the amount of tax on such person along with his tax liability. Be careful when availing of this scheme and paying taxes. The penalty will be imposed according to the provision of section 73 or 74 if an individual represents incorrect data under the composition scheme.

Voluntary Registrations: – For availing of the benefits of this scheme, taxpayers need to make voluntary registration. If in case, the taxpayer’s annual income turnover exceeds 75 lakh then he will be transferred to the regular scheme. Taxpayers who are already a part of VAT composition need to voluntarily register under this scheme.

Note: The eligibility and service supply exemption is under review after the 23rd GST Council meeting

Highly Recommended: GST Forms: Return Filing, Rule, Registration, Challan, Refund, Invoice

Registration Procedure Under the Composition Scheme

Registered or existing taxpayers not under the Composition Scheme may prefer to opt for it (subject to being qualified), only from the beginning of the next financial year. Tax returns to be filed on as or before 31 March of the previous year.

If in case dealers want to switch to the normal scheme, during the year, they may be allowed to do it. Although, they are not able to switch over to the Composition scheme again within the same Financial Year

Filing Returns Under the GST Composition Scheme

Individuals or registered taxpayers can pay tax under the provisions of Composition Scheme shall provide a return in an official form and official manner within the eighteen days after the end of the relevant quarter.

GST CMP 08 form has been officially declared by the government for depositing payment quarterly under the Composition Scheme.

FAQs on GST Composition Scheme

Q.1 Can a composition dealer purchase goods from an inter-state supplier?

Yes, of course, a person who has opted for composition scheme can procure goods from an inter-state supplier without any restrictions

Q.2 What are the specified composition rates?

Composition rate is uniform for dealers & manufacturers at 1% ( 0.5% Central tax plus 0.5% State tax). Composition rate for Restaurant Services is 5% (2.5% Central tax plus 2.5% SGST) of the turnover. Composition rate for service providers is 3%

Q.3 Is it mandatory for a Composition Dealer to maintain detailed records?

No, it is not mandatory for a registered Composition dealer to maintain detailed records as needed by a normal taxpayer.

Q.4 Is a Composition Dealers allowed to avail Input Tax Credit?

No, Composition dealer is not allowed to avail Input Tax Credit. A taxpayer who opts to pay tax under the composition scheme cannot take credit on his input supplies

Q.5 Is composition dealer responsible to pay both, the Reverse charge and a fixed percentage of normal GST which he is supposed to pay?

If the reverse charge is applicable on a specific supply then the composition dealer is liable to pay GST under reverse charge as a recipient of supply at standard GST rates

Q.6 Can the service provider go for the Composition Scheme?

Yes, Composition scheme for services has been introduced with an initial limit of Rs 50 Lakh, taxable at 6%, beginning from April 1, 2019

Q.7 Can a person avail ITC on the stock after being denied to pay tax under composition from an authorised officer?

Yes a person can still avail ITC by filing a statement in FORM GST ITC-01 (containing details of input stocks along with the inputs contained in semi-finished or finished goods present in stock) on the date on which the option is refused as per order in FORM GST CMP07, within a period of thirty days from the order

Q.8 When does an individual who opted for composition, pay tax?

An individual who opted for composition pays tax on a quarterly basis prior to the 18th* of the subsequent month of the quarter during which the supplies were made (changeable by the government notification)

Q.9 Can a Composition Dealer issue Tax Invoices?

No, a Composition Dealer can not issue a tax invoice because he has to pay the tax out of his own pocket and he is not permitted to recover the same from the customers. He is bind to issue Bill of Supply

Q.10 What are the different types of returns, a Composition Dealer has to file?

A Composition Dealer has to file one return i.e. GSTR-4 on an annual basis, CMP 08 on a quarterly basis.

Q.11 Can a Composition Dealer collect tax from customers?

No, a Composition Dealer has to pay taxes from his own sources and he is not eligible to recover the composition tax from the buyer

Q.12 Can an interstate supplier opt for Composition Scheme?

An interstate supplier can not opt for Composition Scheme as it is available only for dealers imbibed in intra-state supplies

Q.13 How is availed input credit treated when one switch on to Composition Scheme from the normal scheme?

In such a case when a person switches on to composition scheme from normal scheme, he/ she becomes accountable to pay an amount equal to the credit of input tax in terms of inputs present in stock on the day instantly after the date of the switchover. The remaining balance of input tax credit in the credit ledger after payment of such amount will be treated inconsiderable

Q.14 Can I choose for Composition Scheme in one year and flip flop in the later year?

Yes, You are allowed to switch between the Composition Scheme and the normal scheme on the basis of your turnover. The same switchover can be declared on the GST Portal. However, this flip flop comes along with alterations in the way you issue invoices and file your returns

Q.15 Is the alternative to pay tax under composition practicable at any time of the year?

No, the tax under composition cannot be paid at any time of the year. A registered taxpayer is supposed to provide a declaration on the GST Portal in FORM GST CMP-02 prior to the beginning of every financial year

{kind=link}

If I am service provider and wants to pay 6% and wants to take new gst Registration then need to take Registration under Rgular scheme or Composition scheme?

I am a composit dealer and I have agriculture business than what is the gst rate for me.

For composition dealer 1% GST, divided as 0.5% CGST and 0.5% SGST

Rental Income from Commercial property / Building exceeds 20 lakhs. Can I register for composite scheme.

Yes

we are into a composition scheme. We are selling electronics Goods, our turn over comes around 40 lakhs only. but we also need to provide repair services to our customers for electronics goods Which means both Goods and Services.

so please kindly anyone reply to us

“Please consult to GST practitioner”

I am a graphic designer and my company is registered under regular GST tax paying. Now I want to migrate to the COMPOSITION scheme. Am I eligible for the composition scheme?

If your P/Y turnover is below 1.5 Crore, then you can migrate to the composition scheme

yes, you can opt but the threshold limit should be well within the limit specified in the CGST Act 2017

We are a service provider with an FY21 turnover of less than 50 lakhs and have filed returns under a composition scheme.

Our turnover might cross 50 lakhs this year, maybe around Feb’22, but we don’t know as of now. Should we continue filing returns under the composition scheme for FY22?

The turnover limit is seen on the basis of previous year turn over, since FY 21 T/O limit is below the prescribed limit you can file composition return for a whole year

i want to know the tax rate for service provider under Composition Scheme

if you are a provider of restaurant service then it will be 5% otherwise it is 6%

Hi,

Are home-baked dog biscuits exempt from GST? if not, can I apply for a composition GST scheme? Under this scheme, if I sell my product to a retailer within the same state I will give them a bill of supply. But, they are registered under the regular GST scheme so will they give a tax invoice to customers or a bill of supply? and for example, if there is 18% GST on the product then do they have to add that to the bill, claim it from the customer and file the GST? or will they apply 1% GST only since my goods are under the composition scheme? thanks for the help.

Yes, you can apply for a composition scheme, and ITC can not be claimed by a taxpayer who purchases from a composition dealer

A hospital having in patients opted for a composition scheme for medicinal sales. Medicinal sales were Rs. 75 lakh and in patients’ room income was Rs. 50 lakh, since room income was exempted under cgst, 1 % gst was [paid for medicine sales only. for 2019-2020. Is it correct

Dear Sir, please consult the same with practicing Chartered Accountant

in FY 2018-19 total sale under composition scheme 1.45 cr. what is limit composition scheme in fy 201819. Have any problem in this sale ?

1.5Crore

Sir, My turnover is less than 1.5 crore, but I am an Inter-state supplier. Can I opt for composition scheme?

Composition Scheme is available only for dealers doing intra-state supplies. If a dealer is involved in inter-State supplies, then they have to opt-out of the scheme

No you can not go under the composition scheme due to inter state supply

Kindly Re-check Answer / Reply of Q. 6. I think its not properly answered.

Query: Presently a taxpayer is registered is under Regular scheme. He is selling goods as well as providing services. He wants to go for a composition scheme.

My understanding is that for the Goods, the maximum Turnover limit is Rs 1.5 crores and pay GST @1%. For services, the Maximum Limit is Rs 50 Laths and pay tax @6%.

so in total Rs 2 crores, he will get his limit ( For Goods Rs 1.5 cr and for services Rs 50 Lakhs)

Kindly confirm the above understanding.

Gross limit is INR 1.5 crore only not 2 crores

hi sir we are in a plan to start Sarees (clothes) retail business with a small volume may be per annum 50 lakhs approx. we will receive amounts from customers on direct selling product and we will receive amounts from customers which we will take orders from vendors on orders from customers and will pay to vendors and we will have a little margin on that. we need suggestions on a turnover on the second scenario how we can take ?? total customer amount or Diff b/w customer receipt and vendor payment?? plz suggest

For turnover calculation, total receipt from customer will be included

Sir, I have a shop of sweets and also selling Milk in the morning I want to know that can I opt composition scheme and do I pay tax on milk supply under this composition scheme or not?

If your Turnover is below 1.5 crores then only you can opt for Composition scheme

Can a supplier of a works contract having an annual turnover of less than Rs. 50 Lakhs in the previous year, avail Composition Scheme made for service providers?

yes

If a Normal GST Registered person makes a supply to a Composition Dealer then which kind of Invoice he can issue?? B2B or B2C

If he issues B2B invoice then would he be able to submit this supply as a b2b supply against the GST No. of Composit Dealer on the GST portal ??

Pls, answer my query.

B2B, Yes

If a composition person purchase goods from other states, what is the rate of tax, whether this tax is taken for input credit or not, pls explain sir

Composition Taxpayer can not claim any ITC on Input Purchase

Can I able to sell my shop which is in composition tax

Sir I want to open a small software development firm in proprietorship mode and also wants to provide services outside the state but as its is in very small level and my turnover will not go above 10 Lakhs. So my query is can I opt for composition scheme for service provides. Please suggest a good solution beacuse I also want to provide bill to my clients. Awaiting for your help. Regards.

“The tax department has given service providers with a turnover of up to Rs 50 lakh time till April 30 to opt for the composition scheme and pay 6 percent GST. … The GST composition scheme was so far available to traders and manufacturers of goods with an annual turnover of up to Rs 1 crore.”

I mean that I cannot opt for a composition scheme?

Yes

SIR, I AM COMPOSITION DEALER GROUNDNUTS PURCHASE FROM FARMERS AND GROUNDNUTS ISSUES DECORTICATING FOR GROUNDNUT SEED. HOW RATE OF TAX AND REVERSE CHARGE

Please contact to GST practitioner

Hello Sir.

I am working as an interior. And my turnover is around 50 lakh. Since I come under composition scheme. I have only purchase invoices for the last quarter. Can you just help me how do I file for intra-state purchase invoice under composition scheme? Please give me a proper explanation. Thanks

Sir, I would like to start a small hardware cum electrical shop (proprietorship ) under NORKA scheme, can I register my trading business under GST Composition scheme??

shall I apply separate PAN for the firm name or its added to my existing PAN?? How much is the max turnover limit per annum?

Your early reply is highly appreciated. if not can you suggest which type of registration is better for me? I plan to run the business by way of arranging materials from the big suppliers with good discount and sell in a reasonable way.

Since you are planning to start a proprietorship concern, therefore, no separate PAN is required. Turnover limit for composition scheme is Rs. 1 crore.

I AM RICE MERCHANT AND RICE IS EXEMPTED NOW HOW TO SHOW MY SALES UNDER THE CMP08 FORM AND DO I HAVE TO PAY TAX.

if you only deal in exempted goods then you cannot opt for composition scheme under GST. if you deal in both taxable and exempted goods then composition rate is applicable for both taxable and exempted supplies.

I am the proprietor of the boutique and cafe under one roof. I am registered under GST. These are not verticals. Both come under the same PAN-based Gst. Can I charge the appropriate rate of GST on the boutique and take ITC while charging 5% for the cafe/restaurant without ITC? The boutique occupies 1500 sq ft area while the cafe occupies 400sq ft area. Thanking you in advance.

Sir, I have a boutique and a cafe under one roof. I am a proprietor of both. Both are under one PAN and one GST Number. They are not verticals. Can I have the boutique under the general category and take input credit while charging 5% in cafe/restaurant without ITC? Thanking you in advance.

Sir I am a shop owner under regular GST scheme and taking material from a composition dealer. How would I pay GST and on what amount if i purchase from a vendor who is under composition scheme? For eg if I purchase a material from composition dealer @ Rs 60 and sell @ 75. I have to pay GST on 15 Rs margin or on entire 75 Rs?

YOU HAVE TO PAY GST ON RS 75 UNDER COMPOSITION SCHEME.

On Rs75/-

DEAR SIR,

I AM PROPRIETOR OF SMALL SCALE REGISTERED COMPANY ENGAGED IN MANUFACTURING OF CUSTOM BUILD ELECTRONIC ITEMS & ALSO DURING UNDERTAKING LABOR WORKS WHERE IN THE MANUFACTURING COMPANY GIVES GOODS TO US FOR TESTING AND INSPECTION AS SPECIFICATION AND AFTER TESTING AND INSPECTION WE ARE RETURNING THE GOODS TO MANUFACTURING COMPANY MY TURN OVER WILL BE AROUND 5 LAKHS ASE INFORM IF I OPT FOR COMPOSITION SCHEME OF GST WHAT ARE THE TAX LIABILITY FOR LABOUR CHARGES & MANUFACTURING THE ITEMS I WILL BE MUCH OBLIGED FOR YOUR ADVICE IN ADVANCE

REGARDS

SRINIVASAN

I want to convert my monthly return to composition ..so when notification will come to do?

Can Work Contractor get GST registration number under Composition Scheme?

No

me ek vehicle ke spars parts sale karta hu aur bike services karta hu.to kya me nayi provision ke hisab se composition me ja shakta hu. mera turnover 20-25 laks jitna he.please help me.

haa , aap composition scheme opt kr skte but jo aap sale kr rhe h parts ki vo within state hona chahiye.

Yes, you are now eligible to opt for composition scheme. Changes will take effect from 01/04/2019.

I’m E-Commerce Sellers can opt for composition scheme in GST.

Sellers supplying goods through E-commerce operator cannot opt for composition scheme.

Sir, I have taxable supplies of Rs.50 Lakhs and also I have Non-taxable supplies of Rs. 20 Lakhs.

1. What will be the Treatment under GST Act, Shall I pay tax on the whole amount or only taxable amount

2. should I opt for composition levy or under Normal Scheme?

as per the reading of section 10(2), the registered person shall be eligible to opt for composition if he is not engaged in making any supply of goods which are not leviable to tax under this act. Please clear the doubt?

You have to pay tax on the taxable amount only.

You should opt for composition as your turnover do not exceeds Rs. 1 crore

IN 2017-2018, I WAS IN REGULAR SCHEME, I SHOWEN SALES DETAILS IN GSTR 1, BUT NOT SHOWED IN GSTR 3B. UNDER AUTO POPULATED OUR PURCHASE IS MORE THAN SALES. AS THE STOCK IS IN BALANCED. THEN I OPT FOR COMPOSITION SCHEME, WHAT TO DO FOR THE SALES SHOWN IN GSTR 1. IF WE HAVE TO PAY, HOW TO PAY UNDER COMPOSITION SCHEME. WHETHER WE HAVE TO PAY OR NOT.

Under the composition scheme, you have to pay on your turnover(sales) at the applicable rate on you from the period you have opted in for composition.