The applicant bank cannot file its return in its GST portal as a technical issue and cannot be loaded, with demand, penalty, and interest, the Telangana High Court ruled.

The bench of Justice Sujoy Paul and Justice Namavarapu Rajeshwar Rao noted that it was the responsibility of the department to maintain its portal function. If the portal was not functional, the petitioner was forced to file a return in the portal of Telangana. The department cannot take advantage of its own wrong.

The headquarters of the bank of the applicant is in Mumbai, Maharashtra, and the centralized registration of the bank of the applicant is also in Maharashtra under the service tax as well as under the goods and services tax, 2017.

The Goods and Services Tax came into being w.e.f 01.07.2017, and the applicant was qualified to have the credit of Rs. 1,41,26,69,646. The applicant filed the return in the official GST portal of Maharashtra, but due to a technical glitch in the Maharashtra portal, his efforts became useless.

The applicant has a branch in Telangana. On 18.10.2017, he filed the GST returns in the portal of Telangana, took credit on the identical day, and transferred it on the identical day to the portal of Maharashtra.

A pre-show cause notice was been provided to the applicant. The pre-show cause notice alleged that the claimed credit via the applicant by the TRAN-I return filed by the Telangana registration is not eligible and needs to be reversed including the applicable interest and penalty.

A response has been filed via the applicant and made it clear that the total transitional credit was transferred before Maharashtra GST registration on the exact day of filing the GST TRAN-1 and solely the differential balance of ITC was available in the State of Telangana.

On 29.12.2021 a SCN was issued via the respondents and in turn the applicant filed the detailed response. The respondents were unsatisfied with the response to the SCN and passed the order verifying the demand of Rs 1,41,26,69,646 being the irregularly claimed transitioned credit through TRAN-1 in the State of Telangana.

It was argued via the applicant that the SCN mentioned that there were technical issues in the Maharashtra GST portal, and the petitioner filed its return before the last date in the Telangana GST portal and transferred the credit to the Maharashtra portal on the exact date.

Hence the applicant does not under compelling situations and there is no restriction under the act to file the same return electronically in another state in which the branch of the applicant stays. When the applicant does not originate any undue advantage from the act nor revenue suffered any loss. In such cases, the order is poor in law.

It was argued via the applicant that the applicants centralized registration is in the State of Maharashtra. Hence, the applicant must be required to file the return on the GST portal of Maharashtra and not in Telangana.

Read Also: Step By Step Guide: GST Registration Online for New User on GST Portal

Despite believing that the Maharashtra portal has technical issues, the applicant was not remediless, and he must approach the higher authorities of the GST Regime of Maharashtra for the redressal of his grievances.

On the GST portal of Telangana, the applicant is not required to file the return and for the same reason, no fault is revealed in the respondent’s measure. It furnished that in a plain reading of Section 140(1)(4)(8) of the Act, it is evident that the lawmakers of the intention is that the return must be filed in that state where the registration takes place.

Hence the applicant is meritless and might be dismissed. The objective of the centralized registration is to ensure that the facility is not been misused by the parties.

The court is unable to specify that there is any restriction or bar in filing the return via electronic mode in the GST portal of Telangana, where the branch of the applicant exists.

It was ruled via the court that the grounds of the Show Cause Notice are poor within the law and the respondent’s assumption that a return cannot have been filed in the GST portal of Telangana is not flowing from section 140 of the Income Tax Act. Hence the measure established on the same notion is poor within the regulatory and needs to be interrupted.

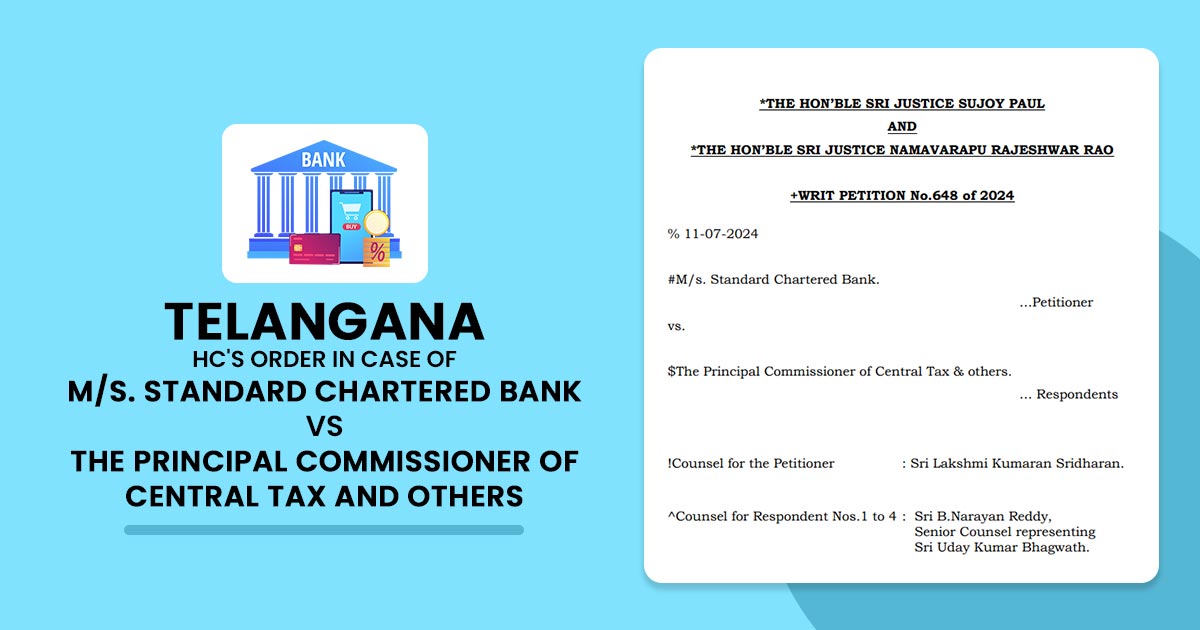

| Case Title | M/s. Standard Chartered Bank Vs. The Principal Commissioner of Central Tax and others |

| Citation | WRIT PETITION No.648 OF 2024 |

| Date | 11.07.2024 |

| Counsel For Appellant | Sri Lakshmi Kumaran Sridharan |

| Counsel For Respondent | Sri B.Narayan Reddy, Senior Counsel representing Sri Uday Kumar Bhagwath |

| Telangana High Court | Read Order |