The Central Board of Direct Taxes (CBDT) on this Wednesday pinpointed that buyers of goods or services shall have to deduct TDS at the source and at 0.1% of the amount that is greater than Rs 50 lakhs when credited or paid to a resident seller on the transactions that have occurred after July 1, 2021, under the section 194Q of the Income Tax Act 1961 that shall be effective from July 1, 2021.

Latest Update

11th April 2022

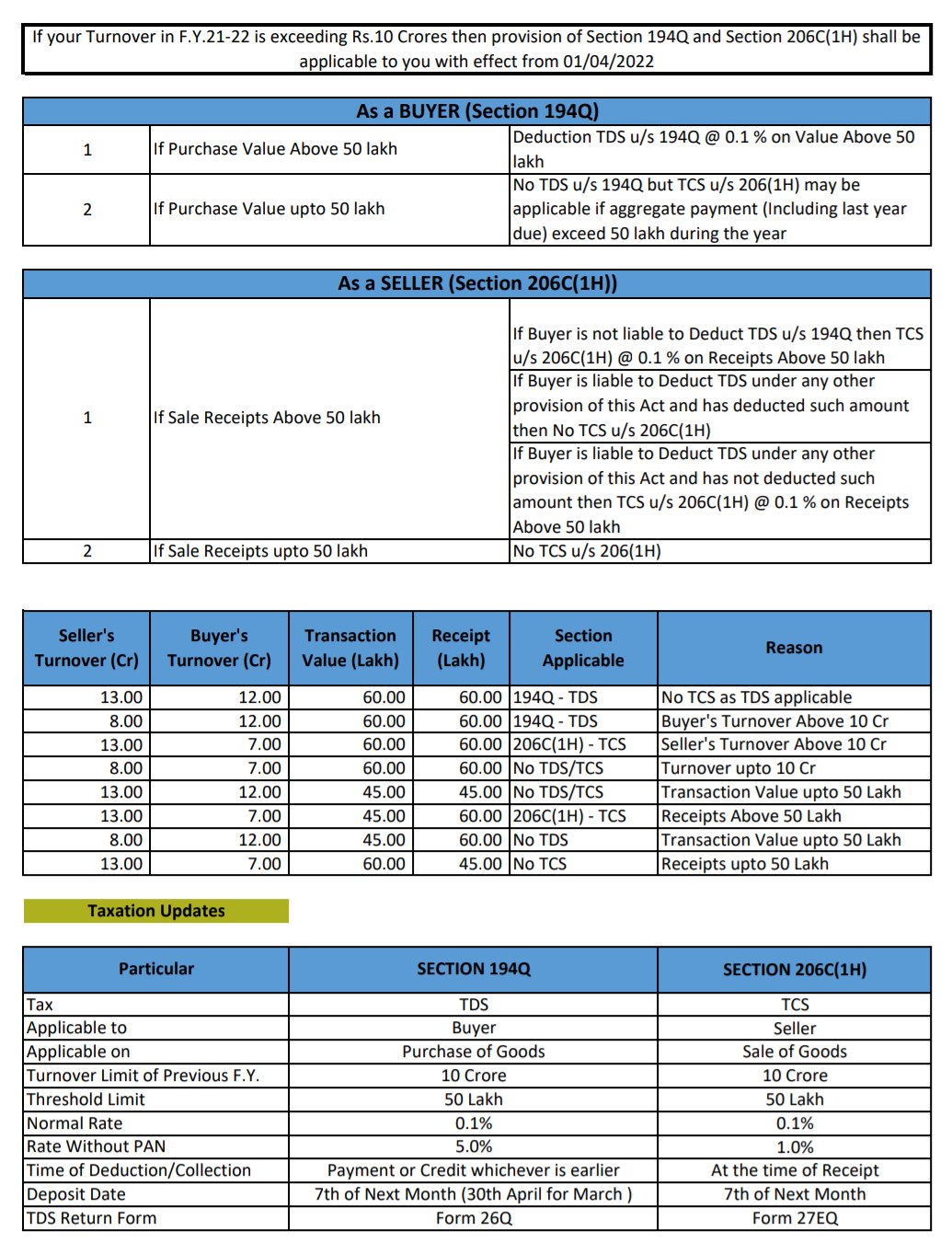

- “According to Section 194Q and Section 206C(1H), if your FY 2021-22 turnover is more than 10 crores then these sections shall be applicable from the 1st of April 2022.”

26th November 2021

- The Income-tax department has issued the circular number 20/2021 related to guidelines under Income tax act sub-section (4) of section 194-0, sub-section (3) of section 194Q, and subsection (I-I) of section 206C required to deduct an amount 1 to 0. 1 % if the income is more than fifty lakh. Read Circular

Try Demo of TDS Return Filing Software!

The Board has specifically pinpointed that the limit of Rs 50 lakhs for the purpose of triggering TDS shall be calculated from April 1, 2021, and the GST component shall have to be set apart at the time of credit. The Board further put clarification that if a transaction comes within the purview of TDS under both section 194O (applicable in the case of e-commerce operators) and section 194Q of the aforesaid Act, deduction shall have to be made as per section 194Q.

Furthermore, when there is a confrontation between the provision of TDS and the provision of TCS wherein goods are sold as per section 206C(1H), provisions of TDS shall apply.

“Addressing the open issues, the circular is just in time and accords much-needed clarity on the subject matter, as the compliance framework becomes effective tomorrow, said Neha Malhotra, director at Nangia Andersen LLP.”

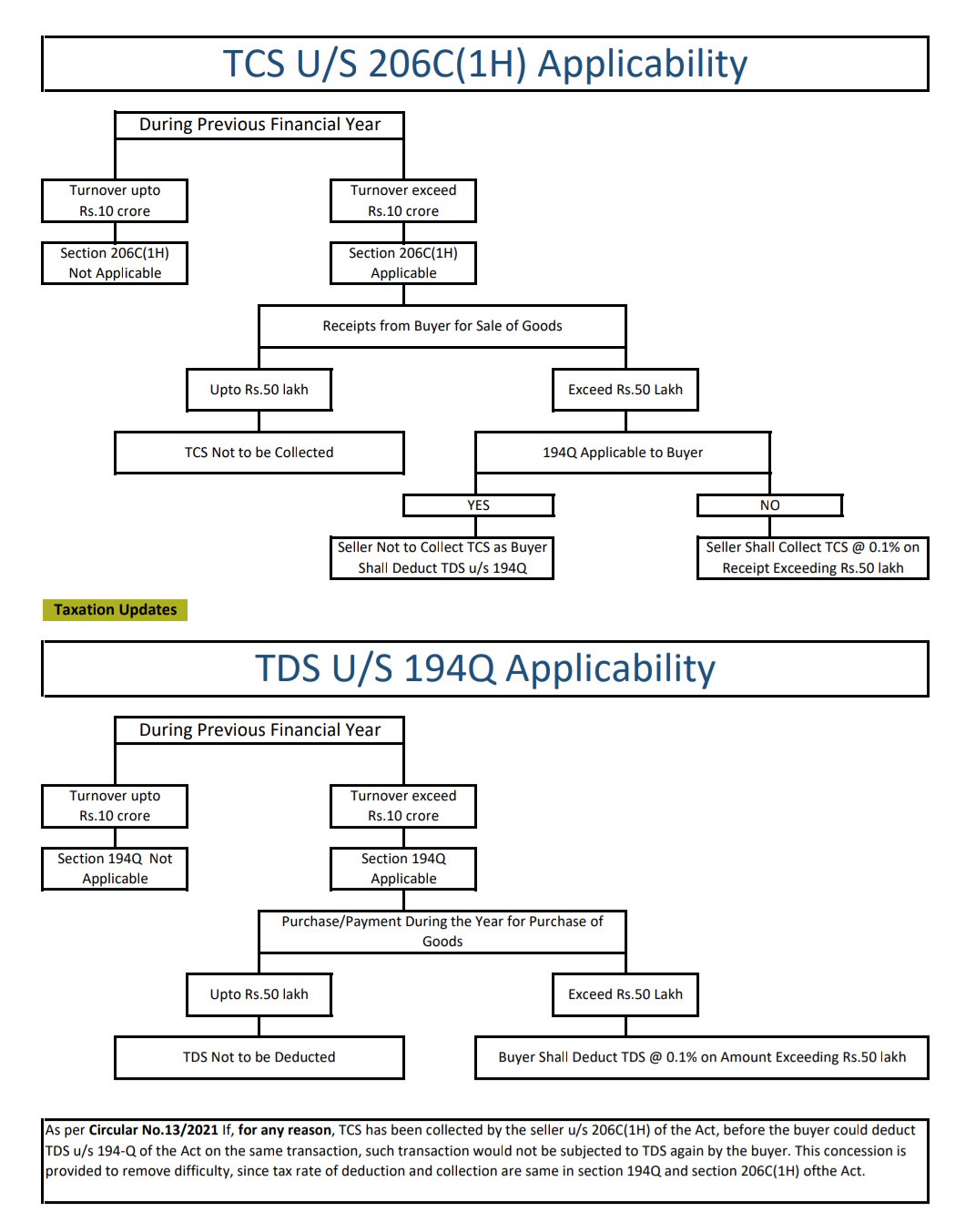

As per section 194Q, every buyer who is responsible for making payment of any amount to a resident seller, for the purpose of purchasing any goods having value or an aggregate value greater than Rs 50 lakhs in any previous year; shall have to at the time of making that payment whichever is earlier, deduct an amount that is equal to 0.1% of such amount that exceeds Rs 50 lakhs as the Income Tax.

As per the circular issued by the Central Board of Direct Taxes

{kind=link}

{kind=link}

The circular further pinpointed that when the tax has to be deducted at the time of ‘credit’, TDS under 194W shall have to be deducted on the amount credited exclusively of GST component; however, if tax has been deducted on the criteria of payment basis then TDS shall have to be deducted on the whole amount. The reason being, it will not be possible to recognize the GST component.

Furthermore, it has been pinpointed that while the new provisions should be applicable on advance payment, the same will not be applicable to non-resident whose purchase is not related to the Permanent Establishment of the said non-resident of India.