Goods and Service Tax (GST) registered taxpayers who desire to apply for the GST Amnesty Scheme 2024 u/s 128A announced in Budget 2024, must learn that a procedural change in application filing is there. The taxpayer without submitting a withdrawal request of plea could not apply for the GST Amnesty Scheme u/s 128A.

Towards the particular taxpayers set by GSTN the change is applicable and to be qualified for the amnesty scheme application they are needed to apply for the related appellate authority to withdraw their current appeal and they could apply for the Amnesty Scheme u/s 128A. On the GST portal for such specified taxpayers the appeal withdrawal is not available.

Read below to discover which taxpayers would be required to apply to the appellate authority to withdraw their plea (if any) and thereafter apply for the GST Amnesty Scheme waiver of interest and penalty u/s 128A.

Who is required to apply before the appellate to withdraw the plea and thereafter apply for the Amnesty scheme? If the taxpayer has submitted a plea against the respective GST notice via GST APL 01 form before March 21, 2023, the taxpayer thereafter is required to submit their request for withdrawing a plea to the related appellate authority first.

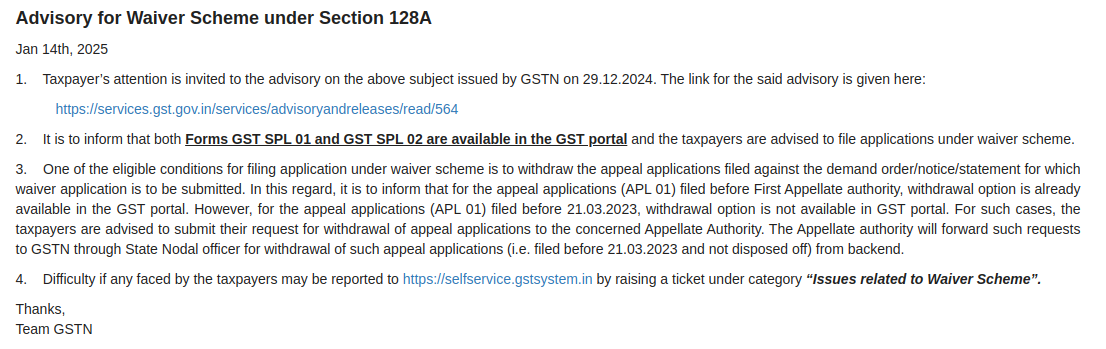

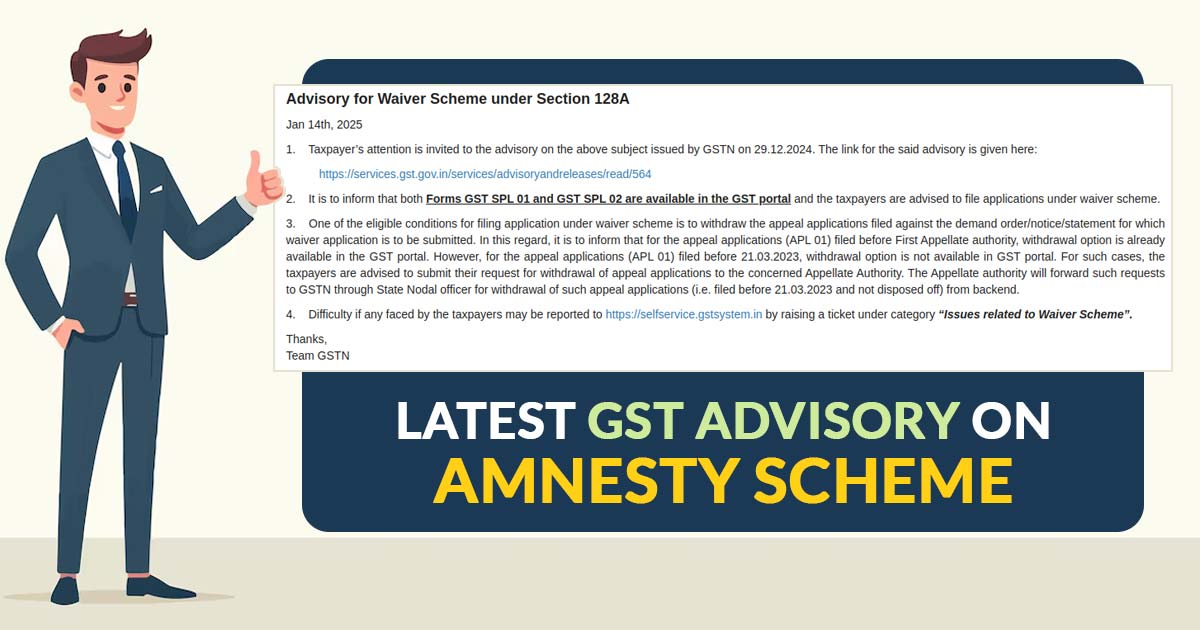

GSTN in an advisory dated January 14, 2025, expressed: “One of the eligible conditions for filing an application under the waiver scheme is to withdraw the appeal applications filed against the demand order/notice/statement for which waiver application is to be submitted.”

“In this regard, it is to inform you that for the appeal applications (APL 01) filed before the First Appellate Authority, the withdrawal option is already available in the GST portal. However, for the appeal applications (APL 01) filed before 21.03.2023, the withdrawal option is not available in the GST portal. For such cases, the taxpayers are advised to submit their request for withdrawal of appeal applications to the concerned Appellate Authority.”

Read Also: New GST Forms SPL-01 and SPL-02 to Avail Interest Waiver and Penalties U/S 128A

“The Appellate authority will forward such requests to GSTN through the State Nodal officer for withdrawal of such appeal applications (i.e. filed before 21.03.2023 and not disposed off) from the backend.”