Income Tax Appellate Tribunal (ITAT), Mumbai, in a decision, has ruled that a new flat value received in a redevelopment project could not be levied to tax as Income from Other Sources’ u/s 56(2)(x) of the Income Tax Act.

Increasing project redevelopment has been seen in Mumbai. Over 31,000 redevelopment projects had been approved as of last May. As per chartered accountants, the ITAT order provides clarity to flat owners who have opted for redevelopment or intend to do so. It assures that no unfair taxes are there on them.

In this case, A Pitale purchased a flat in a housing society in 1997-98. On the redevelopment of the society, he received a new flat in December 2017.

Read Also: ITAT Hyderabad: Flat Ownership for at Least Three Years is Needed to Claim LTCG

In the assessment for the FY 2017-18, the IT officer treated the difference between the stamp value of the new flat (Rs 25.17 lakh) and the indexed cost of the old flat (Rs 5.43 lakh), which works out to Rs 19.74 lakh, as imposed to tax in Pitale’s hands under the head ‘Income from other sources’.

ITAT ruled in the taxpayers’ favour, stressing that receiving a new flat in place of an old one is a case of ‘extinguishment’ of property rights rather than an income-generating transaction. It noted: “This is not a case of receipt of immovable property for inadequate consideration. It is a legitimate transaction involving the replacement of an existing asset with a new one.”

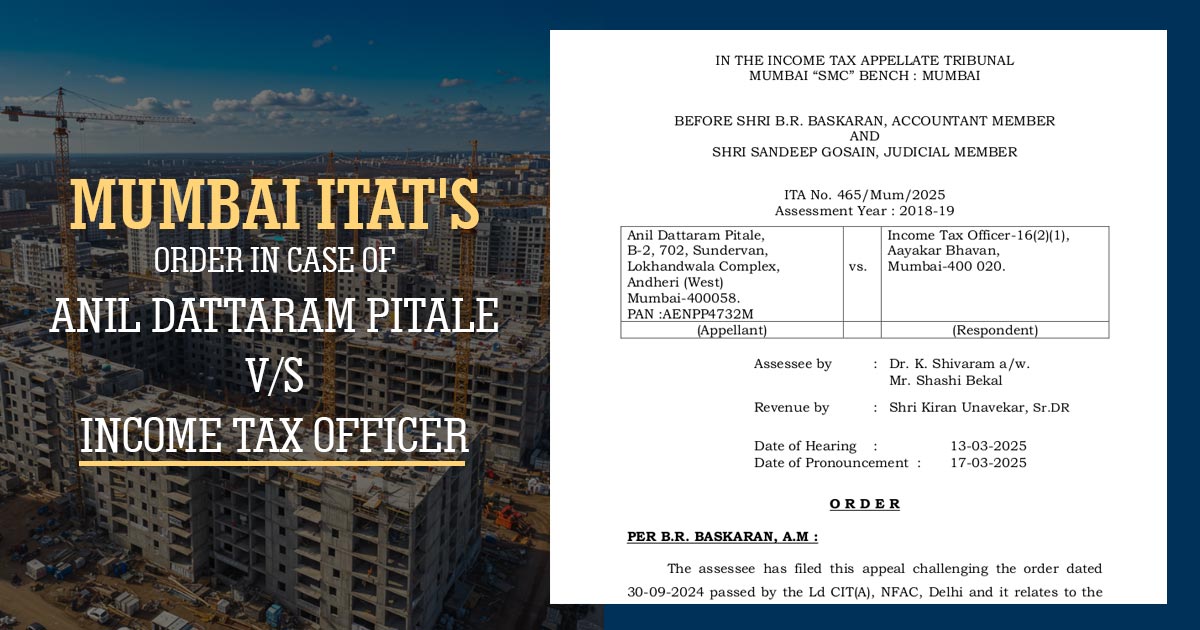

| Case Title | Anil Dattaram Pitale Vs. Income Tax Officer |

| Citation | ITA No. 465/Mum/2025 |

| Date | 17-03-2025 |

| Counsel For Appellant | Dr. K. Shivaram A/W. Mr. Shashi Bekal |

| Counsel For Respondent | Shri Kiran Unavekar, Sr.DR |

| Mumbai ITAT | Read Order |

I am regular user IT Genius for filing of IT returns since e filing process has started