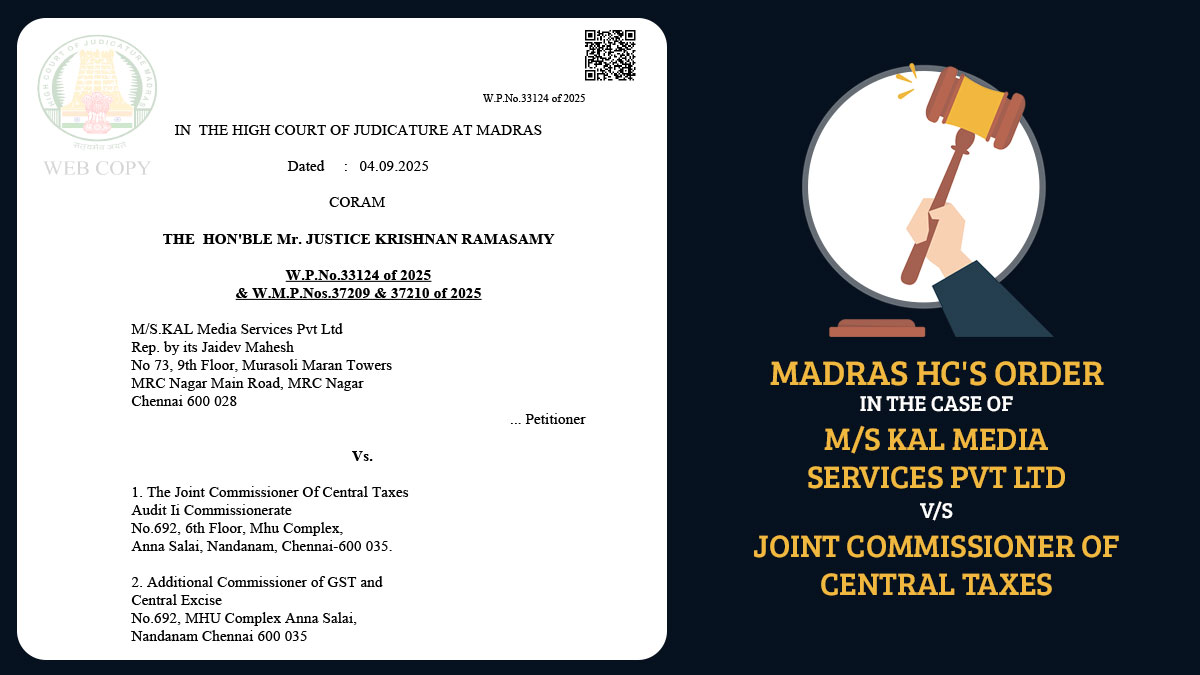

The Madras High Court has ruled that the tax department cannot issue combined GST notices covering multiple financial years at once. Instead, the court stated that each financial year must be dealt with individually.

M/s. KAL Media Services Pvt Ltd, the applicant, contested the impugned show cause notice on 19 June 2025 and the consequential notice on 30 June 2025, claiming that these were a combination of multiple years into one proceeding, which was not allowable under the GST Act.

The counsel of the applicant and the counsel of the respondent said that the problem was similar to one already determined by the High Court in its common order on 21 July 2025 in W.P. Nos. 29716 of 2024 etc. batch.

The court, in its previous ruling, specified the norms governing the issuance of GST show cause notices. The GST Act allows issuance of these notices on the grounds of a specified tax period, it cited.

In the former decision, it was held that when an annual return has been submitted, then the whole fiscal year is considered as the tax period, and as per that, the SCN needs to be framed with reference to that return.

In the cases of notice issuance before annual return filing, they might be issued for the monthly returns. But any notice should be as per the annual return of the pertinent fiscal year after the annual returns are submitted or the limitation period has begun.

No SCN can cover more than 1 fiscal year, as such bunched notices are not permitted in law, Justice Krishnan Ramasamy ruled. Therefore, any notices issued via clubbing multiple financial years together are without jurisdiction and consequently liable to be quashed.

The court determined that the contested notifications, covering 2018 to 2024, shared the same legal flaw.

The action of the department was non-sustainable and did not have jurisdiction, as the GST Act does not permit grouping of several fiscal years into a single notice, the court discovered.

Consequently, the court has quashed the impugned notice and its resulting notice on 30 June 2025, within the scope they desired to club multiple years together.

Recommended: Madras HC Quashes GST Orders Issued Under Notif. No. 56/2023, Says Extension Valid Only in Exceptional Circumstances

The court has given a chance to the GST department to start the fresh proceedings for each fiscal year separately in 4 weeks from the receipt of the order, or before the lapse of the limitation period for each respective year, whichever is later.

| Case Title | M/S KAL Media Services Pvt Ltd vs. Joint Commissioner Of Central Taxes |

| Case No. | W.P.No.33124 of 2025 |

| For the Petitioner | Mr.G Natarajan |

| For Respondent | Mr.Rajendran Raghavan |

| Madras High Court | Read Order |