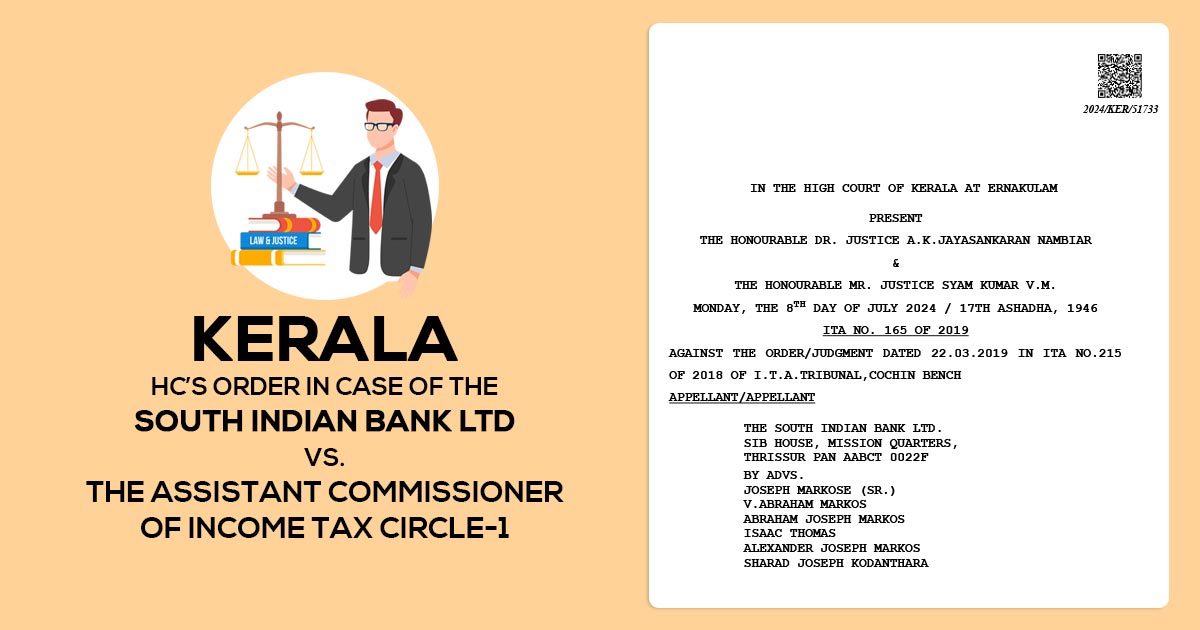

It was ruled by the Kerala High Court that the South Indian Bank is entitled to the deduction envisaged u/s 36(1)(viii) of the Income Tax Act concerning the long-term finance furnished by it for the construction and purchase of houses in India for residential purposes.

The appellant-bank/assessee South Indian Bank Ltd is in the business of furnishing housing loans for the purchase of the construction of houses and had been receiving the advantage of the deduction mentioned u/s 36(1)(viii) in the years before the amendment. The disallowance was derived as a consequence of an amendment that affected the provisions of Sections 36(1)(viii) w.e.f April 1, 2010, through the Finance (No. 2) Act, 2009.

It was discovered by the assessing authority that qualified business in context to the banking company comprises merely the business of furnishing the long-term finance for the development of housing in India and therefore no advantage has been obtained to the appellant if it furnished the long-term finance for the construction or purchase of the houses in India for residential purposes.

It was seen by the appellate tribunal that post-amendment and the deletion of the words ‘construction or purchase of houses in India for residential purposes’ from the definition of the qualified business in context to the banking company, the deduction envisaged for the banking company cannot get claimed in a case where the bank was involved in furnishing the long-term finance for the construction or purchase of the houses for the residential pursuits.

Read Also: Kerala High Court Ruling: An Assessee Can Claim Deduction U/S 80P By Filing ITR on Time

It was argued by the taxpayer that the National Housing Bank was not qualified for the advantages of the unamended Section 36(1)(viii) based on the state that it was not involved directly in the long-term financing for the construction or purchase of houses in India for residential purposes.

Hence the amendment was considered essential to extend the said advantage for the National Housing Bank. The amendment was intended to broaden the scope of the deduction concerning the financial corporations mentioned in section 4A of the Companies Act.

The financial corporations were public sector companies, banking companies, and cooperative banks excluding primary agricultural credit societies or primary cooperative agricultural and rural development banks, and to determine the advantage available to a housing finance company only concerning the provision of long-term finance for the construction or purchase of houses in India for residential purposes.

It was remarked by The division bench of Justice A.K. Jayasankaran Nambiar and Justice Syam Kumar V.M. that the National Housing Bank was not permitted to benefit from the unamended Section 36(1) (viii) of the Income-tax legislation, on the foundation that the same was not involved directly in the long term financing for construction or purchase of houses in India for residential purpose. Consequently, the amendment was deemed crucial to extend the stated benefit even to the National Housing Bank.

The court while permitting the appeal set aside the findings of the tribunal since the given long-term finance for construction or purchases of houses in India for the residential objectives was an activity that was entitled to the deduction u/s 36(1)(viii) solely for housing finance companies; the activity shall not entitle for deduction concerning a banking company.

| Case Title | The South Indian Bank LTD Vs. The Assistant Commissioner of Income Tax Circle-1 |

| Citation | ITA Nos.165 of 2019, 26 and 28 of 2020 |

| Date | 08.07.2024 |

| For the Appellant | Joseph Markose (Sr.), V.abraham Markos, Abraham Joseph Markos, Isaac Thomas, Alexander Joseph Markos, Sharad Joseph Kodanthara |

| For the respondents | Sri.p.k.ravindranatha Menon (Sr.), Sri.jose Joseph |

| Sri.p.k.ravindranatha Menon (Sr.), Sri.Jose Joseph | Read Order |