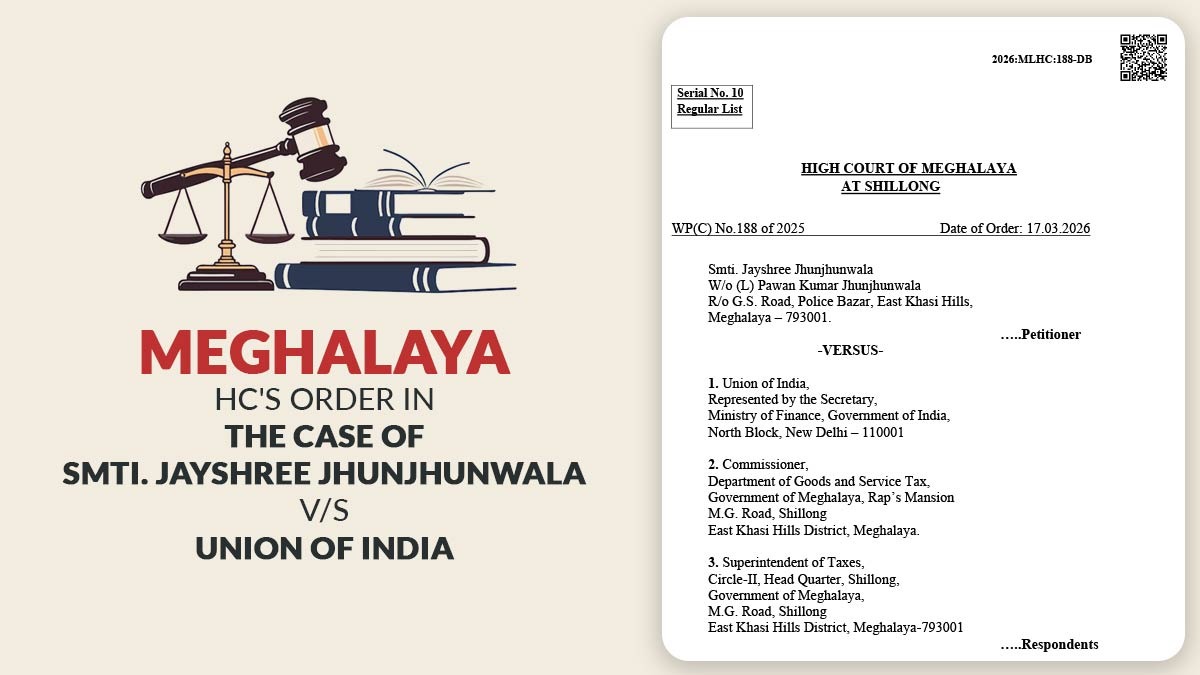

When the foundation was missing then there do not have any erection of the basis to ask for the reopening of the assessment, the Gujarat High Court ruled.

Neither foundational points do exist nor can any tangible material be available with the assessing officer to prove the practice of power for reopening the assessment, the bench of Justice N.V. Anjaria and Justice Devan M. Desai observed.

On 30th March 2018, the applicant challenged the notice provided by the assessing officer against the applicant asking to reopen the assessment under section 148 of the income tax act, 1961. The income levied to tax would have fled the assessment within the terms of section 147 of the income tax act 1961, mentioned in the notice for the AY 2011-12.

The assessee submitted his objections to the reasons given, noting, among other things, in his letter dated September 1, 2018, that the petitioner assessee sold the immovable property with four other people for a total selling value of Rs. 9 crores.

After regarding the capital gains, the income tax return was filed for the AY 2011-12. The calculation of the income was duly shown and 1/5th share of the sale value of the immovable property the bungalow was shown. The immovable property bungalow was sold by 5 joint owners with equal shares.

According to the petitioner, the assessing officer reopened the matter more than four years after the finish of the related assessment year. The applicant had sold the immovable property with the other five co-owners for a total price of Rs. 9 crores and filed an income return for just the net income; it was submitted for Rs. 41,500.

Read Also: Delhi ITAT Set Aside Disallowances Based on Ad Hoc Due to AO Mistake

The council was aggrieved that the applicant does not have shown the capital gains and that there was an income escapement. The other co-owner assessed the total capital gain at Rs 1,27,94,856.

The taxpayer has specified all the points and information in the income return, and there is no question of reopening the assessment the court ruled.

| Case Title | Bimlakumari Lajpatraj Hurra Vs ITO |

| Case No. | R/Special Civil Application No. 16884 Of 2018 |

| Date | 17.04.2023 |

| Counsel for Petitioner | Darshan R Patel |

| Counsel for Respondent | Karan Sanghani |

| Gujarat High Court | Read Order |