Foreign Investment in any economy, whether FDI or FII, boosts growth and development in that economy. This has been witnessed by India also since 1991. Having said that, various tax mechanism also comes into play with the globalization. One such mechanism is Non-Resident Taxable Person (NRTP) in registration. In simple words, it is the registration of NRI’s for GST.

- NRTP encompasses in its purview any person

- Who does not have any fixed place of business or residence in India and

- Who occasionally undertakes those transactions that involve the supply of goods or services or both

It is worth mentioning here that the GST law of India

And more importantly, such a registration certificate is valid for 90 days only until and unless a shorter duration is specifically mentioned while applying for such registration. However, This certificate may further be granted an extension by the respective GST officer by another 90 days.

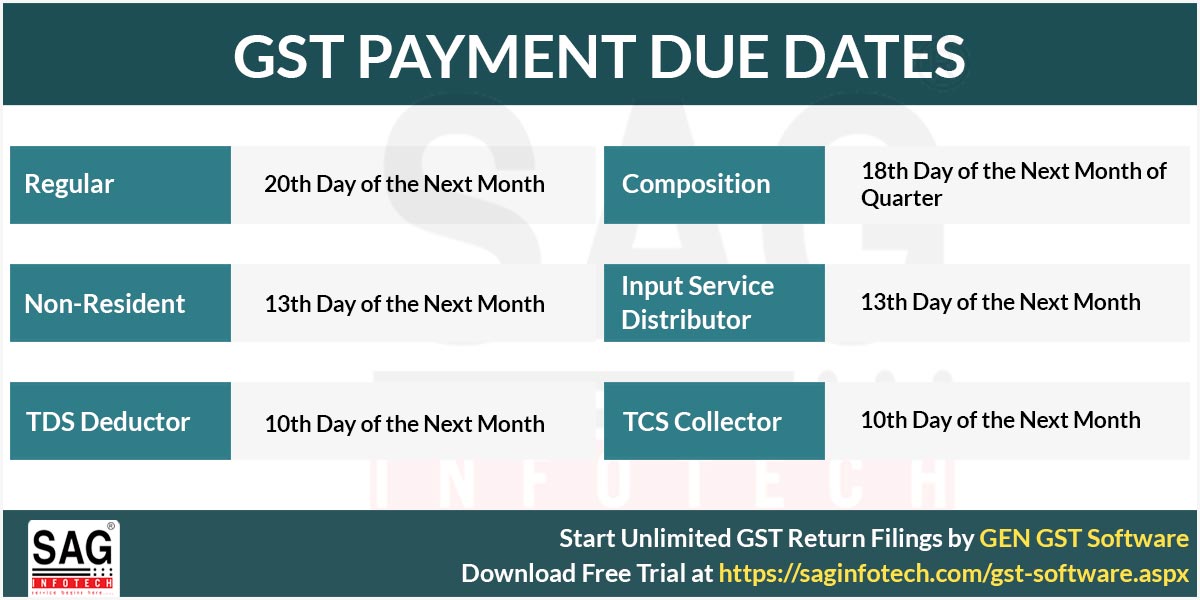

Further, it is necessary for NRTP to extend advance deposit of tax when applying for registration.

Interestingly, the Electronic cash ledger of every NRTP is provided on the GST portal, which consists of deposits and GST payments that a taxpayer

Non-Resident Taxable Person (NRTP) Registration Process

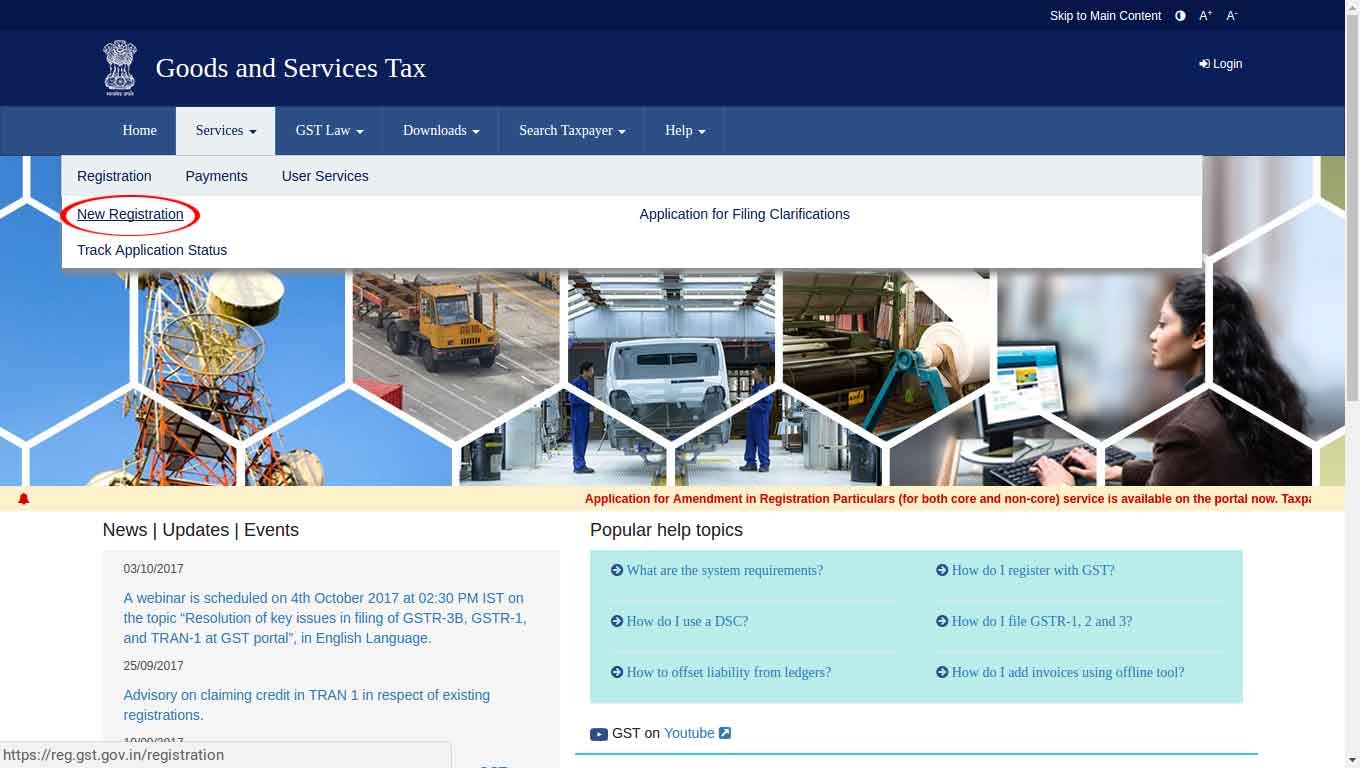

New Registration by NRTP can be done on the web portal of GST on the below-mentioned link www.gst.gov.in.

However, Before beginning the registration process, a 15-digit Temporary Reference Number (TRN) is required to be obtained from the GST portal on providing the necessary information. Following details are asked on GST portal for registration

The application form for registration (GST REG-09) is divided into 5 parts—business details, authorized signatory, principal place of business, bank account and verification.

Business Details: The details that are related to the business are required to be provided that includes, legal name, address TIN/PAN/Unique identification number, state, and so on. Lastly, the application also requires furnishing the details of the estimated turnover and associated tax liability for the registration period. On this basis, a challan is automatically generated for depositing the tax.

Authorized signatory: Here in this step, the personal details and the identity details of the authorised signatory are required for the registration. The personal information of the signatory includes details such as father’s name, address, date of birth, mobile number, gender, e-mail address, and so on The identity information includes details such as nationality, designation, Aadhaar number (if any).

Then Supporting documents including a photograph, Letter of Authorization ( proof of being the authorized signatory), copy of the resolution that is cleared by Board of Directors or Managing Committee and Acceptance Letter.

Principal place of Business: The Principal Place of Business includes the details of the primary location in the state from where NRTP’s business shall be conducted. Under this heading following information is required: address, contact information along with nature of possession of premises i.e. leased, owned etc. Further, One of the following documents are required: Property tax receipt, Municipal khata copy, Electricity bill copy, or Legal ownership document.

Bank Account: Providing of bank details is not mandatory. However, the same detail may be provided later on by filing an amendment application.

Verification: There are 3 options for verification, signature and submission: either by DSC (Digital Signature Certificate)

Finally, The GST officer examines the application and if it is apt, the registration is granted within 7 working days of submission of the application.In case of deficiency or discrepancy, the same is informed to the NRTP for rectification.

The registration certificate is a 15-digit unique tax identification number that is necessarily to be quoted on various official documents by the NRTP as and when need arises.