Basically, the GST registration is given with extensive validity. Although the validity date is liable in case of enrollment of random assessee as well as non-resident assessee. The random assessee or a non-resident assessee whose intention is to extend his GST registration

The procurement relevant to the need of extension of GST enrollment through application filing for Form GST REG-11 covered in Rule 15 for the Central Goods and Services Tax Rules, 2017. The similar part is thoroughly elaborated in the present article.

Classification of individuals needed to file an extended application and additional procurements. Below is the division for the assessee which is needed to file the extension application for Form GST REG-11

- Random assessee and

- Non-resident assessee

Under section 27 of the Central CGST Act, 2017

- Period as defined in the GST enrollment form

- 90 days from the valid time period of the GST enrollment.

If the GST applicants have the intention to prolonge the enrollment then the application for the extension needs to be furnished before the completion of the above validity.

File Elongated Application for GST REG-11 & before Condition

There is the availability of the extension of GST enrolment if a random assessee individual of a non-assessee is present during the filing of an application. It is severe to keep an eye on the enrollment might get extended for the highest period of 90 days. Moreover, the validity of the registration for the random assessee person or a non-assessee can be extended for once.

Condition for Before Filing the Application the Appellant

- Before the expiration period of registration, the Form GST REG-11 needs to be filed for the extended application.

- The petitioner must have to furnish the necessary GST returns

- The petitioner must have to pay the tax liabilities narrating to the extension time period, pre-filing for the extended application.

- The GSTN of the petitioner should be correct and activated. The class of registration has to be either random assessee or the non-resident assessee.

Points for Filing GST REG-11 on Official Portal

The random taxable individual or non-resident assessee prepared to increase the GST enrolment is obliged to accompany the following measures to file the application in Form GST REG-11.

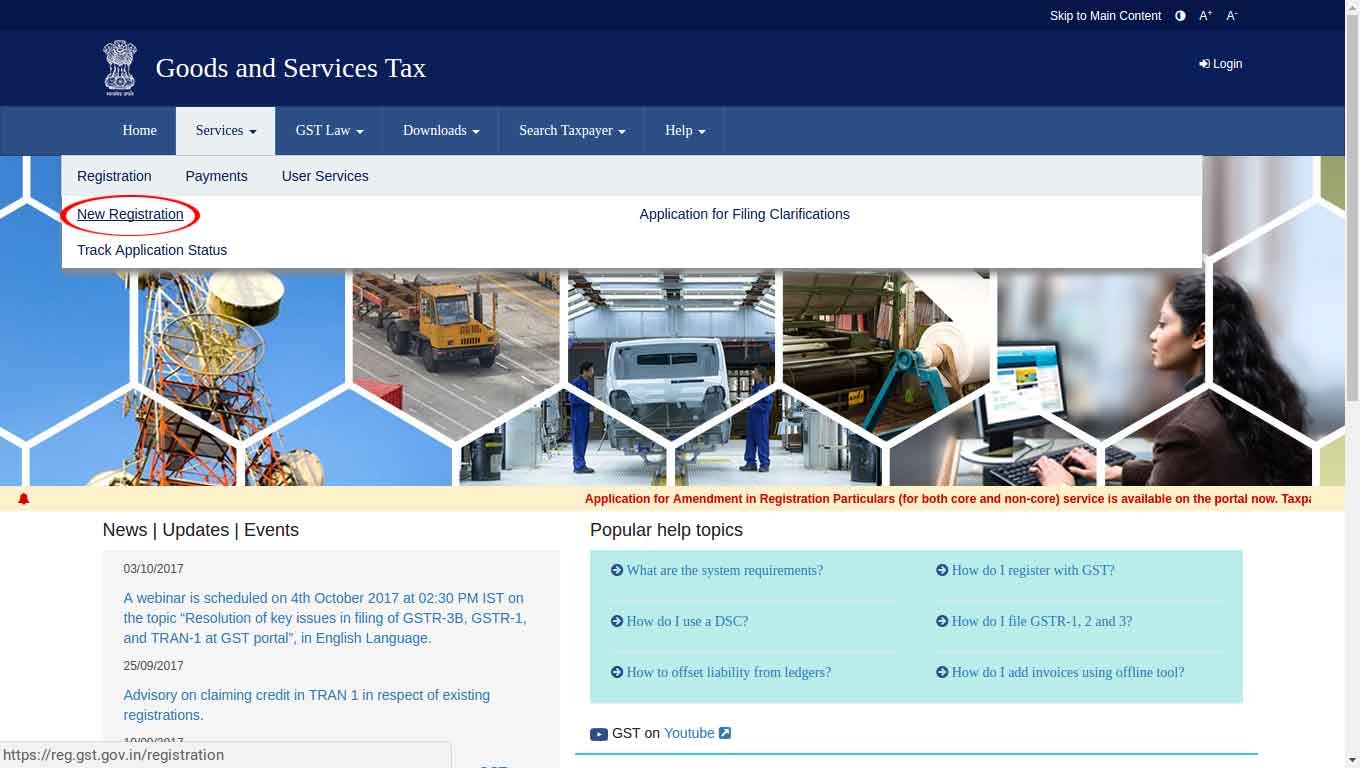

- STEP 1 – Attend the site https://www.gst.gov.in/

- STEP 2 – Tap the ‘Login’ icon

- STEP 3 – Insert the relevant ‘Username’, ‘Password’, and ‘Characters’

- STEP 4 – Click on ‘Log in’

- STEP 5 – Operate the path Services > Registration

- STEP 6 – Select ‘Application for Expansion of enrollment time by random or the non-resident taxable individual

Post following the above steps the application Form GST REG-11 will be displayed. Normal information such as Trade Name, GST Network

- Desired time for which extension is needed,

- The information for the turnover during an elongated time

- Approximation of the tax liability for the elongated period, and

- Information for the payment of approximated tax

Post furnishing of the information the petitioner has to submit the application form by utilizing digital signature certificate (DSC)