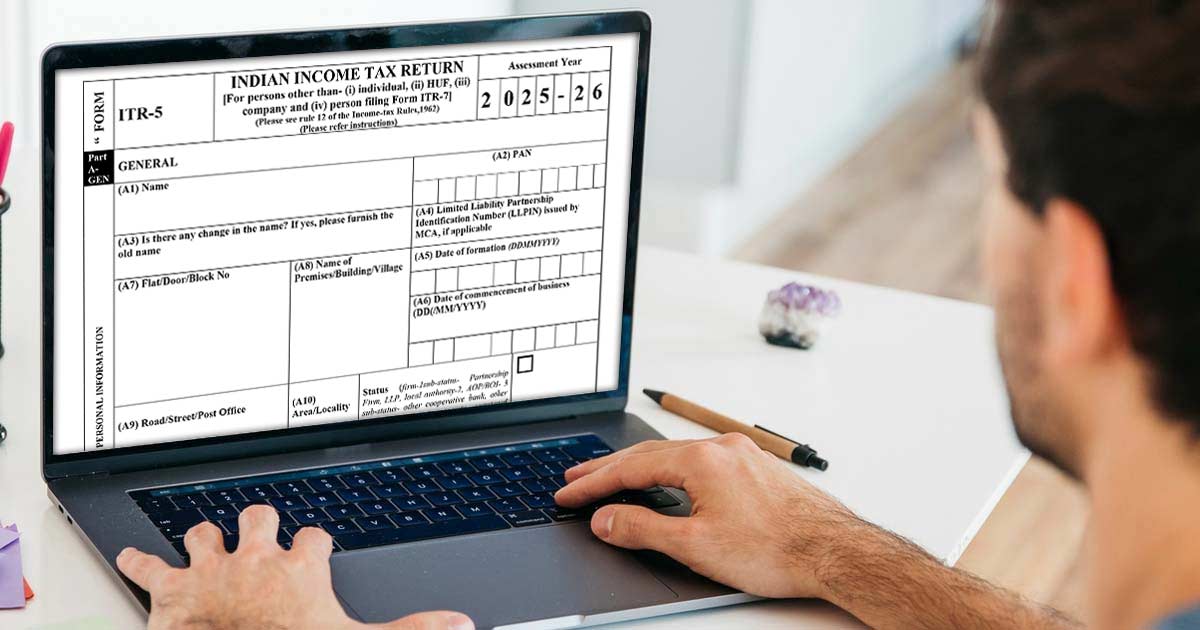

Income Tax Return Filing

Filing an income tax return is a responsibility of every citizen of the country and also mandatory for each one of them. Income Tax Return is the form in which an assessee furnishes all his Income and tax details and thereon submit it to the Income Tax Department. Various ITR forms are ITR 1 Sahaj form, ITR 2, ITR 3, ITR 4, ITR 5, ITR 6 and ITR 7. For filing the tax returns, every assessee should know and choose an appropriate ITR form, depending on his income and profession. ITR 5 Form is one of the income tax return forms that are to be used by specific parties. [For persons other than- (i) individual, (ii) HUF, (iii) company and (iv) person filing Form ITR-7]

Latest Update

- The ITR-5 offline utility, Mac (V1.1.7), the Excel-based utility (V1.6), and the JSON schema (V1.1) have been released on the official portal. Download now

Gen IT Software Demo for Filing ITR-5

Who can File the ITR 5 Form?

ITR 5 Form can be used by Firms, Limited Liability Partnerships (LLPs), Association of Persons(AOP) and Body of Individuals (BOIS), Artificial Juridical Person, Cooperative society and Loc, subject to the condition that they do not need to file the return of income under section 139(4A) or 139(4B) or 139(4C) or 139(4D) (i.e., Trusts, Political party, Institutions, Colleges, etc.). Individuals, HUFs (Hindu Undivided Families), Companies are not eligible to use the ITR 5 Form.

E-Filing Audit Reports

After the AY 2013-14, it has become mandatory for an assessee to furnish a report of audit under sections 10(23C)(iv), 10(23C)(v), 10(23C)(vi), 10(23C)(via), 10A, 10AA, 12A(1)(b), 44AB, 44DA, 50B, 80-IA, 80-IB, 80-IC, 80-ID, 80JJAA, 80LA, 92E, 115JB or 115VW, electronically on or before the date of filing the return of income.

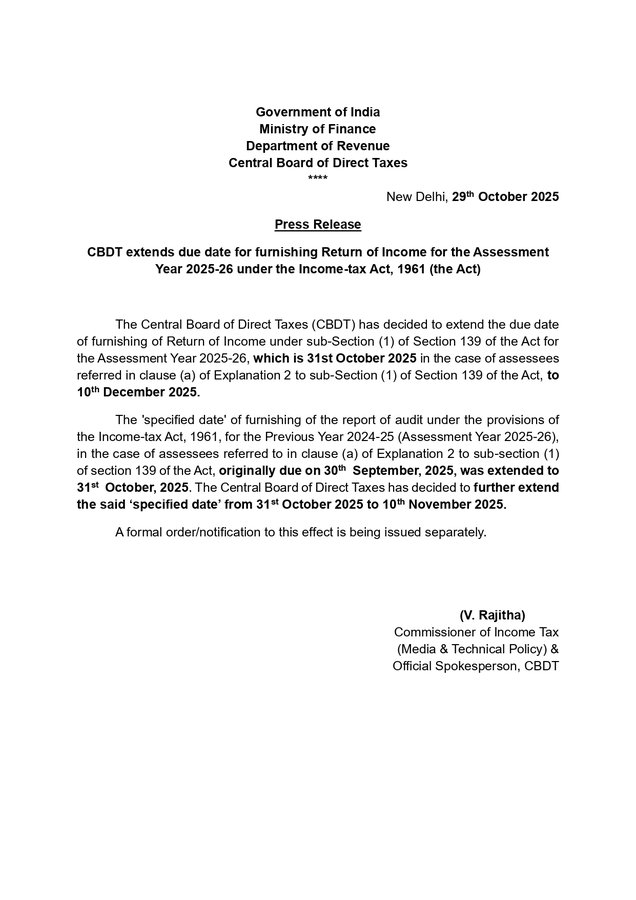

Due Date of ITR 5 Form Filing for AY 2025-26

| Annual Year | For Non-audit Cases | For Audit Cases |

|---|---|---|

| AY 2025-26 | 31st July 2025 (Revised till 16th September 2025, Read Press Release) | 10th December 2025 (Revised) Read PR |

| AY 2024-25 | 31st July 2024 | 31st October 2024 (Revised till 15th November 2024, Read Circular) |

| AY 2023-24 | 31st July 2023 | 31st October 2023 |

Instructions for Filing ITR 5 Form

When a schedule is not applicable, mention it as “—NA—”.

When an item is inappropriate, write “NA” against that item.

“Nil” stands for nil figures. Write Nil to denote figures of zero value.

For a negative figure or loss, write “-” before such a figure, other than provided in the form. All figures should be represented in the round-off manner to the nearest one rupee. In the same way, the figures for total income/ loss and tax payable should be rounded off to the nearest multiple of ten rupees.

How do I File My ITR 5 Form?

The ITR-5 Form can be filed with the Income Tax Department in two fashions i.e. online and offline. The form can be filed in an offline way, either by furnishing the return in a paper form or by furnishing a bar-coded return. When the return is filed on paper, the acknowledgement slip paired with the return form should be properly filled.

However, in the Online way, it can be filed by furnishing the return electronically under a digital signature or by transmitting the data in the return electronically, followed by the submission of the return verification in Return Form ITR V.

In the online filing, the assessee needs to print out two copies of the ITR-V Form. One copy of ITR-V, duly signed by the assessee, has to be sent within 30 days of filling return to Post Bag No. 1, Electronic City Office, Bengaluru–560100 (Karnataka) via ordinary post. The other copy should be kept by the assessee with himself as a record.

Read Also: Penalty Provisions If Not File Income Tax Returns for the Current FY

Note: It is mandatory for a firm to furnish the return electronically under a digital signature, whose accounts are liable to audit under section 44AB.

How to Fill Out the Verification Document?

Furnish all the required information in the verification document. Make sure that the verification has been duly attested before filing the return. Mention the designation of the person signing/attesting the return.

Note: Any individual making a false/wrong statement in the return or in the related schedules shall be liable to be hauled in the court under section 277 of the Income-tax Act, 1961 and shall be punishable under the section with imprisonment and fine after the court’s decision against him.

Step-by-Step Guide to File ITR 5 Form for AY 2025-26?

Part A – GEN General

Personal Information

- Name

- PAN

- Is there any change in the name? If yes, please furnish the old name

- Limited Liability Partnership Identification Number (LLPIN) issued by MCA, if applicable

- Flat/Door/Block No

- Name of Premises/Building/Village

- Date of formation (DD/MM/YYYY)

- Date of commencement of business (DD/MM/YYYY)

- Road/Street/Post Office

- Area/Locality

- Status (firm-1sub-status- Partnership Firm, LLP, local authority-2, AOP/BOI- 3 sub-status- other cooperative banks, other cooperative society, a society registered under society registration Act, 1860 or any other Law corresponding to that state, Primary agricultural credit society/cooperative bank, Rural development bank, Business trust, investment fund, Trust other than trust eligible to file Return in ITR 7, any other AOP/BOI,, artificial juridical person-4, sub-status- Estate of the deceased, Estate of the insolvent, Other AJP)

- Town/City/District

- State

- Country

- Pin code/Zip code

- Office Phone Number with STD code/ Mobile No. 1

- Mobile No. 2

- Email Address -1

- Email Address -2

- Due Date for Filing Return of Income

- 31st July

- 31st October

- 30th November

Filing Status

- (a) Filed u/s (Tick)

- 139(1)-On or before due date

- 139(4)-After due date

- 139(5)-Revised Return

- 92CD-Modified return

- 119(2)(b)- After Condonation of delay

- Or Filed in response to notice u/s

- 139(9)

- 142(1)

- 148

- 153C

- Whether you are a business trust? (Yes or No)

- Whether you are an investment fund referred to in section 115UB? (Yes or No)

- (b) If revised/in response to notice for Modified, then enter Receipt No. and Date of filing the original return (DD/MM/YYYY)

- (c) If filed in response to a notice u/s 139(9)/142(1)/148/153A/153C/ or order u/s 119(2)(b) enter Unique Number/ Document Identification Number (DIN) and date of such notice/order, or if filed u/s 92CD enter date of advance pricing agreement

- (d) Method of opting-out of new tax regime (if applicable) for current AY:

- By filing 10IEA (having income from business or profession) (answer set A)

- By exercising the option in the return of income only (form 10IEA is not applicable) (answer set B)

- 2A. (Set A)

- Have you exercised the option u/s 115BAC(6) of Opting out of new tax regime in Form 10-IEA in AY 2024-25?

- (a) Yes (If ‘Yes’, please furnish date of filing and Acknowledgement number of Form 10-IEA for AY 2024-25)

- 2a. Do you wish to continue to opt out of New Tax Regime for current assessment year: Yes/No

- (If ‘No’, please furnish date of filing and Acknowledgement number of Form 10-IEA for AY 2025-26)

- (b) No (Please select ‘No’, even if Form 10IEA was filed after due date for AY 2024-25)

- 2b. Do you wish to opt out of New Tax Regime for current assessment year: Yes/No

- (If ‘Yes’, please furnish date of filing and Acknowledgement number of Form 10-IEA for AY 2025-26)

- (c) Not Applicable for AY 2024-25 as there was no business income.

- 2c. Do you wish to opt out of New Tax Regime for current assessment year: Yes/No

- (If ‘Yes’, please furnish date of filing and Acknowledgement number of Form 10-IEA for AY 2025-26)

- Note- Option under section 115BAC(6) should be exercised in Form 10IEA on or before the due date for filing return u/s 139(1).

- 2B. (Set B)

- Do you wish to exercise the option u/s 115BAC(6) of Opting out of new tax regime? (default is “No”) Yes or No

- (d.ii) Have you opted for tax regime u/s 115BAD? Yes or No? (If yes, please furnish the AY in which said option is exercised for the first time along with date of filing of Form 10-IF & acknowledgment number)

- (d. iii) If “No”, Option for current assessment year Not opting opting it now. If “opting it now”, please furnish

- (d. iv) If you are a new manufacturing cooperative society, whether you were required to furnish the return of income mandatorily u/s 139(1) for the AY 2024-25? Yes or No

- div(a) If the answer to (div) is “Yes”, whether you have exercised the option u/s 115BAE of Opting of new tax regime in A.Y 2024-25? Yes or No

- div(b) If the answer to (div) is “No”, do you wish to exercise the option u/s 115BAE of Opting of New Tax regime in AY 2025-26: Yes or No

- div(c) If div(a) or div(b) is selected as ‘Yes’, please furnish date of filing of Form 10-IFA & acknowledgment number

- (e) Residential Status

- Resident

- Non-Resident

- (f) Whether the assessee is located in an International Financial Services Centre and derives income solely in convertible foreign exchange? (Yes/No)

- (g) Whether you are recognized as a startup by DPIIT

- (h) If yes, please provide start-up recognition number allotted by the DPIIT

- (i) Whether a certificate from the inter-ministerial board for certification is received?

- (j) If yes, please provide the certification number

- (k) Whether you are recognized as MSME

- (l) If yes, please provide the registration number allotted as per MSMED Act 2006

- (m) In the case of non-resident, is there a permanent establishment (PE) in India

- (n) In the case of non-resident, is there a significant economic presence (SEP) in India as defined in Explanation (2A) to section 9(1) (Yes/No)

- (a) aggregate of payments arising from the transaction or transactions during the previous year as referred in Explanation 2A(a) to Section 9(1)(i)

- (b) number of users in India as referred in Explanation 2A(b) to Section 9(1)(i)

- (o) Whether you are an FII / FPI? Yes/No If yes, please provide SEBI Regn. No.

- (p) Whether this return is being filed by a representative assessee? (Yes or No) If yes, please furnish following information –

- Name of the representative

- Capacity of the Representative (drop down to be provided)

- Address of the representative

- Permanent Account Number (PAN)/Aadhaar No. of the representative

- (q) Whether you are a Partner in a firm?

- (r) Whether you have held unlisted equity shares at any time during the previous year? If yes, please furnish the following information in respect of equity shares

- (s) Legal Entity Identifier (LEI) details (mandatory if refund is 50 crore or more)

- LEI Number

- Valid up to date

Audit Information

- a1. Whether liable to maintain accounts as per section 44AA? (Yes/No)

- a2. Whether assessee is declaring income only under section 44AD/44ADA/44AE/44B/44BB/44BBA

- a2 i. If No, whether during the year Total sales/turnover/gross receipts of business exceeds Rs.1 crore but does not exceed Rs.10 crores?

- a2 ii. If Yes is selected at a2i, whether aggregate of all amounts received including amount received for sales, turnover or gross receipts or on capital account such as capital contribution, loans etc. during the previous year, in cash, & non-a/c payee cheque/DD does not exceed five per cent of the said amount?

- a2 iii If Yes is selected at a2i, whether aggregate of all payments made including amount incurred for expenditure or on capital account such as asset acquisition, repayment of loans etc. & non-a/c payee cheque/DD during the previous year, in cash, does not exceed five per cent of the said payment?

- b. Whether liable for audit under section 44AB? (If Yes is selected at (b), mention by virtue of which of the following conditions:)

- (bi) Sales, turnover or gross receipts exceeds the limits specified under section 44AB

- (b ii) Assessee falling u/s 44AD/44ADA/44AE/44BB but not offering income on presumptive basis (Tick applicable section) 44AD, 44ADA, 44AE, 44BB

- (b iii) Others (Tick)

- c. If (b) is Yes, whether the accounts have been audited by an accountant? (Tick) Yes/No. If Yes, furnish the following information-

- (i) Date of furnishing of the audit report (DD/MM/YYYY)

- (ii) Name of the auditor signing the tax audit report

- (iii) Membership no. of the auditor

- (iv) Name of the auditor (proprietorship/ firm)

- (v) Proprietorship/firm registration number

- (vi) Permanent Account Number (PAN)/Aadhaar No. of the auditor (proprietorship/ firm)

- (vii) Date of audit report

- (viii) Acknowledgement number of the audit report

- (ix) UDIN

- di. Are you liable for Audit u/s 92E?

- dii. If (di) is Yes, whether the accounts have been audited u/s 92E?

- diii If liable to furnish other audit report under the Income-tax Act, mention whether have you furnished such report. If yes, please provide the details as under) (Please see Instructions )

- e If liable to audit under any Act other than the Income-tax Act, mention the Act, section and date of furnishing the audit report?

Partners/ Members/trust

- A. Whether there was any change during the previous year in the partners/members of the firm/AOP/BOI (In case of societies and cooperative banks give details of Managing Committee)

- B. Is any member of the AOP/BOI/executor of AJP a foreign company?

- C. If Yes, mention the percentage of share of the foreign company in the AOP/BOI/ executor of AJP

- D. Whether total income of any member of the AOP/BOI/executor of AJP (excluding his share from such association or body or executor of AJP) exceeds the maximum amount which is not chargeable to tax in the case of that member?

- E. Particulars of persons who were partners/ members in the firm/AOP/BOI or settlor/trustee/beneficiary in the trust or executors in the case of estate of deceased / estate of insolvent as on the 31st day of March, 2025 or date of dissolution

- F. To be filled in case of persons referred to in section 160(1)(iii) or (iv)

- G.Nature of business or profession, if more than one business or profession indicate the three main activities/ products (Other than those declaring income under sections 44AD, 44ADA and 44AE)

Part A-BS: Balance Sheet as on 31st Day of March, 2025 or Date of Dissolution

A. Sources of Funds

- 1 Partners’ / members’ fund

- 2 Loan funds

- 3 Deferred tax liability

- 4 Advances

- 5 Sources of funds (1c + 2c +3 + 4iii )

B. Application of funds

1 Fixed assets

2 Investments

3 Current assets, loans and advances

4

a Miscellaneous expenditure not written off or adjusted

b Deferred tax asset

c Debit balance in Profit and loss account/ accumulated balance

d Total (4a + 4b + 4c)

5 Total, application of funds (1e + 2c + 3e +4d)

No Account Case

C. In a case where regular books of account of business or profession are not maintained, furnish the following information as on 31st day of March, 2025, in respect of business or profession:

- Amount of total sundry debtors

- Amount of total sundry creditors

- Amount of total stock-in-trade

- Amount of the cash balance

Part A Manufacturing Account: Manufacturing Account for the Financial Year 2024-25 (fill items 1 to 3 in a case where regular books of accounts

are maintained, otherwise fill items 62 to 66 as applicable)

- 1 Debits to Manufacturing Account

- 2 Closing Stock

- 3 Cost of Goods Produced – Transferred to Trading Account (1f-2)

Part A-trading Account: Trading Account for the Financial Year 2024-25 (fill items 4 to 12 in a case where regular books of accounts are maintained, otherwise fill items 62 to 66 as applicable)

- 4 Revenue From Operations

- 5 Closing Stock of Finished Stocks

- 6 Total of Credits to Trading Account (4d + 5)

- 7 Opening Stock of Finished Goods

- 8 Purchases (Net of Refunds and Duty or Tax, if Any)

- 9 Direct Expenses (9i + 9ii + 9iii)

- 10 Duties and Taxes, Paid or Payable, in Respect of Goods and Services Purchased

- 11 Cost of Goods Produced – Transferred From Manufacturing Account

- 12 Gross Profit From Business/profession – Transferred to Profit and Loss Account (6-7-8-9-10xii11)

- 12.a Turnover from Intraday Trading

- 12.b Income from Intraday Trading – transferred to Profit and Loss account

Part A-P& L: Profit and Loss Account for the Financial Year 2024-25 (fill items 13 to 60 in a case where regular books of accounts are maintained, otherwise fill items 62 to 66 as applicable)

- 13 Gross Profit Transferred From Trading Account

- 14 Other Income

- 15 Total of Credits to Profit and Loss Account (13+14xii)

- 16 Freight Outward

- 17 Consumption of Stores and Spare Parts

- 18 Power and Fuel

- 19 Rents

- 20 Repairs to Building

- 21 Repairs to Machinery

- 22 Compensation to Employees

- 23 Insurance

- 24 Workmen and Staff Welfare Expenses

- 25 Entertainment

- 26 Hospitality

- 27 Conference

- 28 Sales Promotion Including Publicity (Other Than Advertisement)

- 29 Advertisement

- 30 Commission

- 31 Royalty

- 32 Professional / Consultancy Fees / Fee for Technical Services

- 33 Hotel, Boarding and Lodging

- 34 Travelling Expenses Other Than on Foreign Travelling

- 35 Foreign Travelling Expenses

- 36 Conveyance Expenses

- 37 Telephone Expenses

- 38 Guest House Expenses

- 39 Club Expenses

- 40 Festival Celebration Expenses

- 41 Scholarship

- 42 Gift

- 43 Donation

- 44 Rates and Taxes, Paid or Payable to Government or Any Local Body (Excluding Taxes on Income)

- 45 Audit Fee

- 46 Salary/remuneration Paid to Partners of the Firm

- 47 Other Expenses

- 48 Bad Debts

- 49 Provision for Bad and Doubtful Debts

- 50 Other Provisions

- 51 Profit Before Interest, Depreciation and Taxes [15 – (16 to 21 + 22xi + 23v + 24 to 29 + 30iii + 31iii + 32iii + 33 to 43 + 44x + 45 + 46 + 47iii + 48vii + 49 + 50)]

- 52 Interest

- 53 Depreciation and Amortisation

- 54 Net Profit Before Taxes (51 – 52iii – 53)

- 55 Provision for Current Tax

- 56 Provision for Deferred Tax and Deferred Liability

- 57 Profit After Tax (54 – 55 – 56)

- 58 Balance Brought Forward From Previous Year

- 59 Amount Available for Appropriation (57 + 58)

- 60 Transferred to Reserves and Surplus

- 61 Balance Carried to Balance Sheet in Proprietor’s Account (59 – 60)

- 62 Computation of Presumptive Business Income Under Section 44ad (Only for Resident Partnership Firm Other Than LLP)

- 63 Computation of Presumptive Income From Professions Under Section 44ada (Only for Resident Partnership Firm Other Than Llp)

- 64 Computation of Presumptive Income From Goods Carriages Under Section 44ae

- 65 If regular books of account of business or profession are not maintained, furnish the following information for previous year 2024 -25 in respect of business or profession

- 66 i Turnover From Speculative Activity

- ii Gross Profit

- iii Expenditure, if Any

- iv Net Income From Speculative Activity (66ii – 66iii)

Part A- OI: Other Information

- 1 Method of accounting employed in the previous year Tick? Mercantile or Cash

- 2 Is there any change in the method of accounting

- 3a Increase in the profit or decrease in loss because of deviation, if any, as per Income Computation Disclosure Standards notified under section 145(2) [column 11a(iii) of Schedule ICDS]

- 3b Decrease in the profit or increase in loss because of deviation, if any, as per Income Computation Disclosure Standards notified under section 145(2) [column 11b(iii) of Schedule ICDS]

- 4 Method of valuation of closing stock employed in the previous year

- Raw Material (if at cost or market rates, whichever is less write 1, if at cost, write 2, if at market rate, write 3)

- Finished goods (if at cost or market rates, whichever is less write 1, if at cost, write 2, if at market rate, write 3)

- Increase in the profit or decrease in loss because of deviation, if any, from the method of valuation specified under section 145A

- Decrease in the profit or increase in loss because of deviation, if any, from the method of valuation specified under section 145A

- 5 Amounts not credited to the profit and loss account, being

- The items falling within the scope of section 28

- The proforma credits, drawbacks, refund of duty of customs or excise or service tax, or refund of sales tax or value added tax, or refund of GST, where such credits, drawbacks or refunds are admitted as due by the authorities concerned

- Escalation claims accepted during the previous year

- Any other item of income

- Capital receipt, if any

- Total of amounts not credited to profit and loss account (5a+5b+5c+5d+5e)

- 6 Amounts debited to the profit and loss account, to the extent disallowable under section 36 due to non-fulfillment of the condition specified in relevant clauses

- 7 Amounts debited to the profit and loss account, to the extent disallowable under section 37

- 8 A. Amounts debited to the profit and loss account, to the extent dis-allowable under section 40

- B. Any amount disallowed under section 40 in any preceding previous year but allowable during the previous year

- 9 Amounts debited to the profit and loss account, to the extent dis-allowable under section 40A

- 10 Any amount disallowed under section 43B in any preceding previous year but allowable during the previous year

- 11 Any amount debited to profit and loss account of the previous year but dis-allowable under section 43B

- 12 Amount of credit outstanding in the accounts in respect of

- 13 Amounts deemed to be profits and gains under section 33AB or 33ABA or 33AC

- 14 Any amount of profit chargeable to tax under section 41

- 15 Amount of income or expenditure of prior period credited or debited to the profit and loss account (net)

- 16 Amount of expenditure disallowed u/s

- 17 Whether assessee is exercising option under subsection 2A of section 92CE Tick) Yes or No [If yes , please fill schedule TPSA]

Part A – QD Quantitative details

- (a) In the case of a trading concern

- (b) In the case of a manufacturing concern

Schedules to the Return Form (Fill as applicable)

Schedule HP: Details of Income from House Property

- 1 Address of property 1

- 2 Pass through income if any

- 3 Income under the head “Income from house property” (Ʃ 1k + 2)

Note:

- Furnishing of PAN/Aadhaar No. of tenant is mandatory, if tax is deducted under section 194-IB.

- Furnishing of TAN of tenant is mandatory, if tax is deducted under section 194-I.

Schedule BP: Computation of income from business or profession

- A From business or profession other than speculative business and specified business

- B Computation of income from speculative business

- C Computation of income from specified business under section 35AD

- D Income chargeable under the head ‘Profits and gains from business or profession’ (A37+B42+C48)

- E Intra-head set off of business loss of current year

Schedule DPM: Depreciation on Plant and Machinery (Other than assets on which full capital expenditure is allowable as deduction under any other section)

- 1 Block of assets Plant and machinery

- 2 Rate (%) 15, 30, 40, 45

- 3 Written down value on the first day of previous year

- 4 Additions for a period of 180 days or more in the previous year

- 5 Consideration or other realization during the previous year out 3 or 4

- 6 Amount on which depreciation at full rate to be allowed (3+ 4 – 5) (enter 0, if result is negative)

- 7 Additions for a period of less than 180 days in the previous year

- 8 Consideration or other realizations during the year out of 7

- 9 Amount on which depreciation at half rate to be allowed (7 – 8) (enter 0, if result in negative)

- 10 Depreciation on 6 at full rate

- 11 Depreciation on 9 at half rate

- 12 Additional depreciation, if any, on 4

- 13 Additional depreciation, if any, on 7

- 14 Additional depreciation relating to immediately preceding year’ on asset put to use for less than 180 days

- 15 Total depreciation* (10+11+12+13+14)

- 16 Depreciation disallowed under section 38(2) of the I.T. Act (out of column 15)

- 17 Net aggregate depreciation (15-16)

- 18 Proportionate aggregate depreciation allowable in the event of succession, amalgamation, demerger etc. (out of column 17)

- 19 Expenditure incurred in connection with transfer of asset/ assets

- 20 Capital gains/ loss under section 50* (5 + 8 – 3 – 4 -7 – 19) (enter negative only if block ceases to exist)

- 21 Written down value on the last day of previous year* (6+ 9 -15)

Schedule DOA: Depreciation on other assets (Other than assets on which full capital expenditure is allowable as a deduction)

- 1 Block of assets

- 2 Rate (%) (Nil, 5, 10, 40, 10, 25, 20)

- 3 Written down value on the first day of the previous year

- 4 Additions for a period of 180 days or more in the previous year

- 5 Consideration or other realization during the previous year out of 3 or 4 6 Amount on which depreciation at full rate to be allowed (3 + 4 -5) (enter 0, if result is negative)

- 7 Additions for a period of less than 180 days in the previous year

- 8 Consideration or other realizations during the year out of 7

- 9 Amount on which depreciation at half rate to be allowed (7-8) (enter 0, if result in negative)

- 10 Depreciation on 6 at full rate

- 11 Depreciation on 9 at half rate

- 12 Total depreciation* (10+11)

- 13 Depreciation disallowed under section 38(2) of the I.T. Act (out of column 12)

- 14 Net aggregate depreciation (12-13)

- 15 Proportionate aggregate depreciation allowable in the event of succession, amalgamation, demerger etc. (out of column 14)

- 16 Expenditure incurred in connection with transfer of asset/ assets

- 17 Capital gains/ loss under section 50 (5 + 8 -3-4 -7 -16) (enter negative only if block ceases to exist)

- 18 Written down value on the last day of previous year* (6+ 9 -12)

Schedule DEP: Summary of depreciation on assets (Other than assets on which full capital expenditure is allowable as a deduction under

any other section

- 1 Plant and machinery

- 2 Building (not including land)

- Furniture and fittings

- 4 Intangible assets

- 5 Ships (Schedule DOA- 12vii)

- 6 Total depreciation (1e+2d+3+4+5)

Schedule DCG: Deemed Capital Gains on sale of depreciable assets

- 1 Plant and machinery

- 2 Building (not including land)

- 3 Furniture and fittings

- 4 Intangible assets

- 5 Ships (Schedule DOA- 12vii)

- 6 Total depreciation ( 1e+2d+3+4+5)

Schedule ESR: Expenditure on scientific Research etc. (Deduction under section 35 or 35CCC or 35CCD)

- Expenditure of the nature referred to in section

- Amount, if any, debited to profit and loss account

- Amount of deduction allowable

- Amount of deduction in excess of the amount debited to profit and loss account (4) = (3) – (2)

Note: In case any deduction is claimed under sections 35(1)(ii) or 35(1)(iia) or 35(1)(iii) or 35(2AA), please provide the details as per Schedule RA.

Schedule CG: Capital Gains

- A. Short-term Capital Gains (STCG)

- B. Long-term capital gain (LTCG)

- C1 Sum of Capital Gain Incomes (11ii + 11iii + 11iv + 11v + 11vi + 11vii + 11viii+11ix+11x of table E below)

- C2 Income from transfer of Virtual Digital Assets (Item No. B of Schedule VDA)

- C3 Income chargeable under the head “CAPITAL GAINS” (C1 + C2)

- D. Information about deduction claimed against Capital Gains

- E. Set-off of current year capital losses with current year capital gains

- F. Information about accrual/receipt of capital gain

Schedule 112A: From sale of equity share in a company or unit of equity oriented fund or unit of a business trust on which STT is paid under section 112A

- S.No

- Share/Unitacquired

- Share Unit transferred

- ISI N Code

- Name of the Share/ Unit

- Name of the Share/ Unit

- Sales Price Per Share/ Unit

- Full Value of Consideration- if shares are acquired on or before 31.01.2018 (Total Sale Value) (4*5) -If Shares are acquired after 31st day of January 2018 – please enter full value of consideration

- Cost of acquisition without index at ion Higher of 8 and 9

- Cost of acquisition

- If the Long-term capital asset was acquired before 1st day of February 2018, Lower of 6 and 11

- Fair Market Value per share/ unit as on 31st day of January, 2018

- Total Fair Market Value of capital asset as per section 55(2)( ac)- (4*10)

- Expenditure wholly and exclusively in connection with the transfer

- Total deductions (7+12)

- Balance (6-13) Item 5 of LTCG Schedule of ITR5

115AD(1)(b)(iii) proviso: For NON-RESIDENTS – From sale of equity share in a company or unit of equity oriented fund or unit of a business trust on which STT is paid under section 112A

- S.No

- Share/Unit Acquired

- ISIN Code

- Name of the Share/ Unit

- Name of the Shares/ Unit

- Sales Price Per Share/ Unit

- Full Value Consideration (Total Sale Value )(4*5)

- Cost of acquisition without indexation (higher of 8 or 9)

- Cost of acquisition

- If the long term capital asset was acquired before 01.02.2018, -Lower of 6 & 11

- Fair Market Value per share/unit as on 31st January, 2018

- Total Fair Market Value of capital asset as per section 55(2)(ac)-(4*10)

- Expenditure wholly and exclusively in connection with transfer

- Total deductions (7+12)

- Balance (6-13) Item 5 of LTCG Schedule of ITR5

Schedule VDA: Schedule VDA Income from transfer of virtual digital assets

- Date of Acquisition

- Date of Transfer

- Head under which income to be taxed (Business/Capital Gain)

- Cost of Acquisition (In case of gift; a. Enter the amount on which tax is paid u/s 56(2)(x) if any b. In any other case cost to previous owner)

- Consideration Received

- Income from transfer of Virtual Digital Assets (enter nil in case of loss) (Col. 6 – Col. 5)

Schedule OS: Income from other sources

- 1 Gross Income chargeable to tax at normal applicable rates (1a+ 1b+ 1c+ 1d + 1e)

- 2 Income chargeable at special rates (2a+ 2b+ 2c+ 2d + 2e related to sl. no. 1)

- 3 Deductions under section 57

- 4 Amounts not deductible u/s 58

- 5 Profits chargeable to tax u/s 59

- 6 Net Income from other sources chargeable at normal applicable rates (1 – 3 + 4 + 5)

- 7 Income from other sources (other than from owning and maintaining race horses) (2 + 6)

- 8 Income from the activity of owning race horses

- 9 Income under the head “Income from other sources” (7+ 8e)

- 10 Information about accrual/receipt of income from Other Sources

Schedule CYLA: Details of Income after Set off of current year losses

- Head/ Source of Income

- Income of current year (Fill this column only if income is zero or positive)

- House property loss of the current year set off

- Business Loss (other than speculation or specified business loss) of the current year set off

- Other sources loss (other than loss from race horses and amount chargeable to special rate of tax) of the current year set off

- Current year’s Income remaining after set off

Schedule BFLA: Details of Income after Set off of Brought Forward Losses of earlier years

- Head/ Source of Income

- Income after set off, if any, of current year’s losses as per 5 of Schedule CYLA)

- Brought forward loss set off

- Brought forward depreciation set off

- Brought forward allowance under section 35(4) set off

- Current year’s income remaining after set off

Schedule CFL: Details of Losses to be carried forward to future years

- Assessment Year

- Date of Filing (DD/MM/ YYYY)

- House property loss

- Loss from a business other than the loss from speculative business and specified business

- Loss from speculative business

- Loss from specified business

- Loss from life insurance business u/s 115B

- Short-term capital loss

- Long-term Capital loss

- Loss from owning and maintaining race horses

Schedule UD: Unabsorbed depreciation and allowance under section 35(4)

- Assessment Year

- Depreciation

- Allowance under section 35(4)

Schedule ICDS: Effect of Income Computation Disclosure Standards on profit

- I Accounting Policies

- II Valuation of Inventories (other than the effect of change in method of valuation u/s 145A, if the same is separately reported at col. 4d or 4e of Part A-OI)

- III Construction Contracts

- IV Revenue Recognition

- V Tangible Fixed Assets

- VI Changes in Foreign Exchange Rates

- VII Government Grants

- VIII Securities (other than the effect of change in method of valuation u/s 145A, if the same is separately reported at col. 4d or 4e of Part A-OI)

- IX Borrowing Costs

- X Provisions, Contingent Liabilities and Contingent Assets

- XI s Total effect of ICDS adjustments on profit (I+II+III+IV+V+VI+VII+VIII+IX+X)

Schedule 10AA: Deduction under section 10AA: Deductions in respect of units located in Special Economic Zone

- SI

- Undertaking

- Assessment year in which unit begins to manufacture/produce/provide services

- Sl

- Amount of deduction

Schedule 80G: Details of donations entitled for deduction under section 80G

- A Donations entitled for 100% deduction without qualifying limit

- B Donations entitled for 50% deduction without qualifying limit

- C Donations entitled for 100% deduction subject to qualifying limit

- D Donations entitled for 50% deduction subject to qualifying limit

- E Total donations (Aiii + Biii + Ciii + Diii)

Schedule 80GGA: Details of donations for scientific research or rural development

- Relevant clause under which deduction is claimed

- Name and address of donee

- PAN of Donee

- Amount of donation

- Eligible Amount of donation

Schedule 80GGC: Details of contributions made to political parties

- Date

- Amount of contribution

- Eligible amount of contribution

- Transaction Reference number for UPI transfer or Cheque number/IMPS/NEFT/RTGS

- IFS code of Bank

Schedule 80IAC: Deduction in respect of eligible start-up [to be filled only if answer to A19(g) is ‘Yes’]

- Date of incorporation of Startup

- Nature of business

- Certificate number as obtained from Inter Ministerial Board of Certification

- First AY in which de-duction was claimed

- Amount of deduction claimed for current AY

Schedule 80LA: De duction in respect of offshore banking unit or IFSC

- Type of entity

- Type of income of the unit

- Authority granting registration

- Date of registration

- Registration number

- First AY during which de-duction is claimed

- Amount of de-duction claimed for current AY

Schedule RA: Details of donations to research associations etc. [deduction under sections 35(1)(ii) or 35(1)(iia) or 35(1)(iii) or 35(2AA)]

- Name and address of donee

- PAN of Donee

- Amount of donation

- Eligible Amount of donation

Schedule 80-IA: Deductions under section 80-IA

- a Deduction in respect of profits of an enterprise referred to in section 80-IA(4)(i)

- b Deduction in respect of profits of an undertaking referred to in section 80-IA(4)(iv)

- c Total deductions under section 80-IA (a1 + a2 + b1 + b2)

Schedule 80-IB: Deductions under section 80-IB

- a Deduction in respect of industrial undertaking located in Jammu & Kashmir or Ladakh [Section 80-IB(4)]

- b Deduction in the case of undertaking which begins commercial production or refining of mineral oil [Section 80-IB(9)]

- c Deduction in the case of an undertaking developing and building housing projects [Section 80-IB(10)]Deduction in respect of industrial undertaking located in industrially backward districts [Section 80-IB(5)]

- d Deduction in the case of an undertaking engaged in processing, preservation and packaging of fruits, vegetables, meat, meat products, poultry, marine or dairy products [Section 80-IB(11A)]

- e Deduction in the case of an undertaking engaged in integrated business of handling, storage and transportation of food grains [Section 80-IB(11A)]

- f Total deduction under section 80-IB (Total of a1 to e2)

Schedule 80-IE: Deductions under section 80-IE

- a Deduction in respect of undertaking located in North-East

- aa Assam

- ab Arunachal Pradesh

- ac Manipur

- ad Mizoram

- ae Meghalaya

- af Nagaland

- ag Tripura

- ah Total deduction for undertakings located in North-east (total of aa1 to ag2)

- b Total deduction under section 80-IE (ah)

Schedule 80P: Deductions under section 80P

- 1 Sec.80P(2)(a)(i) Banking/Credit Facilities to its members

- 2 Sec.80P(2)(a)(ii) Cottage Industry

- 3 Sec.80P(2)(a)(iii) Marketing of Agricultural produce grown by its members

- 4 Sec.80P(2)(a)(iv) Purchase of Agricultural Implements, seeds, livestocks or other articles intended for agriculture for the purpose of supplying to its members.

- 5 Sec.80P(2)(a)(v) Processing , without the aid of power, of the agricultural Produce of its members.

- 6 Sec.80P(2)(a)(vi) Collective disposal of Labour of its members

- 7 Sec.80P(2)(a)(vii) Fishing or allied activities for the purpose of supplying to its members.

- 8 Sec.80P(2)(b)Primary cooperative society enagaged in supplying Milk, oilseeds, fruits or vegetables raised or grown by its members to Federal cooperative society enagaged in supplying Milk, oilseeds, fruits or vegetables/Government or local authority/Government

- Company / corporation established by or under a Central, State or Provincial Act

- 9 Sec.80P(2)(c)(i)Consumer Cooperative Society Other than specified in 80P(2a) or 80P(2b)

- 10 Sec.80P(2)(c)(ii)Other Cooperative Society engaged in activities Other than specified in

- 80P(2a) or 80P(2b)

- 11 Sec.80P(2)(d)Interest/Dividend from Investment in other co-operative society

- 12 Sec.80P(2)(e)Income from Letting of godowns / warehouses for storage, processing /

- facilitating the marketing of commodities

- 13 Sec.80P(2)(f)Others

- 14 Total

Schedule VI-A: Deductions under Chapter VI-A

- 1 Part B- Deduction in respect of certain payments

- 2 Part C- Deduction in respect of certain incomes

- 3 Total deductions under Chapter VI-A (1 + 2)

Schedule AMT: Computation of Alternate Minimum Tax payable under section 115JC

- 1 Total Income as per item 13 of PART-B-TI

- 2 Adjustment as per section 115JC(2)

- 3 Adjusted Total Income under section 115JC(1) (1+2d)

- 4 Tax payable under section 115JC(1)

Schedule AMTC: Computation of tax credit under section 115JD

- 1 Tax under section 115JC in assessment year 2025-26 (1d of Part-B-TTI)

- 2 Tax under other provisions of the Act in assessment year 2025-26 (2g of Part-B-TTI)

- 3 Amount of tax against which credit is available [enter (2 – 1) if 2 is greater than 1, otherwise enter 0]

- 4 Utilisation of AMT credit Available

- 5 Amount of tax credit under section 115JD utilised during the year [total of item No. 4 (C)

- 6 Amount of AMT liability available for credit in subsequent assessment years [total of 4 (D)]

Schedule SI: Income chargeable to tax at special rates

- 1a 111A or section 115AD(1)(ii)- Proviso (STCG on shares/equity oriented MF on which STT paid) [where transfer was before 23rd July 2024 as applicable]

- 1b 111A or section 115AD(1)(b)(ii)- Proviso (STCG on shares units on which STT paid) [where transfer was on or after 23rd July 2024 as applicable]

- 2 115AD (STCG for FIIs on securities where STT not paid)

- 3a Proviso to 112(1) (LTCG on listed securities/ units with indexation) [where transfer was before 23rd July 2024 as applicable and tax thereon after taking into account Sl. no. B4(f) of Schedule CG, if

- any.]

- 3b 112(1) (LTCG on listed securities/ units) [where transfer was on or after 23rd July 2024 as applicable]

- 4a 112(1)(c)(iii) (LTCG for non-resident on unlisted securities or other than Listed debentures) [where transfer was before 23rd July 2024 as applicable]

- 4b 112(1)(c)(iii) (LTCG for non-resident on unlisted securities) [where transfer was on or after 23rd July 2024 as applicabl]

- 5a 115AB (LTCG for non-resident on units referred in section115AB) where transfer was before 23rd July 2024 as applicable]

- 5b 115AB (LTCG for non-resident on units referred in section115AB) where transfer was on or after 23rd July 2024 as applicable]

- 6a 115AC (LTCG for non-resident on bonds/GDR)[where transfer was before 23rd July 2024 as applicable]

- 6b 115AC (LTCG for non-resident on bonds/GDR) [ where transfer was on or after 23rd July 2024 as applicable]

- 7 115AD (LTCG for FII on securities)

- 8a 112 (LTCG on others)) [where transfer / event was before 23rd July 2024 as applicable

- 8b 112 (LTCG on others) [where transfer / event was on or after 23rd July 2024 as applicable]

- 9a 112A or section 115AD(1)(b)(iii)-Proviso (LTCG on sale of shares or units on which STT is paid)) [where transfer was before 23rd July 2024 as applicable]

- 9b 112A or section 115AD(1)(b)(iii)-Proviso (LTCG on sale of shares or units on which STT is paid)) [where transfer / event was on or after 23rd July 2024 as applicable]

- 10 STCG chargeable at special rates in India as per DTAA

- 11 LTCG Chargeable at special rates in India as per DTAA

- 12 115B (Profits and gains of life insurance business)

- 13a 115AC (Income by way of interest received by a non-resident from bonds purchased in foreign currency)

- 13b 115AC (Income by way of dividend received by non-resident from GDR purchased in foreign currency)

- 14 115BB (Winnings from lotteries, puzzles, races, games etc.)

- 15 115BBJ (Winnings from online games)

- 16 115BBE (Income under section 68, 69, 69A, 69B, 69C or 69D)

- 17 115BBF (Income from patent)

- a Income under head business or profession

- b Income under head other sources

- 18 115BBG (Income from transfer of carbon credits)

- a Income under head business or profession

- b Income under head other sources

- 19 115BBH-Tax on Income from Virtual Digital asset

- a. Income under head business or profession

- b. Income under head Capital Gain

- 20 115A(1)(b) (A) & 115A(1)(b)(B) (Income of a non-resident from Royalty)

- 21 Income from other sources chargeable at special rates in India as per DTAA

- 22a Pass Through Income in the nature of Short Term Capital Gain chargeable @ 15%

- 22b Pass Through Income in the nature of Short Term Capital Gain chargeable @ 20%

- 23 Pass Through Income in the nature of Short Term Capital Gain chargeable @ 30%

- 24a Pass Through Income in the nature of Long Term Capital Gain chargeable @ 10% u/s 112A

- 24b Pass Through Income in the nature of Long Term Capital Gain chargeable @ 12.5% u/s 112A

- 25a Pass Through Income in the nature of Long Term Capital Gain chargeable @ 10% – u/s other than 112A

- 25b Pass Through Income in the nature of Long Term Capital Gain chargeable @ 12.5% – u/s other than 112A

- 27 Pass through income in the nature of income from other sources chargeable at special rates

- 28 Any other income chargeable at special rates (Please choose from dropdown menu)

- Total

Schedule IF: Information regarding partnership firms in which you are partner

- Name of the Firm

- PAN of the firm

- Whether the firm is liable for audit? (Yes/No)

- Whether section 92E is applicable to firm? (Yes/No)

- Percentage Share in the profit of the firm

- Amount of share in the profit

- Capital balance on 31st March in the firm

Schedule EI: Details of Exempt Income (Income not to be included in Total Income or not chargeable to tax)

- 1 Interest income

- 2 i Gross Agricultural receipts (other than income to be excluded under rule 7A, 7B or 8 of I.T. Rules)

- ii Expenditure incurred on agriculture

- iii Unabsorbed agricultural loss of previous eight assessment years

- iv Agricultural income portion relating to Rule 7, 7A, 7B(1), 7B(1A) and 8 (from Sl. No. 40 of Sch. BP)

- v Net Agricultural income for the year (i – ii – iii + iv)

- vi In case the net agricultural income for the year exceeds Rs.5 lakh, please furnish the following details

- 3 Other exempt income (3a+3b)

- 4 Income not chargeable to tax as per DTAA

- 5 Pass through income not chargeable to tax

- 6 Total (1+2+3+4+5)

Schedule PTI: Pass Through Income details from business trust or investment fund as per section 115UA, 115UB

- Sl.

- Investment entity covered by section 115UA/115 UB

- Name of business trust/investment fund

- PAN of the business trust/ investment fund

- Sl.

- Head of income

- Current Year of income

- Share of current year loss distributed by Investment fund

- Net Income/Loss 9=7-8

- TDS on such amount if any

Schedule- TPSA: Details of Tax on secondary adjustments as per section 92CE(2A)

- 1 Amount of primary adjustment on which option u/s 92CE(2A) is exercised & such excess money has not been repatriated within the prescribed time

- 2

- Additional Income tax payable @ 18% on above

- Surcharge @ 12% on “a”

- Health & Education cess on (a+b)

- Total Additional tax payable (a+b+c)

- 3 Taxes paid

- 4 Net tax payable (2d-3)

- 5 Date(s) of deposit of tax on secondary adjustments as per section 92CE(2A)

- 6 Name of Bank and Branch

- 7 BSR Code

- 8 Serial number of challan

- 9 Amount deposited

Schedule 115TD: Accreted income under section 115TD

- 1 Aggregate Fair Market Value (FMV) of total assets of specified person

- 2 Less: Total liability of specified person

- 3 Net value of assets (1 – 2)

- 4(i) FMV of assets directly acquired out of income referred to in

- section 10(1)

- 4(ii) FMV of assets acquired during the period from the date of creation or establishment to the effective date of registration/provisional registration u/s 12AB, if benefit u/s 11 and 12 not claimed during the said period

- 4(iii) FMV of assets transferred in accordance with third proviso to

- section 115TD(2)

- 4(iv) Total (4i + 4ii + 4iii)

- 5 Liability in respect of assets at 4 above

- 6 Accreted income as per section 115TD [3 – (4iv – 5)]

- 7 Additional income-tax payable u/s 115TD at maximum marginal rate

- 8 Interest payable u/s 115TE

- 9 Specified date u/s 115TD

- 10 Additional income-tax and interest payable

- 11 Tax and interest paid

- 12 Net payable (10 – 11) (Enter 0 if negative)

- 13 Date(s) of deposit of tax on accreted income

- 14 Name of Bank and Branch

- 15 BSR Code

- 16 Serial number of challan

- 17 Amount deposited

Schedule FSI: Details of Income from outside India and tax relief

- Sl.

- Country Code

- Taxpayer Identification Number

- Sl.

- Head of income

- Income from outside India (included in PART B-TI)

- Tax paid outside India

- Tax payable on such income under normal provisions in India

- Tax relief available in India (e)= (c) or (d) whichever is lower

- Relevant article of DTAA if relief claimed u/s 90 or 90A

Schedule TR: Details Summary of tax relief claimed for taxes paid outside India

- 1 Details of Tax relief claimed

- 2 Total Tax relief available in respect of country where DTAA is applicable (section 90/90A)

- 3 Total Tax relief available in respect of country where DTAA is not applicable (section 91)

- 4 Whether any tax paid outside India, on which tax relief was allowed in India, has been refunded/credited by the foreign tax authority during the year? If yes, provide the details below

- (i) Amount of tax refunded

- (ii) Assessment year in which tax relief allowed in India

Schedule FA: Details of Foreign Assets and Income from any source outside India

- A1 Details of Foreign Depository Accounts held (including any beneficial interest) at any time during the calendar year ending on 31st December, 2024)

- A2 Details of Foreign Custodial Accounts held (including any beneficial interest) at any time during the calendar year ending on 31st December, 2024

- A3 Details of Foreign Equity and Debt Interest held (including any beneficial interest) in any entity at any time during the calendar year ending on 31st December, 2024

- A4 Details of Foreign Cash Value Insurance Contract or Annuity Contract held (including any beneficial interest) at any time during the calendar year ending on 31st December, 2024

- B Details of Financial Interest in any Entity held (including any beneficial interest) at any time during the calendar year ending on 31st December, 2024

- C Details of Immovable Property held (including any beneficial interest) at any time during the calendar year ending on 31st December, 2024

- D Details of any other Capital Asset held (including any beneficial interest) at any time during the calendar year ending on 31st December, 2024

- E Details of account(s) in which you have signing authority hel (including any beneficial interest) at any time calendar year ending on 31st December, 2024 and which has not been included in A to D above.

- F Details of trusts, created under the laws of a country outside India, in which you are a trustee, beneficiary or settlor

- G Details of any other income derived from any source outside India which is not included in,- (i) items A to F above and, (ii) income under the head business or profession

Schedule GST: Information Regarding Turnover/gross Receipt Reported for GST

- Sl. No.

- GSTIN No(s).

- Annual value of outward supplies as per the GST return(s) filed

Note: Please furnish the information above for each GSTIN No. separately

Part B – TI Computation of total income

- 1 Income from house property ( 3 of Schedule-HP) (enter nil if loss)

- 2 Profits and gains from business or profession

- 3 Capital gains

- 4 Income from other sources

- 5 Total of head wise income (1 + 2v + 3e +4d)

- 6 Losses of current year to be set off against 5 (total of 2xvii, 3xvii and 4xvii of Schedule CYLA)

- 7 Balance after set off of current year losses (5 – 6) (total of column 5 of schedule CYLA + 4b + 2iv)

- 8 Brought forward losses to be set off against 7 (total of 2xvi, 3xvi and 4xvi of Schedule BFLA)

- 9 Gross Total income (7 – 8) (also 5xvii of Schedule BFLA + 4b + 2iv)

- 10 Income chargeable to tax at special rate under section 111A, 112, 112A etc. included in 9

- 11 Deductions under Chapter VI-A

- 12 Deduction u/s 10AA (Total of Sch. 10AA)

- 13 Total income (9 – 11c – 12)

- 14 Income chargeable to tax at special rates (total of (i) of schedule SI)

- 15 Net agricultural income/ any other income for rate purpose (3 of Schedule EI)

- 16 Aggregate income (13 – 14 + 15) [applicable if (13-14) exceeds maximum amount not chargeable to tax]

- 17 Losses of current year to be carried forward (total of xi of Schedule CFL)

- 18 Deemed total income under section 115JC (3 of Schedule AMT)

Part B – TTI Computation of tax liability on total income

- 1 a Tax payable on deemed total income under section 115JC (4 of Schedule AMT)

- b Surcharge on (a) above (if applicable)

- c Health and Education Cess @ 4% on 1a+1b above 1c

- d Total Tax Payable on deemed total income (1a+1b+1c)

- 2 Tax payable on total income

- 3 Gross tax payable (higher of 1d or 2g)

- 4 Credit under section 115JD of tax paid in earlier years (applicable if 2g is more than 1d) (5 of Schedule AMTC)

- 5 Tax payable after credit under section 115JD (3 – 4)

- 6 Tax relief

- 7 Net tax liability (5 – 6c)

- 8 Interest and fee payable

- 9 Aggregate liability (7 + 8e)

- 10 Taxes Paid

- 11 Amount payable (Enter if 9 is greater than 10e, else enter 0)

- 12 Refund (If 10e is greater than 9) (refund, if any, will be directly credited into the bank account)

- 13 Details of all Bank Accounts held in India at any time during the previous year (excluding dormant accounts) (In case of nonresidents, details of any one foreign Bank Account may be furnished for the purpose of credit of refund)

- 14 Do you at any time during the previous year

- 15 Net refund after adjustment as pe r Sl. No. 14 (12-13) (refund, if any, will be directly credited into the bank account)

- 16 Do you have a bank account in India (Non- Residents claiming refund with no bank account in India may select No)

- 17 Do you at any time during the previous year,-

- (i) hold, as beneficial owner, beneficiary or otherwise, any asset (including financial interest in any entity) located outside India; or

- (ii) have signing authority in any account located outside India; or (iii) have income from any source outside India? [applicable only in case of a resident] [Ensure Schedule FA is filled up if the answer is Yes ]

18. Tax Payments

- A. Details of payments of Advance Tax and Self-Assessment Tax

- B. Details of Tax Deducted at Source (TDS) on Income [As per Form 16 A issued or Form 16B/16C/16D/16E furnished by Deductor(s)] A issued or Form 16B/16C/16D/16E furnished by Deductor(s)

- C. Details of Tax Collected at Source (TCS) [As per Form 27D issued by the Collector(s)]

Verification

I, _____________________________________(full name in block letters), son/ daughter of______________________________________, solemnly declare that to the best of my knowledge and belief, the information given in the return and the schedules thereto is correct and complete is in accordance with the provisions of the Income-tax Act, 1961. I further declare that I am making this return in my capacity as _ (drop down to be provided) and I am also competent to make this return and verify it. I am holding permanent account number (if allotted) (Please see instruction) I further declare that the critical assumptions specified in the agreement have been satisfied and all the terms and conditions of the agreement have been complied with. (Applicable, in a case where return is furnished under section 92CD).

Date Sign here

{kind=link}

There are many technical glitches in itr 5 utility for example audit turn less then one crores column answer is in protected sheet with secret code only CPC know the code

i am unable to validate the ITR-5 as because the loss shows is not equal to the loss of carried forward loss in BTI and CFL. The ITR-5 is filed as belated return where the loss may not be carried forward. pls help in getting the ITR-5 validated and varified before e varify and upload,

I am filing ITR 5. The problem regarding 80P is as

At sr. no. 1 amount in banking facilities can not be claimed in sheet: schedule 80P.

While uploading jason for ITR-5 an error massage “Invalid hash value identified, Modification to ITR details outside Utility is not allowed.”

Please advise how to resolve it.

Applicable of filling a IT Return of School is require to file ITR 5, as it is registered under Society Registration Act. During scrolling ITR 5 is not available (others are available e.g. ITR 1, ITR2, ITR3, ITR4 & ITR 7). Pls guide me what I will do? Is it require to file other ITR form? Pls advice.

I am filing ITR-5 with ZERO income. First I tried ITR-4 but it didn’t allow me to file saying for zero income you can’t file ITR-4.

Then I filled ITR-5 with utility, but now in error, it is giving me an error to show in how many firms you are partner. This firm is not a partner in any firm. But the error is not going. So how to resolve this issue.

Where to find the utility to create JSON file. The one available on the INcome tax dept site is not uploading. Portal says access denied