Goods and Service Tax is an ambitious tax regime applicable from the 1st of July 2017 made a number of indirect taxes subsumed into it. The government has revealed the due dates for the payment of GST. The GST payment due date for general taxpayers is the 20th of next month while the GST payment due date for composition scheme dealers is the 18th of next quarter. As per Budget 2022, the due date had been revised from the 20th of next month to the 13th of next month in the case of Non-Resident taxpayers.

Latest Update In GST Payment

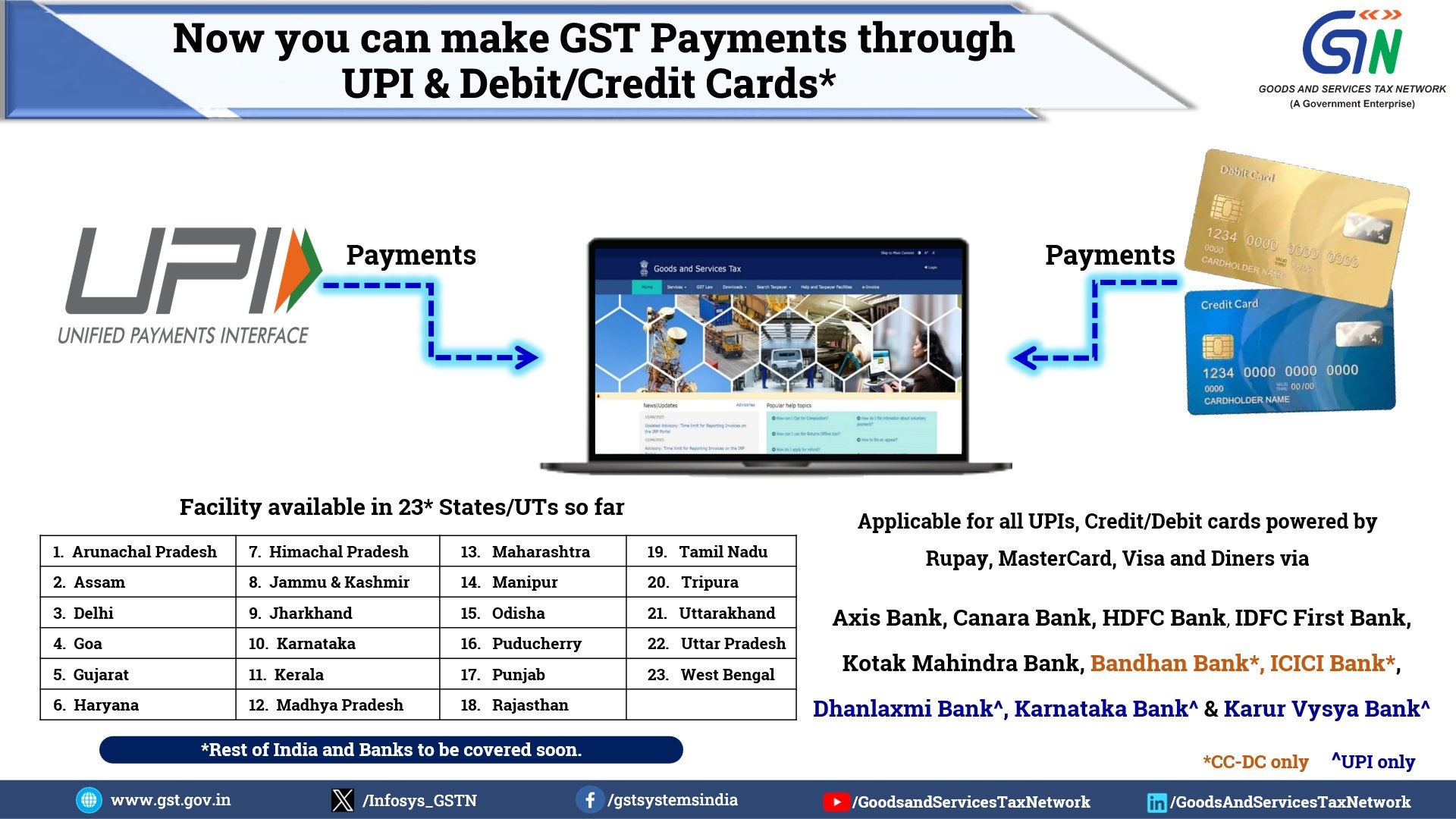

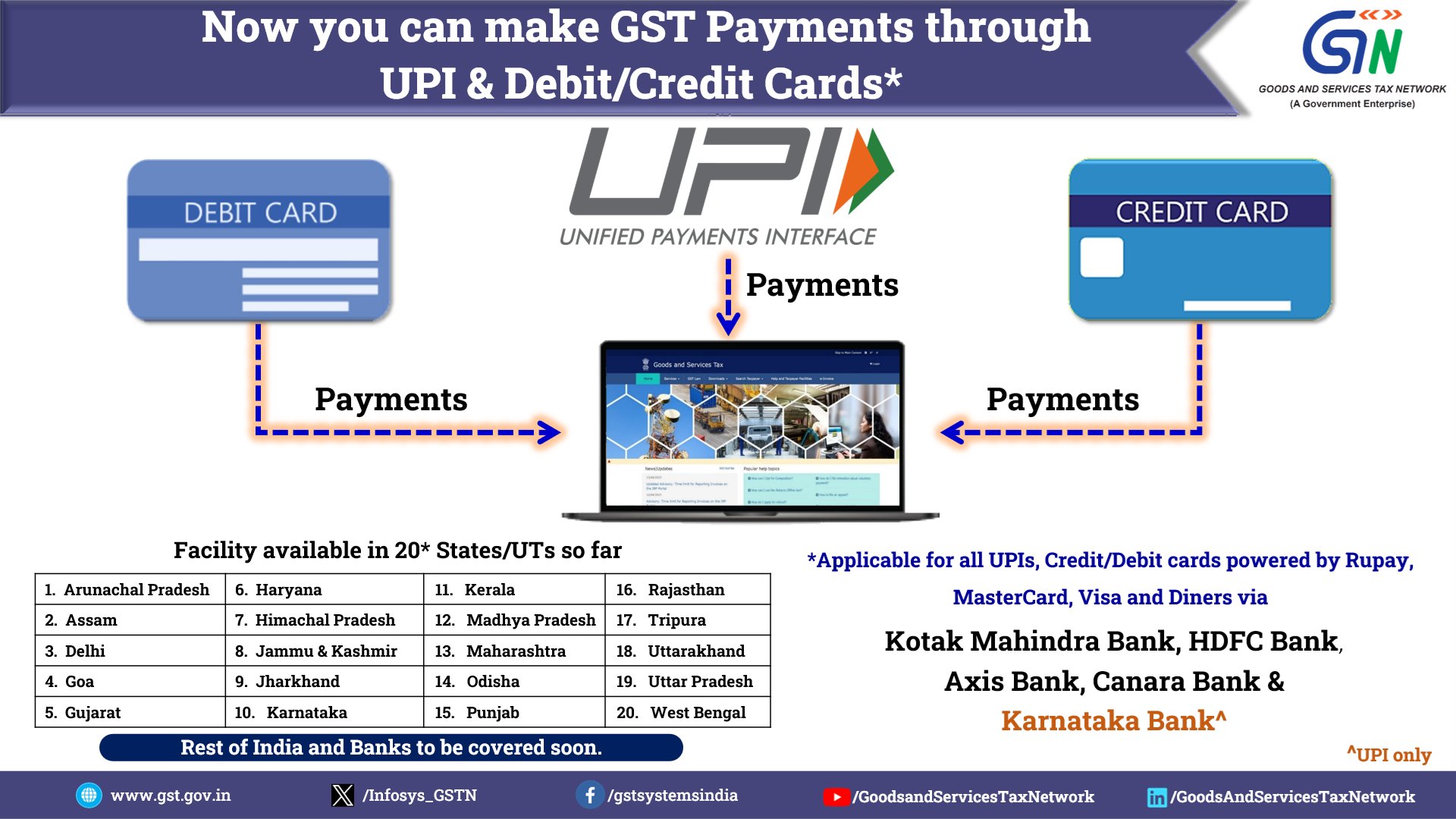

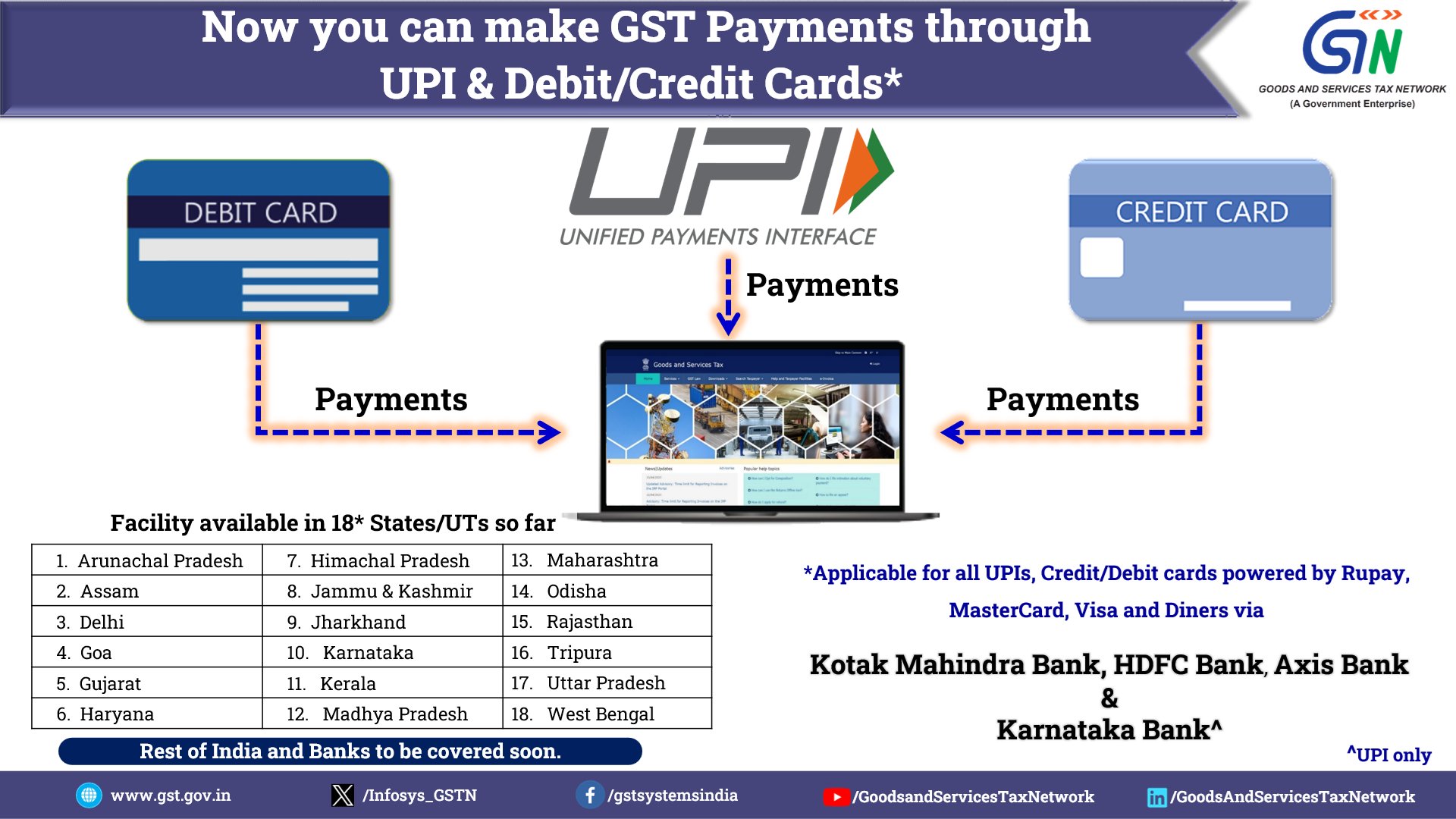

- Manipur taxpayers can now make GST payments via UPI and credit/debit cards. View More

- The GST department has added Yes Bank to enable UPI and debit/credit card payments. View More

- The Kerala GST department has shared a notification, SRO No. 1153/2024, related to the pending GST payment under the Finance Act 2024. Read PDF

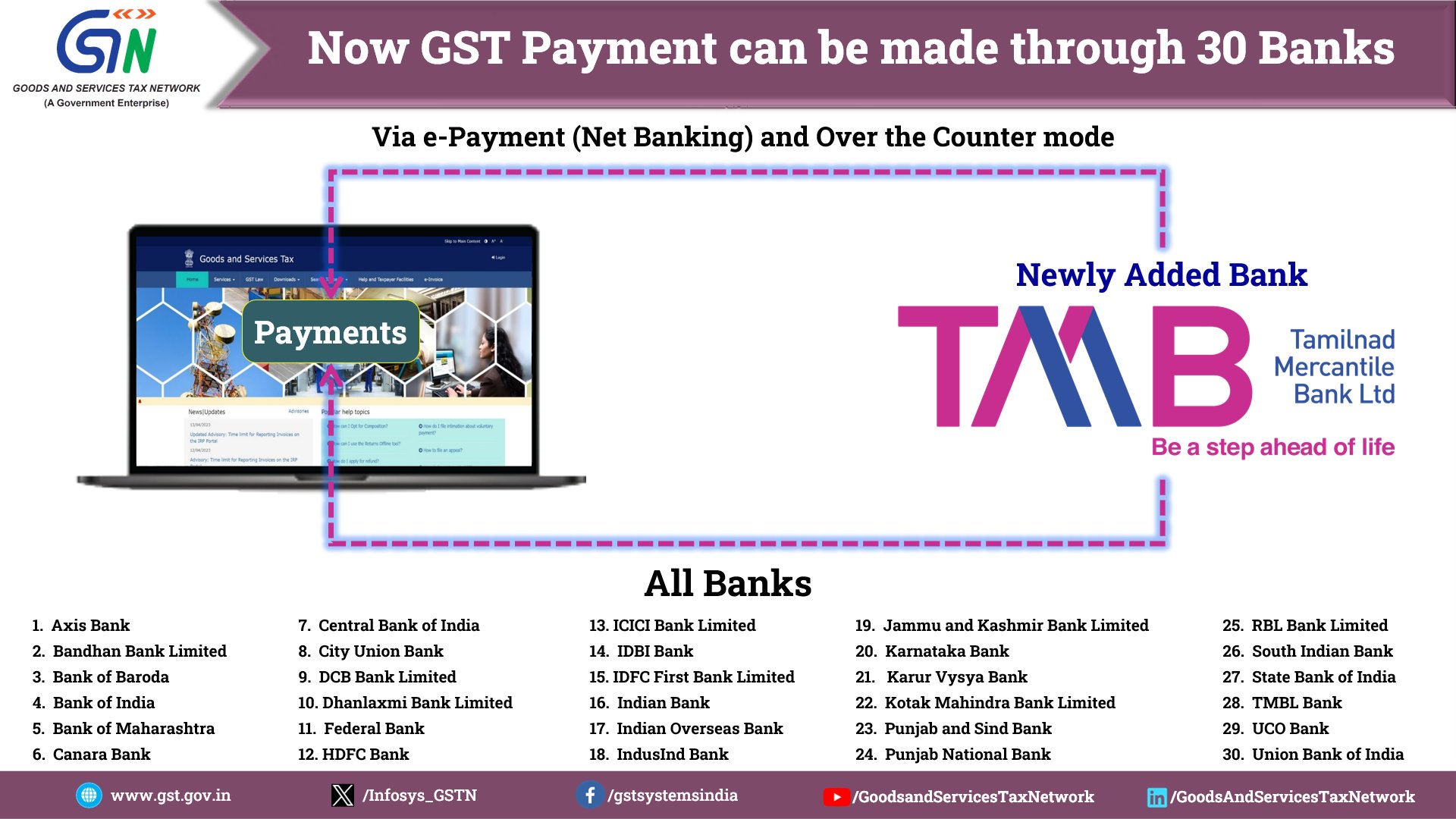

- Punjab and Uttarakhand taxpayers can now make GST payments via debit and credit cards. View More Also, the department has added a new TMB bank for the taxpayers. . View More

- Arunachal Pradesh taxpayers can now complete GST payments via UPI and debit or credit card facilities at the official GST portal. View more

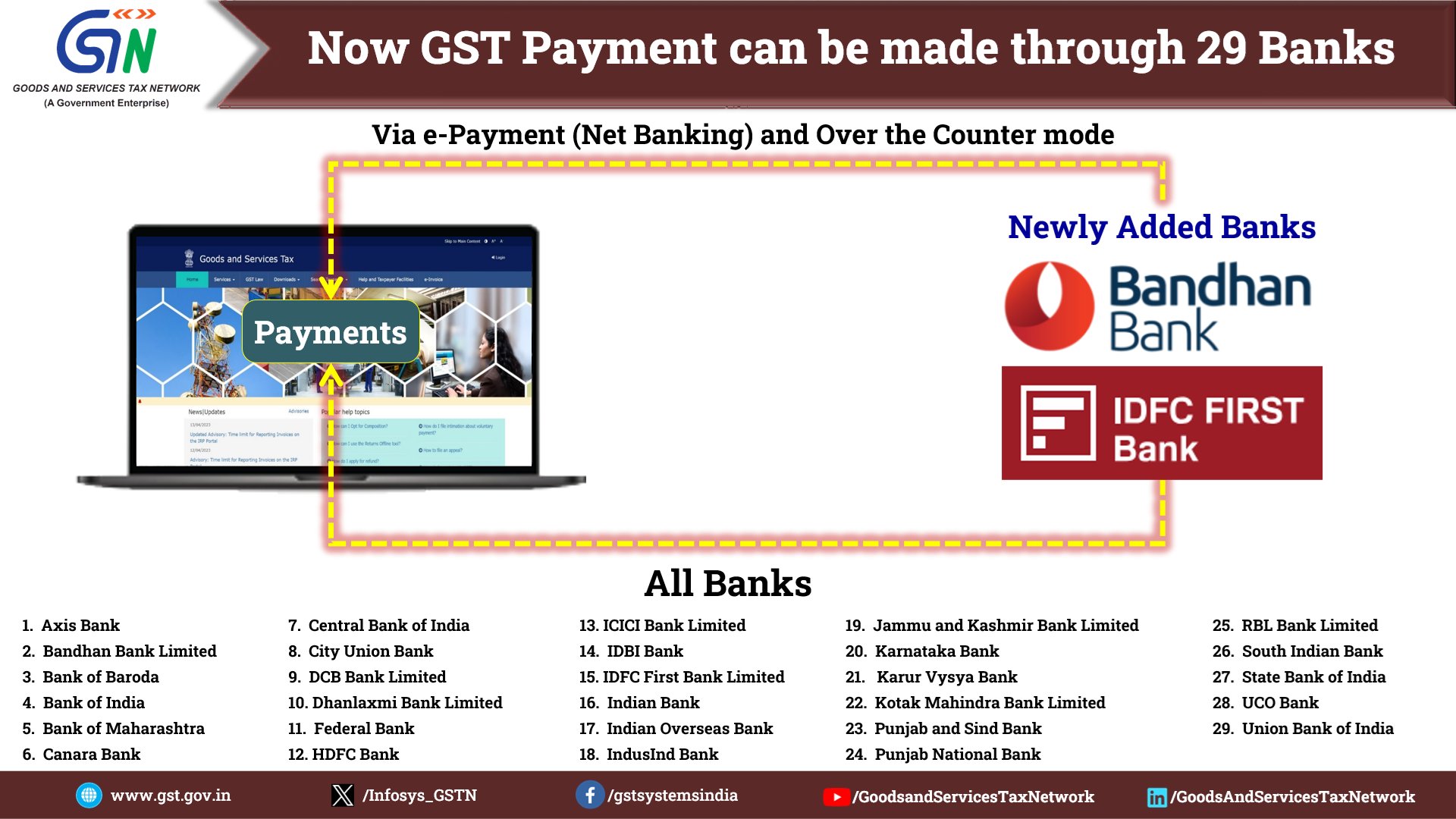

- IDFC First and Bandhan Bank have now enabled GST payment via Credit/Debit Card at the official portal. View more

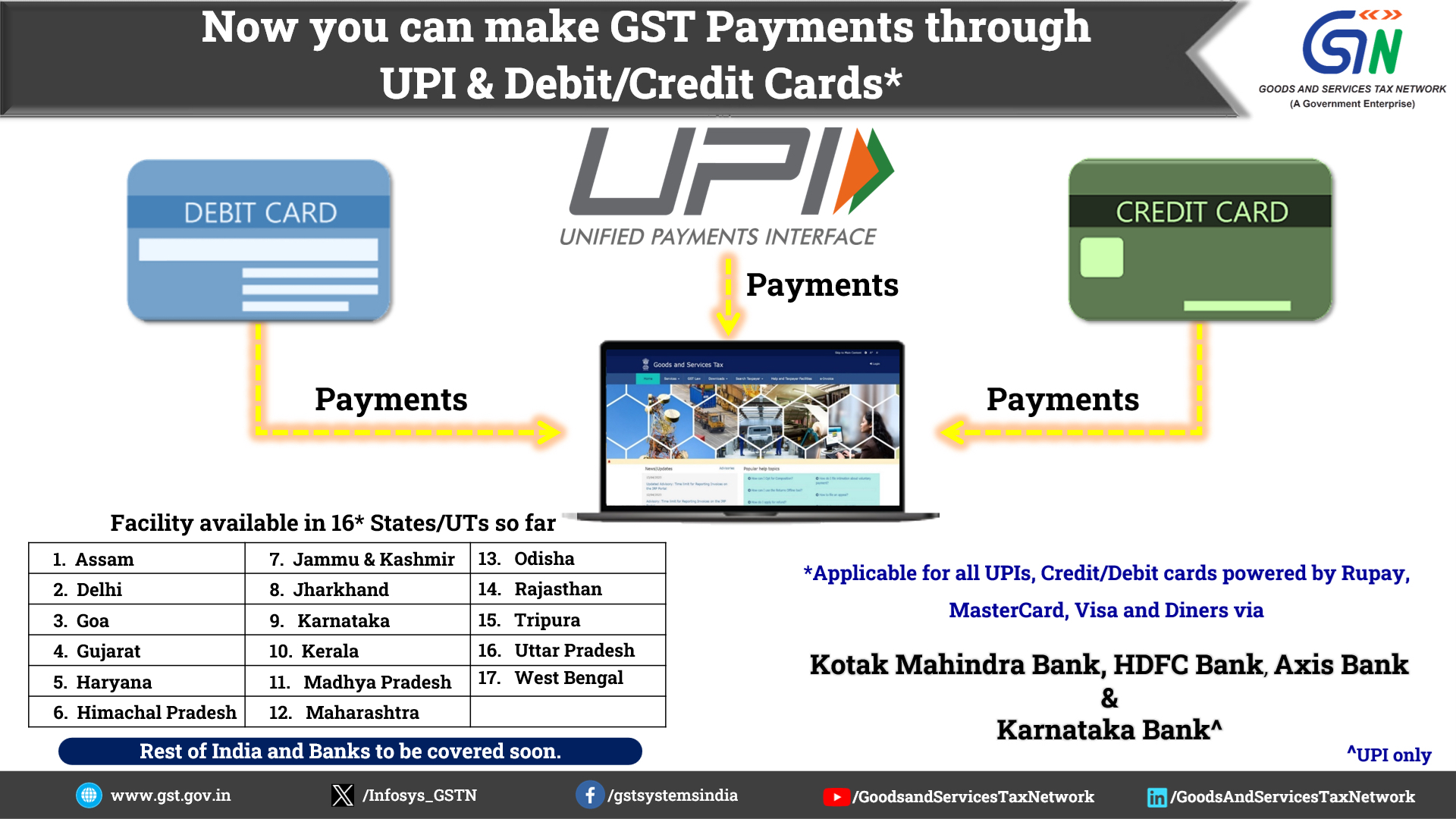

- GSTN updated its payment procedures to make people pay using UPI, and credit/debit cards, with the help of Axis and Karnataka Bank. Read more

- GSTN department enables the GST payment via UPI, debit card and credit card for West Bengal taxpayers.

- HDFC Bank now allows UPI and debit/credit card payments for GST at the official portal. View more

- Jammu & Kashmir taxpayers can now make GST payments via UPI and debit or credit card facilities. View more

- For taxpayers, the GST department has added a new bank, Dhanlaxmi to facilitate GST payments on the official portal. View more

- The GST department has added more banks to make a GST payment at the official portal. View more

- The GST department added a new state Uttar Pradesh for UPI facilities and CC/DC payment.

- Four additional states have been included (Jharkhand, Karnataka, Rajasthan and Tripura) to provide Credit Card, Debit Card, and UPI facilities for GST payment.

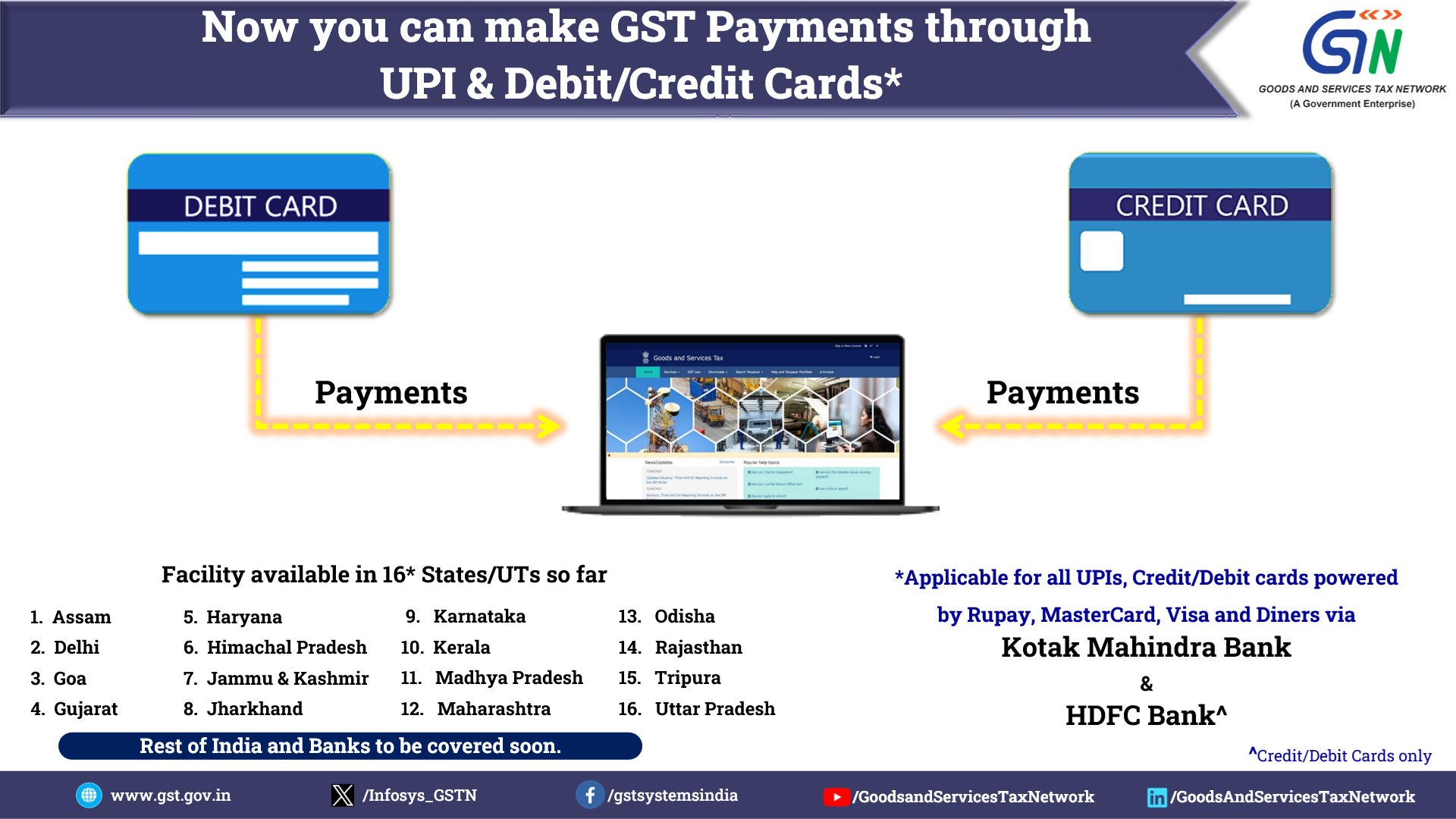

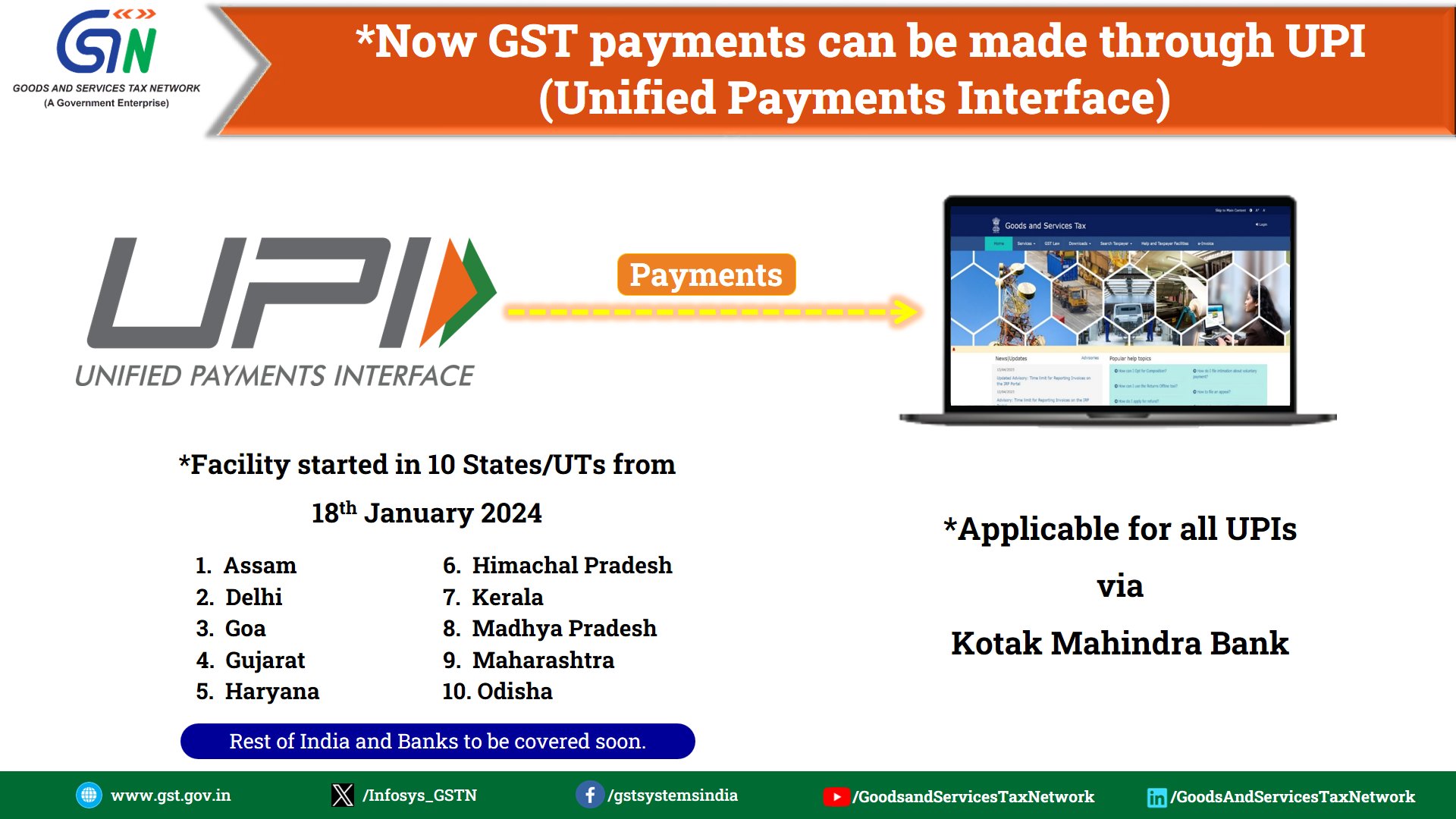

- Kotak Mahindra bank users can make GST payments via UPI facility in selected 10 states. View more

GST Payment Due Dates for Both General & Composition Scheme Taxpayers

| Type of Taxpayer | GST Payment Due Dates |

|---|---|

| Regular | 20th Day of the Next Month |

| Composition | 18th Day of the Next Month of Quarter |

| Non-Resident | 13th Day of the Next Month |

| Input Service Distributor | 13th Day of the Next Month |

| TDS Deductor | 10th Day of the Next Month |

| TCS Collector | 10th Day of the Next Month |

Recommended: Due Dates of GST for Return Filing for Taxpayers in India

Interest on Late Payment of GST

According to the GST Penalty regulations, interest will be charged at the rate of 18 percent per annum from the taxpayers who fail to pay their taxes on time. The interest will be levied for the days after the due date.

Check the example below to understand it better: Suppose your tax liability is Rs. 2,000 and you have not paid tax on time for a given month. Now, if you pay tax after one day from the due date, your interest will be calculated as 2000*18/100*1/365 = Rs. 0.98 Per day. If you delay more than that, you’ll have to pay an interest of the same amount per day. Check out the document attached below (chapter 10, point 50) for more details.

Fill Form for Free Demo of Gen GST Software

Penalty on Missing GST Due Date

In such cases, where taxpayers do not file their returns within specified due dates mentioned, he is obliged to pay a late fee of Rs. 50/day i.e. Rs. 25 per day in each case of CGST and SGST (in case of any tax liability) and Rs. 20/day i.e. Rs. 10/- day in each CGST and SGST (in case of Nil tax liability) subject to a maximum of Rs. 5000/-, from the given due date to the actual date when the returns are finally filed.

Rules and Regulations of GST Payment for Taxpayers

- The electronic cash ledger will be credited if payment for tax, interest, penalty and fee has been made by internet banking, credit card, NEFT, RTGS. While the amount can be used for the payment of interest, tax, penalty which is remaining in the electronic cash ledger of the taxpayer

- A payment for GST PMT-06 form is done through challan while the challan is only valid for the time period of 15 days. When the payment is done successfully, a Challan Identification Number (CIN) is generated. If in any case the CIN is not generated than the taxpayer can file Form GST PMT-07

- Online payments even made after 8 pm will be credited on the same day to the taxpayer’s account. While there will be no physical challan accepted for the GST payment while the challans will be generated from the gst.gov.in only for all the payments of taxes, fees, penalty, interest

- For the payment of challan under the 10000 rupees limit, it can be done over the counter with cash, cheques, demand draft through authorized banks while for the payments exceeding the amount of 10000 will be collected through digital mode only

Some of the Other Rules of the Challan are:

- Just immediately after the creation of CPI and common portal identification number, all new challan can be modified or edited. If there is any change in the amount there must be new challan generated also if the challan contains incorrect data will expire automatically after 15 days

- Each and every challan must be issued with a separate cheque or DD

- A partially filled challan can be saved in the post-login mode and can be accessed using the path > Services > Payments > My Saved Challans. A maximum of 10 challans can be saved on the GST portal with a validity period of 7 days

- The system will restrict any new generation of OTC challan if there is any unpaid OTC challan generated with the tax period amount exceeding rupees 10000. The challan will also automatically get cancelled or expire after 7 day validity period

- There will be UTR used in RTGS transactions with RBI. While the UTI must be linked, If in case the payment is not updated even after 2 hours on the landing page, there will be an option to link the UTR

- On behalf of a taxpayer, the third party can make the payments

Important Things of GST Payment for Freelancers

Beneath the present GST law any individual who is providing the services that comes under the taxes should enroll in the state as a hub of providing the service; if the average turnover exceeds 20 lakh for the fiscal year ( ₹10 lakh in some states like those in the North East), and that shall be liable to apply for freelancers upon the mentioned exceeding limit. 18% GST shall be applied to the freelancer which is same as applicable for the other service provider relied on the kind of service they furnsih.

Provisions for Electronic Credit Ledger

The amount should be credited to the Electronic credit ledger which is filed by the person in his Returns. While the amount stated in the electronic credit ledger can be used for tax payments only. Any differences in the electronic credit ledger must be brought to the notice of an officer through form GST PMT-04.

According to the following order, a taxpayer must discharge his tax duties:

- Self-assessed tax with other dues related to the returns of previous tax periods

- Self-assessment tax and other dues concerned with the current text period

- The amount payable under the rules and regulations act including the demand stated in section 73 or 74

- Late payment interest on GST

- Interest will be applicable at the rate of 18% if the payment is not done within the due date

- A rate of 24% interest will be applicable in the case when a taxpayer claims excess of input tax credit or makes a reduction in the output tax liability

GST Payment Process By An Unregistered Person on Portal

GSTN provides a complete GST payment procedure by an unregistered person by generating a user ID on the official government portal. Here, we disclosed step by step guide.

How to Generate a User ID on the Portal?

- Open https://www.gst.gov.in/ website on Safe Browser

- Now Click on Services > User Services > Generate User Id for Unregistered Applicant

- A new page will be opened for the name of the ‘New Registration for Unregistered Applicant’

- After, you have to select one option from Resident or Non-Resident status

- After select one, they can file the mandatory fields such as state, legal name as per PAN, trade name, details of the authorised signatory, and address of the authorized signatory and address.

- After filling required details, enter the captcha code, and then click on ‘Proceed’. You will receive OTPs on your registered mobile number and email.

Process of GST Payment

https://www.gst.gov.in/ > Payment > Create Challan Enter the ID generated above and make payment

GST Payment Verification Procedure

https://www.gst.gov.in/ > Payment > Track Payment Status Enter GSTIN/Other Id generated above along with CPIN and click on track status.

General Queries on GST Payment

Q.1 – What do you mean by the GST late fee and interest rate?

In context to the late fees, the non-payment of the late payment poses an interest. The total penalty burden surges through 18% per year as interest. An assessee is subjected to the same burden during the complete time of furnishing the taxes. The fees and the interest gets computed from the last date to the date of filing.

Q.2 – What shall be the result if the assessee does not furnish the GST Return?

The assessee who holds the GST enrolled number is required to furnish the GST return. If someone loses to furnish the GST return then a late fee will get imposed on the daily grounds. One shall not be enabled to furnish the ITR for the subsequent month if he or she does not or fails to furnish the GSTR for the current month. Apart from all these compliances an amount of Rs 50 shall be imposed every day as a late fee. Rs 5000 will be the highest amount that could be obtained as a late fee if the assessee losses to furnish his GST return.

Q.3 – As a taxpayer I do not have any amount to file as a GST return, Could I furnish my GSTR?

Yes, one is enabled to furnish the GST return. The filing is adjusted as a NIL return. There might be two cases to furnish the GSTR with no tax. In the first case, there shall have no buyings and no sale in that specific year hence no transaction is there. Thus one can furnish the NIL transaction return. In the other case, the goods and services have been purchased by you but no sale has been performed. Hence you have furnished the GST during the purchase thus you need to furnish the GSTR-3B and avail of the ITC.

Q.4 – What is the method to compute the late fees for the GST payment?

Rs 100 shall be imposed by CGST and Rs 100 by SGST post to the last date of furnishing of the GST return. Hence a total of Rs 200 per day shall be levied through the tax council against the taxpayer. For instance, if the assessee losses to furnish the return due on the date 15th August and do not furnish the same till 9th September then the late fees shall be computed as:

- 25 days * 200 = INR 5000 of late fees

Q.5 – Is there any interest imposed on the late fees with respect to the payment of GSTR?

GST penalty laws verified that each assessee who losses the last date to furnish the taxes needs to file the interest with 18% per annum as late fees. Hence if the individual due for the GST return is Rs 2500 and he or she files it after 3 days of the last date then the interest need to pay as a late fee on the tax shall be computed as:

- 2500*18/100*3/365 = Rs. 3.7 of interest on late fees

The interest amount gets computed towards the duration between the actual last date of paying the tax and the date on which the return was furnished.

Q.6 – Is it important to furnish the GST as a NIL transaction?

If you own a GST registration number then truly it is essential for a taxpayer that he furnish the GSTR. If you pose no buyings or sale transaction then you are required to furnish the NIL GSTR. if you do not furnish the GST return, then late fees shall get imposed. Beneath the CGST act Rs 25 will be imposed as well as Rs 25 shall get charged under the SGST act on a per-day basis. On the same penalty amount, 18% interest per annum will be imposed.

Q.7 – Can late fees on GST be avoided?

In some of the cases, GST late fees shall get avoided but if it does not then it should be furnished prior to the furnishing of the taxes

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

one of my friend due to covid he din’t filed GST nil return since2019 february ,and he is sole trader no business during the past 48 months due to illness. Now he recovered from health issues and want to start same business, but he try to use GST no , he received notices want to file nil return every month that system showing cgst rs.5000/- and sgstrs. 5000/- late fee, if he pay rs. 10,000 each month till january 2023 for 48 months the total amount aproxmately rs. 4,80,000/- is it possable a comman people to up date that much amount for gst late fee to start again his business ? how to shart itout? but his total turnover before 2018-19also not more than rs.90,00,000/-

“Please consult GST Practitioner for the same”

what will happen if you fail to to pay the gst and already got a warning , the what will happen

This will lead to Legal proceedings against the taxpayer from the concerned department

16.10.2022 SIR.WE ARE GST REGISTERED COMPANY.WE RECEIVED CAR SALES RS.5 LACS WITH GST ON DT.13.10.22 AND WE GENEREATED SALE INVOICE ON DT 14.10.22.CAN WE MAKE GST PAYMENT ON NEXT MONTH ON 20.11.2022 TO GOVT.PLEASE REPLY.THANKS.K.RENGARAJAN

No

Dear Sir,

We have a one-issue regarding non-receipt of payment from our vendor against output bills,

We are cleared all GST returns and uploading of bills for that particular party.

Please suggest recovering the payment from that vendor from 2018 – 19 FY to 2020 – 21 FY

We have all Purchase Orders and Bills.

Please suggest an option to recover the payments,

“Please consult GST practitioner”

sir file return for october due date showing 11.11.21. But while creating challan fee 340 rupees showing. please help.

This amount relates to the Late fee of the previous period of GSTR-1/GSTR-3B

GST is not paid for the month of April 21

9% interest for 15 days and calculation of interest per day or monthly.

Please help.

Interest is calculated on a monthly basis

sir i missed one invoice in gstr 3b of nov 2020 but shown the same invoice in gstr 1 of dec 2020 but did not paid the interest of the liability of the same invoice till date .what should i do now how to set off that liability with interest ? can it be done before the next gstr 3b due date i.e. befor 30th june 2021?

You can pay the interest in GSTR 3B Dec 2020 month

Sir m 7th mahine se GSTR3B Nhi bhar paya to palnty kitni lgegi

We have generated one challan to make a payment of GST, but the payment cannot be completed at the time of online payment.

Shall we use the same challan no. to pay the GST payment in future.

Please advice

Premkumar Nair

Yes, CIN no generated can be valid for 15 days

Sir,

Please note that we have paid tax dues through net banking before 20th, i.e, the due date and adjusted our liability from the cash and credit ledger before 20th but we have filed return, i.e only affixing DSC and filing the return on 22nd. Please let us know whether we will have to pay any interest and if yes then why?

Please refer to Rule 85(3) for the same

Hello sir,

My question is that I m not filled my GST returns for the period 12 months during the f.y 2019-20 even there is no transaction during the same so what is the total amount I have to pay?

You just have to pay the late fee amount of only Rs.20 per day if there is nil liability return and if there is a tax liability return then Rs.50 per day

Sir, I missed a bill to file in Oct 2017 and closed RC in Jan 2019. today 23.02.2021, my customer called regarding GST pending details.

kindly help to address the same

Dear sir, you can reply to them that now your GST registration is canceled hence you can not do anything

Gst payment

I have not able to reset my GST login and password, my phone is stolen, how to recover GST user name and password to self create GST challan,

email id which is used at the time of registration is also misplaced, not able to recover that too

Raise complaint to GST site

Dear Sir,

I have claimed 02-NOV-20 sales invoices on 03Feb21 GSTR3B, how much penalty is applicable. Also, I forget the same for DEC20 & Jan21 Invoices to claim in GSTR1 of JAN21. What should I do & how much penalty is applicable

Dear Sir, the portal is not asking for any interest & late fees for such transaction up till now

Dear Sir,

We have submitted GSTR-3B in the month of Nov 2020 against the F.Y. 2019-20, but the party was told you have filed after 30th September 2020, so, that we cannot take input and we are unable to pay the GST amount. Kindly advise us what we do. Because we have already paid the tax to the government but the party cannot refund the tax amount to us.

“Please contact to GST practitioner for the same”

Hello, I need help, I want to file the return for Oct, I have paid the late fees but I’m not able to file the return GST 3b. Pls guide

What kind of issue you are facing right now on the portal

Sir, I am not filled GST from March 2020 to today, and I have many losses in the business in this coronavirus period I am going out of station for January 2020 to date and I am the same sales online some amount bill (9 bills) March to July 2020. My business is not more than 10 lakes in the year. so, what can I do? I am not capable to pay penalty. I am in poverty. Please give me reply urgent basis.

please contact to gst practitioner urgently

will It work?

December to November get fine

Sir, the same problem i am facing now I need to pay penalty itself 15000. How I can get wavier in this issue

Please contact to GST portal for the same

I had subscribed for GST around July 2018. But never used it or did any business. How can I close my account now? Will I have to pay a heavy penalty?

Yes

Sir,

As on 04/11/2020, my Electronic Cash Ledger Balance is 10,000. which I paid in excess by mistake.

For the month of September 2020, I have sold a value of 30,000. I need to pay a tax of 5,700. How to Adjust the payable tax with the Cash Balance to file GSTR 3B.

Thanks.

Simple sir when there is an underpayment of tax when filing your GSTR 3B, the excess cash balance reflects and the same can be adjusted to set off the liabilities

I received a certain amount (a type of assessment: ORIGINAL: which is due to me, tax period 2020. so I want to understand when SARS say the payment due date is on the 31-10-2020 and the payment interest date on the 01-10-2020. what does this mean? please help.

meaning i will get paid .

Please contact to GST practitioner

I have taken registration on April 2018. I have filed GST returns up to May 2018. Thereafter I have dropped my business and not used the registration.

Now I have to resume my business till. When I logged in and tried to file June 2018 R3B my portal its asking for Rs.5780.00 late fee.

This amount is the penalty for the whole transaction of two years or per month? Kindly clarify.

This amount is for the whole transaction in a year

Dear sir,

We forgot to file the tax of aug-17gst 3b return for f.y.2017-18. Can we file the current month? party canceled gstin no in may-19. How much penalty & interest?

In GSTR-3B sequence of Filing is mandatory, hence you have to file GSTR 3B of all period and late fee applicable Rs.500 per return

SIR,

I AM FILING THE AUG 18 GSTTR 3B RETURN THE TAX LIABILITY WILL BE RS.90 (CGST & SGST) IN THE SITE IT SHOWING INTEREST & LATE FEE RS..5000/- IN EACH HEADING, AS PER COVID LAST NOTIFICATION IT IS RS.250 EACH.

There may be portal side issue, so please contact to GST portal for the same

sir,

we forgot to show RCM invoice in 3B of April, may, June, July 2020 and we want to show then in current month Aug, What interest do we have to pay…. is interest on Relief will be applicable or not

I am filing an annual return of 2018-19. There is a difference between rs. 72450/- between GSTR-1 taxable value & GSTR-3B taxable value.

how much tax I suppose to pay( Tax percentage) on Rs.72450 amount. what percentage of tax I should calculate on this amount.

The tax rate applicable on your existing goods applies to it also

Gstr 3b file for April 2019 nil return and next month show penalty 5000 so please reply

It is a portal issue, Please raise complaint ticket no. for the same

GST return from Oct 19 to Mar 20 are to be filed for client having turnover below 5 Cr. Tax is payable in each period. Late fees is capped max to Rs. 250+250. But what about interest rate ? How much will be rate & to be caluclated from which date ?? Pls clarify..

Please go through this link. It will clarify your issues https://www.gst.gov.in/newsandupdates/read/384

Dear Sir,

I have missed GST liability of Rs 2851 to show in GSTR-3B in FY 2018-19. And now in July 2020 i am going to pay. Kindly advise how to pay this liability and how much interest and penalty we have to pay.

Sir, in this case, late fee will be applicable @ Rs.500 per return, and interest is calculated @18% on balance days

I have a sale invoice in the month of Feb 2020 but I forgot to disclose it in GSTR 3B of Feb 2020, now I am showing it in the GSTR 3B of April 2020 and paying the amount on 04/07/2020. how much interest I have to pay on that. (Tax Amount – 100000)

If your Turnover is below Rs. 5 Crore, then till 30/09/2020 no interest is applicable for your GSTR 3B

Dear sir,

what was the max amount of late fees/penalty for GSTR 10 (final return), After cancellation?

In my return there was show 10,000 & DATE of canceled is 17.3.18 (3B & R1 is filled till March 2018)

pls, inform me if there are any new amendments in 2020 for GSTR 10 late fees/penalty.

Sir in respect of GSTR 10 no such amendments coming from the portal side, Kindly contact to GST portal