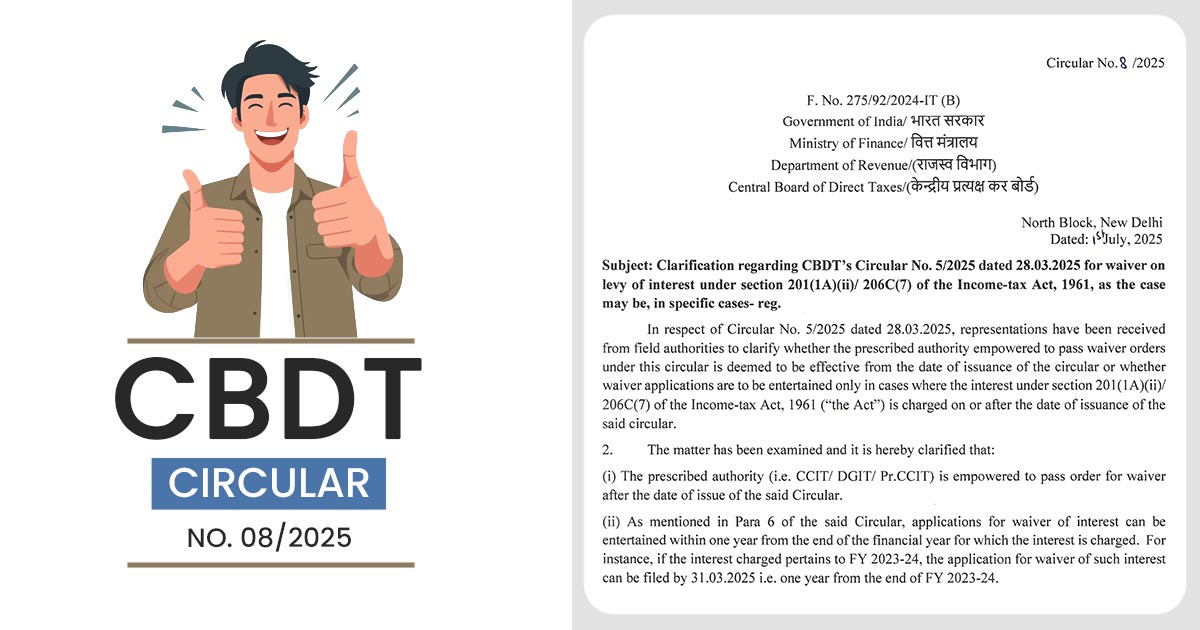

Circular No. 8/2025 dated July 1, 2025, has been issued via the Central Board of Direct Taxes (CBDT) to explain concerns of field officers for the exemption of interest under Sections 201(1A)(ii) and 206C(7) of the Income-tax Act, 1961, as initially addressed in its earlier Circular No. 5/2025 dated March 28, 2025.

The clarification answers queries on whether the authority to grant waivers is effective retrospectively or only from the date of the issuance of the circular.

The CBDT has established that the stipulated authority-namely, Chief Commissioners of Income Tax (CCIT), Director Generals of Income Tax (DGIT), or Principal Chief Commissioners (Pr.CCIT), is authorised to process exempted applications after the issuance of Circular No. 5/2025.

- The CBDT has described the timeline for filing the exempted applications:

- Within 1 year from the end of the fiscal year in which the interest was levied, the application is to be filed.

- For instance, if the interest is for FY 2023-24, March 31, 2025 is due date to file an exempted application.

The circular authorises for exempted applications of interest levied before March 28, 2025, the date of the earlier circular, provided they comply with the one-year submission window cited above.

Taxpayers and deductors from this move might get relief who may have defaulted in TDS or TCS payments and are encountering interest liabilities. The relaxation has the motive to ease the procedure and simplify the compliance load for the qualified applicants.

Tax professionals, chartered accountants, and business chambers admire the clarification since it addresses the interpretational gaps and ensures consistent application across tax jurisdictions.

More details in the PDF below