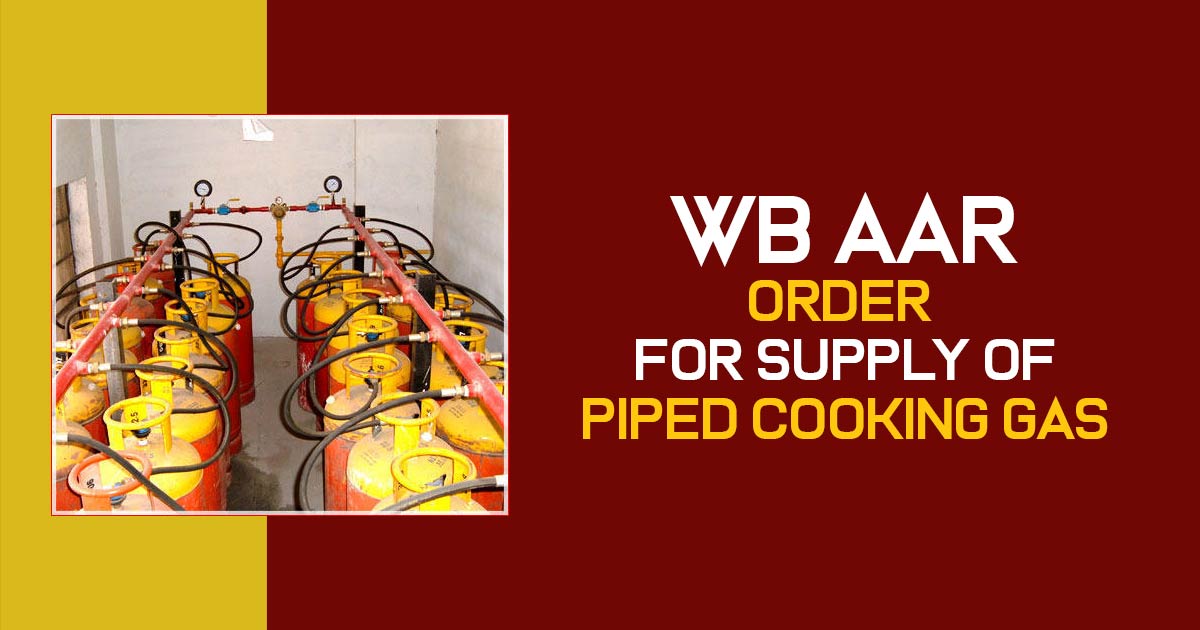

West Bengal’s Authority for Advance Rulings (WBAAR) specified that the supply of the cooking gas via pipelines from the gas banks to the residential place shall be the supply of the services and to be provided within the facility and management services

AAR has specified it a name as the composite supply beneath GST in which the principal supply is facilities and the management services. The composite supply is said to be the supply of two or more goods and services or dual. These come in a bundle and are then supplied in conjunction with each other in the normal business form and are said to be the principal supply. The rate for the principal supply shall be the rate for the complete supply.

If in case the petitioner furnishes the facility and property management services to owners of apartment for the residential complex which consists of the maintenance of and repair services associated to supply of cooking gas via pipeline and is further subjected to the owner of the apartment who is not claiming for the pipeline gas supply. In this description, the gas supply is within LPG Reticulated System.

AAR (Authority for Advance Rulings) revealed that the same system is the upgraded additions that are provided through the builders. This consists of the piped network that provides cooking gas to the person’s flat via a centralized gas bank. The cylinders are connected through the manifold that includes the two arms active bank and standby bank. The gas is supplied through the former which is used as a backup in the future.

Standby is utilized as a supply when the LPG (Liquefied Petroleum Gas) gets finished and in that time the empty cylinder is replaced with a new one. The complete system can be managed manually or automatically however the intention is that there must no shortage of supply. A gas meter is installed on the space provided in the apartment so as to record the usage that the payment can be made under that.

AAR sees that when the owner of the apartment wants to get supply from the pipeline then he/she shall be furnished with that as well as the services for which the same individual has paid. “Thus the supply of cooking gas through the pipeline is inextricably linked with facility and property management services as provided by the applicant, AAR said.”

As per that it commented that even the separate invoices as ‘GAS CHARGES BILL’ for use of gas, supply of gas within the pipeline is determined to be naturally bundled with facility and property management services and supplied in conjunction with each other.

Read Also: GST Impact on Petroleum Products in India

Tax expert suggested that normally one will acknowledge the supply of cooking gas as the supply of goods and not as a supply of facility management services, and thus this shall be held as an exciting view through implementing the strategy of supply which is naturally bundled and thus operated as composite supply.

“With this and some other recent rulings, it is becoming more and more clear that what qualifies as ‘composite’ or ‘mixed supply’ needs to be carefully examined keeping in mind the common practice in the industry, dependence of one supply on the other i.e. inextricable linkage, methodology of supply, invoicing mechanism etc, he answered.”