The Intention Behind Introducing Section 139(8A)

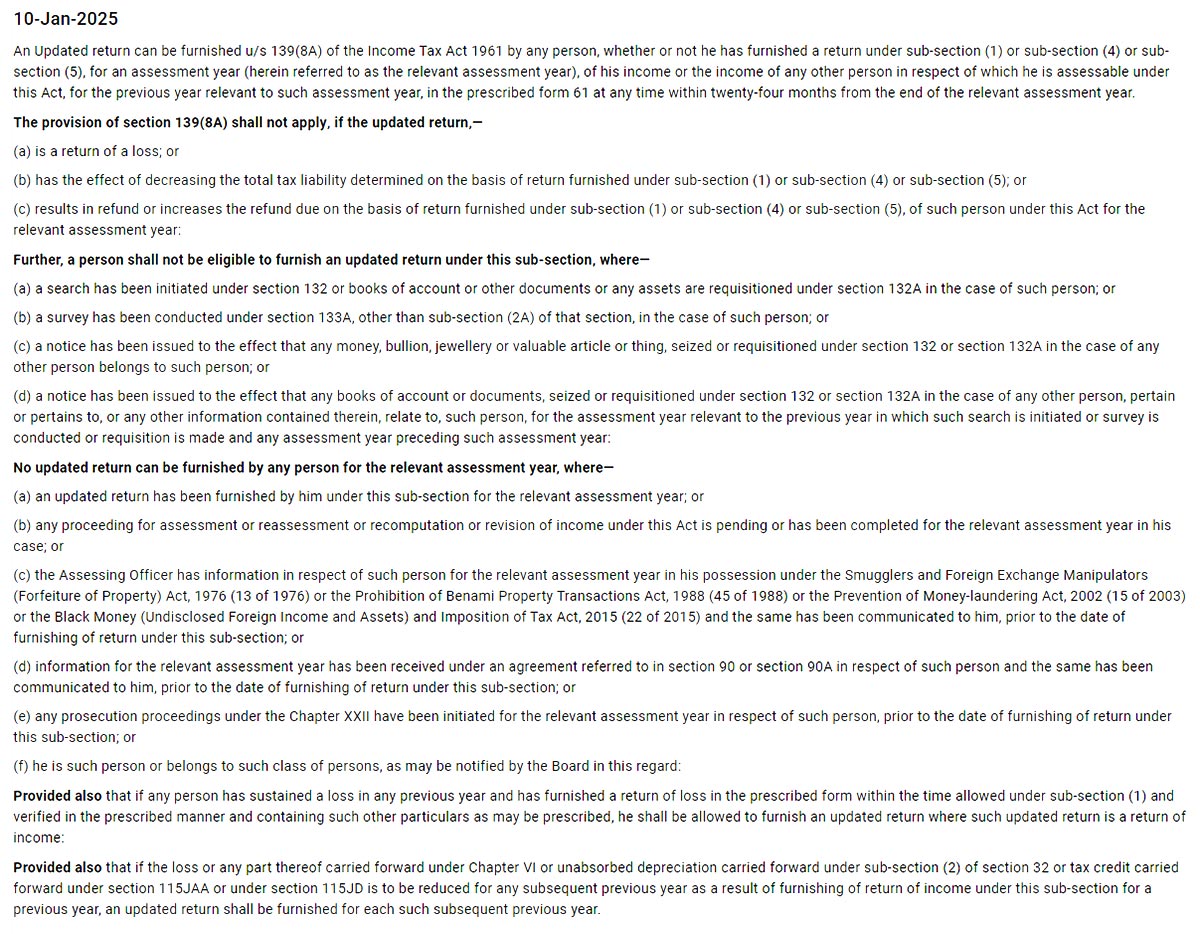

To provide more time to the assessee, a new provision under Section 139(8A) of the Act is proposed for furnishing an updated income tax return, regardless of whether the individual has previously filed a return for the relevant assessment year. The recommendation allows for the submission of an updated return within a longer duration than currently permitted under the Income Tax Act.

Latest Update

- The e-filing portal 2.0 has released a detailed guide on filing Updated Returns under Section 139(8A). Read more

Submit Query Regarding Income Tax Software

Duration of ITR Filing

Any individual might file the updated income tax returns of his income or the other individual’s income towards which the person is assessable beneath the act for AY related to the assessment year in 24 months from the finish of the assessment year with another tax. These returns would be filed in the mentioned form and manner and would have prescribed particulars.

New Section 139(8A) is Not Applied

The new proposed provision of Sec 139(8A) will not apply in case of the updated return,

- Is a return of a loss

- Holds the effect of decreasing the total tax liability found on the grounds of the return filed u/s 139(1), (4) or (5)

- The results in the refund or hikes in the refund due on the grounds of the return filed u/s 139(1), (4) or (5)

Crux: Updated income tax return can only be filed condition it raises tax liability.

Who Would Not be Subjected to Furnish the Updated ITR Under Section 139(8A)

An individual would indeed not be subjected to file the updated return u/s 139(8A) if: –

- Search gets executed u/s 132A or books of account other documents or any additional assets are requisitioned u/s 132A in context to these people.

- A survey is conducted u/s section 133A excluding 133A(2A) for the case of these people.

- A notice has been provided to the effect that any books of the account or documents seized or requisitioned u/s 132 or sec 132A in context to any other person, pertain or pertains to any.

- The additional details specified in it concern these people. The mentioned above exception is towards AY concerning PY where the same search gets executed or survey is being performed or requisition is performed and the two AYs examining a specific assessment year.

Indeed there would be no updated return that will be filed by any individual for the related assessment year in which

- An updated return needs to be filed by him u/s 139(8A) for the concerned assessment year.

- Any proceeding for the assessment or reassessment or recalculation or amendment of the income beneath the act is due or gets completed for the concerned assessment year in his

- Case

- The assessing officer poses the details towards this individual for the related assessment year under his possession beneath

- Money Laundering Act, 2002 prevention

- “The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015”

- The restriction of the Benami Property Transactions Act, 1988

- The Smugglers and Foreign Exchange Manipulators (Forfeiture of Property) Act, 1976

- And that is to be reported to him before his income tax filing date of the updated return.

- Beneath the exchange of the details, the data for the related assessment has been obtained beneath the DTAA for these individuals and that has been discussed with him before the filing date of the updated return.

- Any prosecution proceedings beneath Chapter XXII started for the related assessment year towards these individuals before the filing date of the updated return.

- He is the type of individual who belongs to the class of person who is being reported by the board for this.

Moreover the same would be asked to rectify sec 139(9) to give that return furnished u/s 139(8A) would be treated as a bogus return till this return comes within the proof of payment of tax as needed beneath the proposed section 140B.

Additional Tax to get Furnished with Updated ITR Under New Section 140B

A new section 140B needs to be proposed to furnish the tax needed to get furnished for the opting to file the updated return:

Where No Income Tax Return Filed Before:

When the taxpayer does not furnish the ITR u/s 139(1) or (4), he would be subjected to furnish the tax which is left along with the interest and the fee subjected to pay beneath any provision of the act for the late return filing or any default or late payment of advance tax including with the payment of the additional tax.

The tax subjected to pay would be calculated post to consideration of the below-mentioned points:

- (i) the amount of advance tax, if any

- (ii) any TDS or TCS

- (iii) any relief of income tax claimed under section 89

- (iv) any relief of foreign tax claimed u/s 90 or 91

- (v) any relief of foreign tax claimed u/s 90A

- (vi) any tax credit claimed to be set off u/s 115JAA or section 115JD.

These updated returns would indeed come with proof of payment of these taxes, additional tax, interest, and fee.

Where Income Tax Return File u/s 139(1) or (4) or (5)

- (i) TDS, TCS, Advance Tax, Self-assessment tax, and the amount of relief brought in the former return

- (ii) TDS or TCS on additional income offered

- (iii) Foreign tax credit u/s 90 or 91 on extra income offered

- (iv) Foreign tax credit u/s 90 or 91 on extra income offered

- (v) any tax credit availed to be set off u/s 115JAA or section 115JD i.e. is not claimed in the former return.

The above tax mentioned would be more than the refund amount if there is any then it is to be given for these former returns. Additional tax payment by an individual chosen for filing of the updated returns u/s 139(8A) is indeed needed with the below-mentioned rates:

- From December of the AY till 12 months from the finish of the related assessment year, the payment is to be furnished:

- 25% of average tax and interest subjected to pay.

- Payment is to be given post to the expiry of 12 months from the finish of the AY while before the finish of the 24 months from the finish of the related AY:

- 50% average of tax and interest subjected to pay.

It is indeed clear that towards the intention of the calculation of the additional income tax, the tax would consist of the surcharge and cess whatever the name mentioned for it on these taxes.

ITR Section 139(8A) Advantages & Disadvantages

Honourable Finance Minister had declared the Finance Budget of 2022-23 dated 01st February in the Lok Sabha in which the proposal to draw the provision of furnishing the updated income return was addressed.

What is the Provision to Furnish the Updated Return U/S 139(8A)?

It is suggested to insert the new provision from 01-04-2022 u/s 139(8A) that furnishes a choice to the assessee to file the updated return of his income in 2 years from the finish of the concerned AY even when the original tax return was furnished or not.

What Conditions Would Be Apply Beneath Updated Return Would Be Furnished?

The conditions to furnish the updated return are mentioned as:

- The updated return would be furnished when the other income is being shown in the return and this makes the assessees pay more tax.

- Towards the specific assessment year, only one updated return would be furnished.

- An additional tax would be imposed with the rate of 25% and 50% of the average tax and the interest subjected to pay correspondingly if the return is furnished in 12 months and 24 months from the finish of the assessment year.

- While furnishing the updated return the taxpayer is needed to give proof of the payment of the entitled tax and the interest including with the late return furnishing the fees and the additional tax.

- The updated return would not be furnished if it is a return of loss or decreased tax liability or surges refund.

- The updated return would not be furnished in search and seizure cases or where the prosecution proceedings have been executed with respect to the taxpayers or cases in which the assessment, reassessment, revision, or re-computation is pending or completed.

What are the Benefits of the Updated Return U/S 139(8A)?

The benefits of the updated return are mentioned as:

- It used to furnish more opportunity to rectify the income that looses to revealed in the earlier return.

- The same would furnish the advantage from any more lawful proceedings and prosecution.

- The updated return would support diminishing the litigation.

What are the Drawbacks of the Updated Return U/S 139(8A)?

The drawbacks of updated return are mentioned as:

- The additional tax rate imposed is much more and this results in the higher rise of the tax liability.

- This utility has been given by the government towards the people who seek to show the additional income with respect to the original return but this would not permit the assessee to diminish his or her income which is on the other side of the interest of the assessee.

What Does a Person Learn From This?

The government is attempting to furnish an opportunity to the assessee to reveal their income which is omitted to be shown previously while on the other side it would generate more revenue for the government. This would optimize the compliance to the assessee in a litigation-free environment.

{kind=link}

I have prepared Excel utility for ITR 3 under section 139(8A).can generate Jason file too.Part B ATI is correctly filled ,and additional Tax liability is paid.But while uploading Jason file facing 1querry. May be due to data at col 5 is not populated from Original ITR 2 filed .pl guide

“Please contact to portal for this issue.”

updated return download itr4 ay 2021 2022 but excel found unreadable content in itr4 ,do you want content recover the content of this workbook showing , after that all data filling but json file not saved and also json summary will not come , please give me advised

Please download the Excel Utility of ITR-4 of that Assessment Year again and please try it again after some time.

mera income 500000 h kya ham apna itr file u/s 139(8a) ke madhyam se bhar sakte h mera itr file karna chhut gaya h