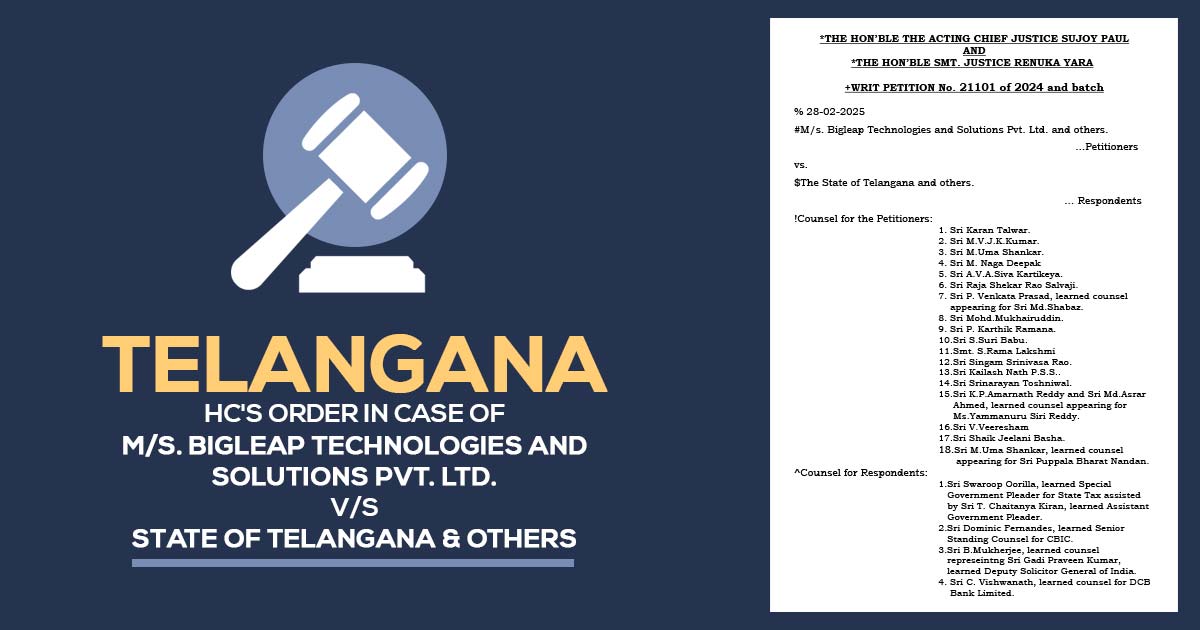

The Telangana High Court stated that GST show cause notices and orders lacking the proper officer’s signature cannot withstand judicial scrutiny.

The Division Bench of Acting Chief Justice Sujoy Paul and Justice Renuka Yara noted that “since Rule and prescribed Forms mandate requirement of signature of Proper Officer, its violation makes the notice/order vulnerable. Any contrary view taken by the Court about DRC-07 having no signature without considering the above rule and prescribed Form must be held as per incuriam.”

The taxpayer/applicant in the case has contested the legality, validity and propriety of the show-cause notices and final orders which admittedly do not include physical or digital signatures of the Proper Officer, although the impugned show-cause notices and final orders were placed on the portal.

It was furnished by the taxpayer that in the absence of any physical or digital signatures on the impugned Show cause notices and orders it could not withstand judicial scrutiny. A SCN/order should include the signature of the officer who has issued them. The document is not authenticated in the absence of any signature.

It was furnished via the department that the Goods and Services Tax Network (GSTN) via its advisory on 25.09.2024 cited that the SCNs and the orders are generated on the common portal via the officer’s login, which is accessed using the digital signature.

Related:- Supreme Court to Rule on Extension of GST SCN Adjudication Timeline Under CGST Act

It was claimed that such documents being computer generated upon the officer’s command do not need the digital signature since they could merely be issued via the officer via logging into the portal with their digital signatures. Therefore neither the SCNs nor the officers could bear a stamp of invalidity in the lack of physical or digital signatures of the officers.

It was mentioned by the bench that once there exists a particular column earmarked for the signature, the mentioned needs become a legal need.

With the department, the bench disagreed that as sections 73/74 of the GST Act are quiet about the requirement of digital/physical signature, any such requirement in DRC-01 and DRC-07 can be overlooked.

“If strict rule of interpretation is applied in view of statutory requirement of existence of signature in the statutory Forms, it cannot be said non-existence of signature will not cause any dent to the notice/order,” the bench cites.

The bench in the above-said view has permitted the petition.

| Case Title | M/s. Bigleap Technologies and Solutions Pvt. Ltd. V/S State of Telangana & Others |

| Citation | WRIT PETITION No. 21101 of 2024 and batch |

| Date | 28-02-2025 |

| Counsel For Appellant | Karan Talwar, M.V. J.K. Kumar, M. Uma Shankar, M. Naga Deepak |

| Counsel For Respondent | Swaroop Oorilla, Dominic Fernandes, B. Mukherjee and C. Vishwanath |

| Telangana High Court | Read Order |