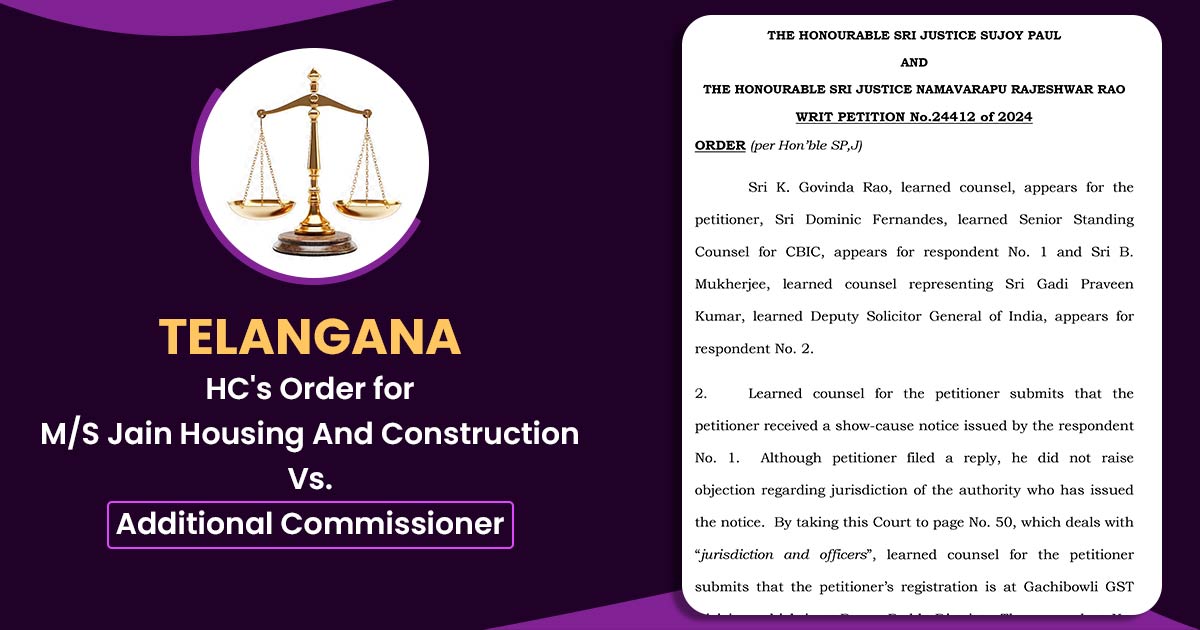

The Telangana High Court in a ruling ruled that the appellate authority is qualified to decide questions of jurisdiction against Goods and Services Taxes (GST) orders.

The decision was directed towards a writ petition contesting an SCN and the following order originally issued via the GST authorities. The applicant claimed that the officer who furnished the notice did not have the required jurisdiction, making the order invalid.

The counsel K.Govinda Rao representative of the applicant mentioned that a legal plea can be filed u/s 107 of CGST Act, 2017, but the appellate authority shall not have the competence to determine the jurisdiction question.

The registration of the applicant was with the Gachibowli GST Division, Ranga Reddy District, and the officer issuing the notice was allegedly not authorized to do so, which raised the question of jurisdiction. The petitioner requested relief from the High Court, arguing that the notice and order were issued by a body lacking authority.

Dominic Fernandes, Senior Standing Counsel for the CBIC, opposed the claims of the petitioner claiming that the show-cause notice (SCN) and the Order-in-Original were valid and issued via a competent officer.

He also claimed that the applicant has a clear legal remedy u/s 107 of the CGST Act, that permits for an appeal against these orders along with the questions pertinent to the jurisdiction.

The court presided over by Justice Sujoy Paul and Justice Namavarapu Rajeshwar Rao, addressed the primary opinion of the petitioner regarding the jurisdictional competence of the officer.

Read Also: Notable HC Cases on Condonation of Delay in GST Appeals

It was remarked by the court that the problem of jurisdiction was not a purely statutory question but instead a mixed question of fact and law. This differentiation is significant because, as noted by the court, issues that encompass both factual and legal aspects are most appropriately resolved by the appellate authority created within the statutory framework.

Additionally, the court emphasized that under Section 107 of the CGST Act, the appellate authority is empowered to resolve matters concerning the authority of officers responsible for issuing orders. The court chose not to intervene directly and instructed the petitioner to pursue the statutory remedy of filing an appeal, where the issue of jurisdiction could be addressed and resolved.

While resolving the writ petition, the Telangana High Court emphasized the significance of making use of the legal remedy provided under the CGST Act.

The observation was made that the appellate authority, in the context of an appeal, can address the jurisdictional matter in compliance with the law. The court granted a reprieve by declaring that the duration spent on the writ petition would be excluded from the time limits for filing the appeal.

The court kept the norm that the appellate authority is the pertinent judicial forum to determine the jurisdictional problems under GST law.

| Case Title | M/S Jain Housing And Construction Vs. Additional Commissioner |

| Citation | No.24412 of 2024 |

| Date | 05.09.2024 |

| For Petitioner | Sri K. Govinda Rao |

| For Respondents | Sri B.Mukherjee |

| Telangana High Court | Read Order |