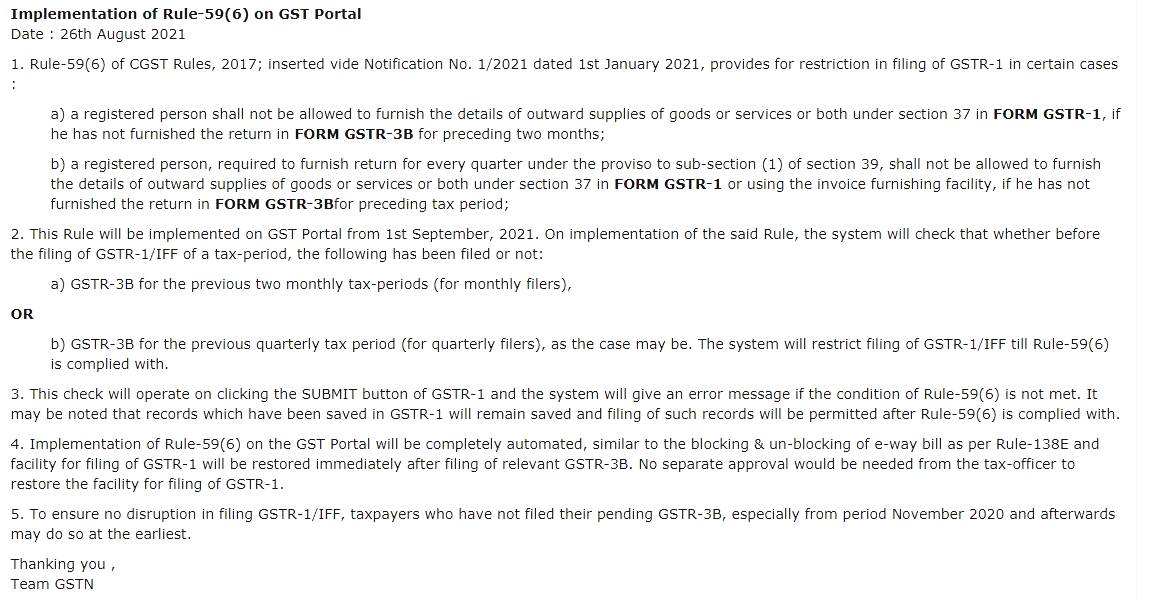

Rule-59(6) Implementation on GST Portal

On 1st January 2021 Rule-59(6) of CGST Rules, 2017 has been embedded vide Notification No. 1/2021, which gives for limitation in the filing of GSTR-1 in a specific case:

- Below section 37 in FORM GSTR-1, if the person has not filed the return in FORM GSTR-3B for the past two months then the enrolled person is not permitted to file the information of outward supplies of goods or services or dual.

- Beneath the proviso to sub-section(1) of section 39, an enrolled individual is needed to file the return for every quarter. The same registered person will not be permitted to file the information of outward supplies of goods or services or dual beneath section 37 in FORM GSTR-1 or using the invoice furnishing facility if he did not file the return in FORM GSTR-3Bfor preceding tax period.

From 1st September 2021, the same rule shall get executed on the GST portal. Upon the execution of the specified rule, the system shall check that prior to the furnishing of the GSTR-1/IFF of a tax-period the mentioned has been furnished or not:

- “a) GSTR-3B for the past 2-month tax periods (for monthly filers),”

- b) GSTR-3B for the past quarterly tax period (for quarterly filers) according to the concern. The system shall limit the filing of the GSTR-1/IFF till Rule-59(6) is complied with.

On tapping the submit button of GSTR-1 this check shall operate and the system shall provide you with the error message if the condition of Rule-59(6) has not been met. It might be noted that the records that have been saved in GSTR-1 shall get saved and furnishing of the records shall be allowed after the compilation of Rule-59(6).

The execution of Rule-59(6) on the GST portal shall be completely automated same as blocking and unblocking of the e-way bill under the Rule-138E and the facility to furnish the GSTR-1 shall be restored quickly post to the furnishing of related GSTR-3B. There is no other permission required from the tax officer to restore the facility for filing of GSTR-1.

So as to make sure that there will be no interruption in furnishing the GSTR-1/IFF, the assessee who has not furnished their pending GSTR-3B, specifically from the time of November 2020, and then might implement so at the earliest.

Latest Update in Advisory on GSTR-1 & HSN

As per Notification No. 78/2020 – Central Tax, on October 15, 2020, the assessee is required to report Harmonised System of Nomenclature (HSN) Code of Goods and Services provided by them on raising of tax invoices, with effect from 1st April 2021 on the under the designated lines.

| S.no | “Aggregate Turnover in the preceding Financial Year” | “Number of Digits of HSN Code to be reported in GSTR-1” |

|---|---|---|

| 1 | Up to INR 5 crores | 4 |

| 2 | Above INR 5 crores | 6 |

It is reported through some assessments that HSN is practised through them for reporting in GSTR-1 is not available in the table 12 HSN drop-down. They said that they are seeing the problems while adding the needed HSN information in table-12 and furnishing the statement of outward supplies in form GSTR-1 of July 2021. Moreover, for some JSON files, the HSN field is coming as a blank from the offline tool including some additional errors as given below:

- Processed with Error, In Progress or obtained but pending

- “Duplicate Invoice Number found in payload please correct”

To see the complete advisory on the action to be carried through the assessee to solve the mentioned problems issues, Tap on:

{kind=link}