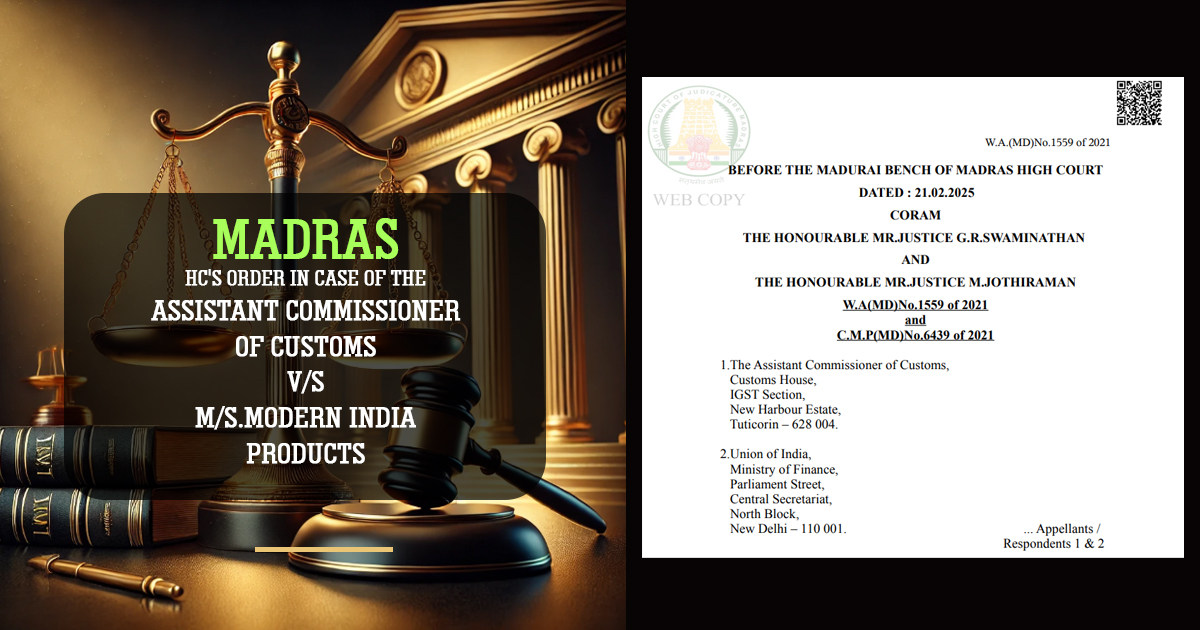

The Hon’ble Madras High Court of Madurai Bench in the case of M/s Modern India Products v. The Assistant Commissioner of Customs House IGST Section & Ors. [Writ Appeal (MD) No. 1559 of 2021 dated February 21, 2025], has permitted the refund claim via the taxpayer of the Integrated Goods and Services Tax (“the IGST”) refund for exports that shall be entitled as zero-rated supply.

While Circular No. 37/2018-Customs dated October 09, 2018 (“the Circular”) relied upon by Standing Counsel to state that if duty drawback is claimed, refund of IGST amount cannot be sought. The Court relied on the Hon’ble Gujarat High Court case wherein it was held that the Circular cannot prevail over Rule 96 of the CGST Rules.

Case Facts of Modern India Products

M/s Modern India Products (“the Petitioner”) is an exporter of goods known as “absorbent gauze roll”. The export was made dated September 26, 2017. The goods were valued at Rs.12,72,827/- and the applicant filed a sum of Rs.2,54,449/- for IGST.

It was ruled by the applicant that the exports shall come under zero rated supply and they are qualified to refund of the IGST amount as per Sections 16 and 54 of the IGST Act read with Rule 96 of CGST Rules.

It does not acted on when the applicant applied for the refund. Therefore the applicant submitted W.P(MD)No.9796 of 2020. Via the related single bench the writ petition was permitted dated April 17, 2021. Therefore the current intra-court plea has been submitted via the applicant on aggrieved from the circumstances.

Issue Related IGST refund

Whether IGST refund can be asked if duty drawback is claimed?

Madras High Court Decision

The Hon’ble Madras High Court of Madurai Bench in Writ Application (MD) No. 1559 of 2021 held as under:

Marked that, the Circular specifies that if duty drawback is claimed then refund of IGST amount cannot be sought.

Relied on, M/s. Amit Cotton Industries v. Principal Commissioner of Customs [R/Special Civil Application No. 20126 of 2018 dated June 27, 2018] wherein the Division Bench of the Hon’ble High Court ruled that the Circular cannot prevail over Rule 96 of the CGST Rules.

The Hon’ble Division Bench noted that the circular will not save the circumstance for the Department. Madras High Court followed the same decision in the decision notified in M/s. Precot Meridian Limited v. The Commissioner of Customs, The Assistant Commissioner of Customs[W.P. (MD) No. 20504 of 2019 dated November 19, 2019].

It was ruled that various other High Courts have attained the same view. As the single-judge bench granted relief to the applicant only via following the current legal position, interruption with the cited order is not warranted.

Madras High Court Comments on the Case of Modern India Products

The Ministry of Finance introduces the duty drawback scheme as a rebate for duty chargeable on any imported materials or excisable materials used in the manufacture or goods processing, manufactured in India, and exported. The products exported are the revenue natural.

To grant Duty Drawback under sections 74 and 75 of the Customs Act, 1962 (“the Customs Act”) the central Government is empowered. Section 74 of the Customs Act concerns drawback allowable on re-export of duty-paid goods, wherein duty drawback to the extent of 98% of the duty paid on imported goods can be claimed for re-export, given the goods are re-exported within 2 years of payment of import duty.

Additionally, Section 75 of the Customs Act discusses drawbacks on imported materials used in the manufacture of goods which are exported, it assigns duty drawback on the export of manufactured articles.

There are three types of Duty Drawback:

- All Industry Rates

- Brand Rates

- Special Brand Rates

Under the Customs Act in the GST regime, no revision has been made to the drawback provisions.

The Hon’ble Delhi High Court in the Pari Materia case of Intec Export India Pvt. Ltd. v. Union of India [W.P. (C) 9065/2023 dated October 30, 2023] asked the Revenue to refund IGST despite higher duty drawback selection where column A and B provided identical rates.

| Case Title | The Assistant Commissioner of Customs vs. M/s.Modern India Products |

| Citation | W.A(MD)No.1559 of 2021 C.M.P(MD)No.6439 of 2021 |

| Date | 21.02.2025 |

| Counsel For Appellant | Mr.R.Nandakumar |

| Counsel For Respondent | Mr.N.Sudalai Muthu |

| Madras High Court | Read Order |