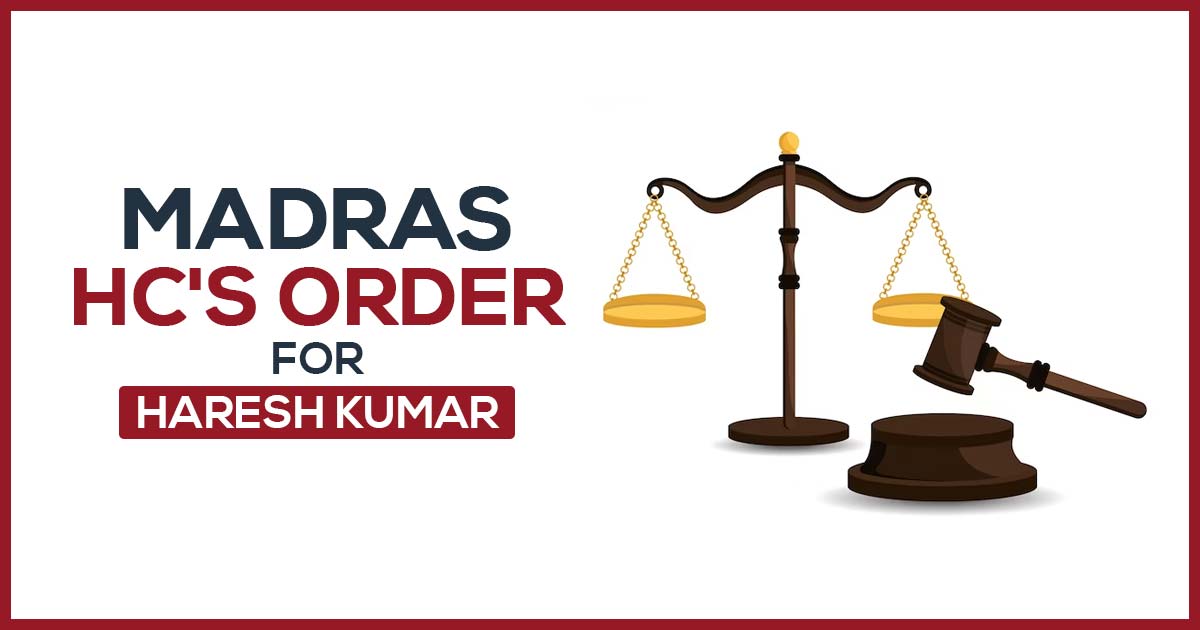

A single bench of Justice C. Saravanan of Madras High Court ordered the purchaser to create a pre-deposit of 200% of the maximum fine or a replacement furnish Bank Guarantee in terms of Section 129(c) of the respective Goods and Services Tax ratification and the Rules made under that.

After furnishing Bank Guarantee for the remaining balance of the penalty or making the required cash payment, the respondents’ Goods and Services Tax authorities were instructed to release the detained consignment.

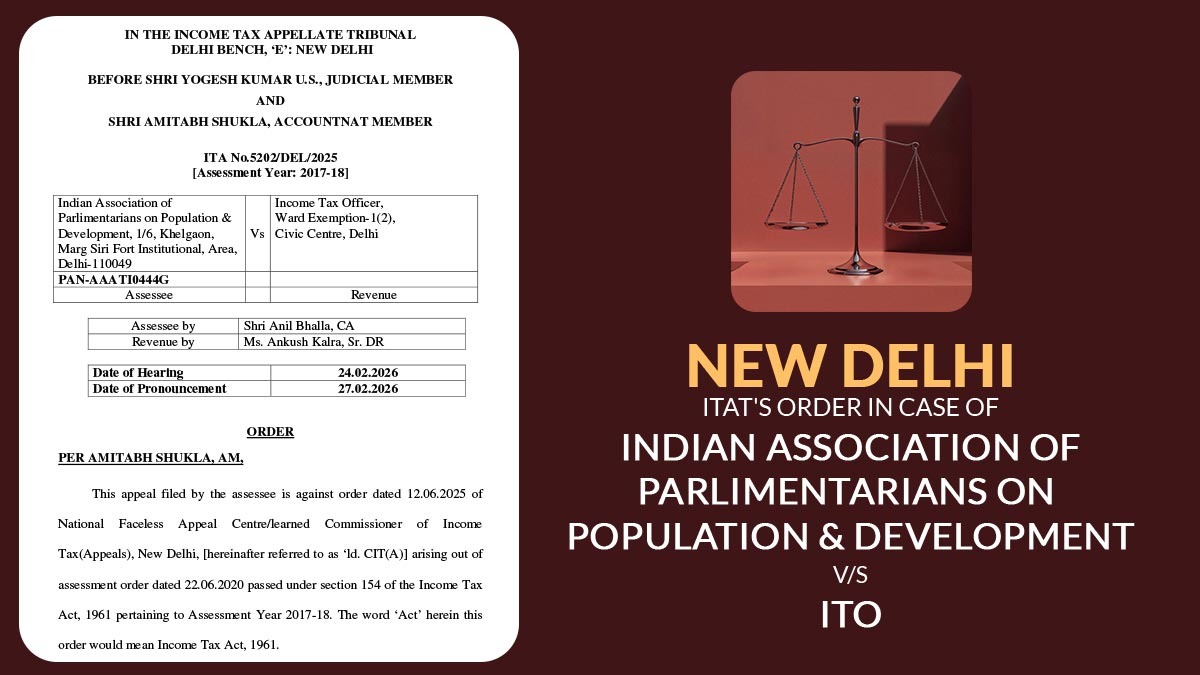

The first respondent stopped and held a consignment of goods that the petitioner had shipped that had a tax invoice dated April 18, 2023. A detention order was issued on April 18, 2023, in the form of GST MOV-06. As a result, the consignment that was being transported was held back, despite being accompanied by the E-Way Bill.

The bench observed that the reason for detaining the goods from the respondents was due to the petitioner’s supplier incorrectly transferring the Input Tax Credit. This compelled the petitioner to utilise the credit to offset the tax liability on the supplies made by the supplier.

The department must initiate the proper legal actions to reclaim the input tax that the supplier mistakenly transferred to the petitioner. According to the respondent’s counsel, the petitioner may face a maximum penalty of 200% of the tax due under Section 129(1)(a) of the Central Goods and Services Tax, 2017 (CGST).

The petitioner also filed a statutory appeal under Section 107 of the Central Goods and Services Tax (CGST) Act, 2017, according to the counsel of the petitioner. The petitioner also paid 25% of the disputed penalty to the Appellate Authority, whereas the respondents assessed a penalty equal to 100% of the value of the goods that were detained.

The petitioner further claimed that the respondents should have released the items after there was a pre-deposit of the sum under Section 107(6) of the Central Goods and Services Tax Act. Also, it is claimed that the petitioner has paid Rs. 17,42,350.

Read Also: Madras HC: GST ITC Needs Immediate Solution Benefitting Govt Twice

The bench observed that since the appeal would take longer to resolve, the necessary pre-deposit was made in order to safeguard the interest in the revenue.

The officer who detained the goods has been rendered functus officio, however, once a mandatory pre-deposit has been made, the order is null and void, and all subsequent recovery actions are subject to the final decision of the appeal.

The High Court ruled that “Therefore, to balance the interest of the revenue and the petitioner, I am of the view that there can be a direction to the petitioner to deposit the maximum penalty of 200% of the tax to safeguard the interest of the revenue.”

| Case Title | Haresh Kumar Vs The Assistant Commissioner (ST) |

| Citation | W.P.No.14628 of 2023 |

| Date | 05.05.2023 |

| Counsel For Appellant | Mr G.Nataraja |

| Counsel For Respondent | Mr C.Harsharaj |

| Madras HC | Read Order |