It was held by the Jharkhand High Court that the Goods and Services Tax ( GST) Input Tax Credit ( ITC ) is permissible even on the late filing of the Goods and Services Return GSTR-3B for the FY 2017-18 while asking for a Refund of Penalty & Interest to the petitioner.

M/s. Ram Constructions, a proprietorship concern that has its place of business at Barkiray, Maheshpur, Pakur, Jharkhand via its Proprietor furnished the existing writ petition for the issuance of a chance writ, order or direction, holding and declaring Section 16(4) of the Central Goods and Services Tax Act, 2017 as ultra vires, since, it asks for restricting the Input Tax Credit claim, within a time frame, which is being a breach of Article 14, Article 19(1)(g) and Article 300A of the Constitution of India and also being the breach of the basic structure of the Goods and Services Tax Act, 2017.

Also, the applicant pleaded for the issuance of an appropriate writ, order, direction, holding and declaring the amendment brought under Rule 61(5) of the Central Goods and Services Rules, 2017 inserted vide Clause 4(a) of Notification No. 49/2019 on 9th October, 2019 issued by Respondent No.-2 Central Board of Indirect Taxes and Customs (Annexure- 5) as ultra vires, through which GSTR-3B has been reported to be a return u/s 39 of the Central Goods and Services Act, 2017 wef 01.07.2017, as being wholly violative of Article 14, Article 19(1)(g) and Article 300A of the Constitution of India as it has the effect of interrupting with the granted right of the applicant to claim the ITC.

Further, the applicant asked for the issuance of a writ, order, or direction like Prohibition, commanding the Respondents, their servants, agents, and subordinates to forbear from providing any effect and acting on the grounds of or in furtherance of the provisions of Section 16(4) of the Act and the regulations made and notifications issued thereunder in any purported proceedings there under and from charging or any tax collection based on that.

Additionally, the issuance of an appropriate writ, order, and direction for quashing and setting aside the order on 31.01.2023 including DRC-07 on 10.10.2023 was even pursued.

After hearing both sides the Jharkhand Bench of Chief Justice marked that according to Clause (5) of Section 16 inserted by the Finance (No.2) Act, 2024, w.e.f 01.07.2017 the respondents are asked to permit the applicant to take the ITC concerning the late returns furnished for the FY 2017-18 and the interest along with the penalty imposed on the applicant via the respondents will be refunded at 6% p.a interest from the date of these collections till the repayment date.

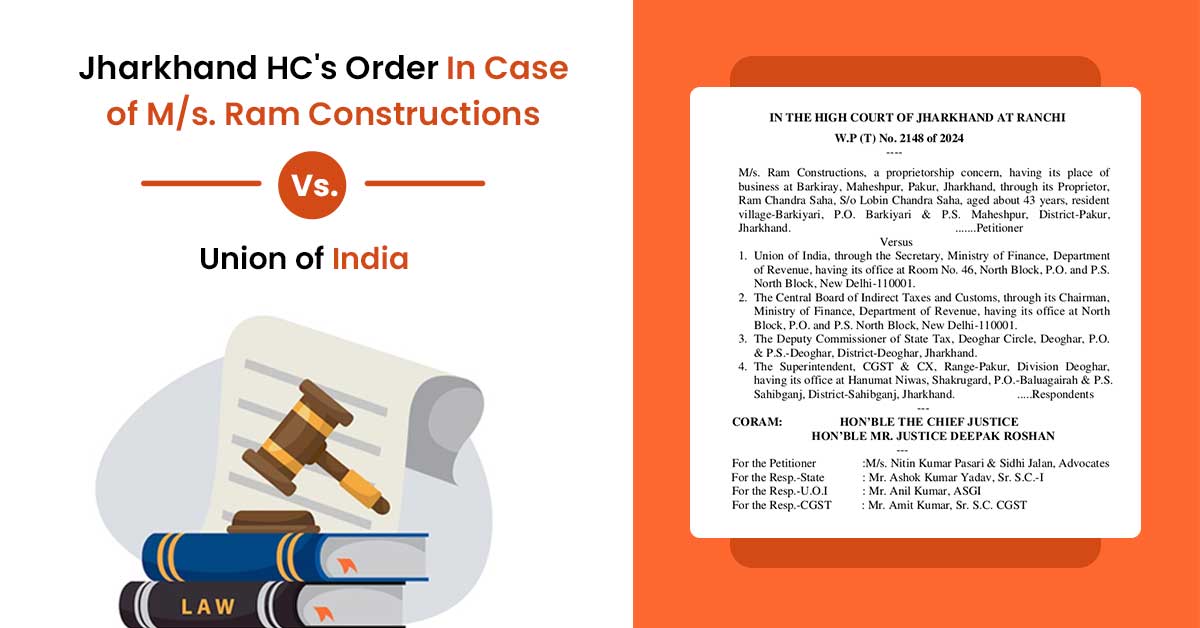

| Case Title | M/s. Ram Constructions Vs. Union of India |

| Citation | W.P (T) No. 2148 of 2024 |

| Date | 07.12.2024 |

| For the Petitioner | Advocates Ankit Kanodia, Megha Agarwal and Jitesh Sah |

| For the Resp.-State | Mr. Ashok Kumar Yadav, Sr. S.C.-I |

| For the Resp.-U.O.I | Mr. Anil Kumar, ASGI |

| For the Resp.-CGST | Mr. Amit Kumar, Sr. S.C. CGST |

| Jharkhand High Court | Read Order |