The Ahmedabad ITAT set aside a partially passed order under section 263 of the IT Act, 1961, where the Principal Commissioner of Income Tax improperly mandated the inclusion of accommodation entries without adequate verification.

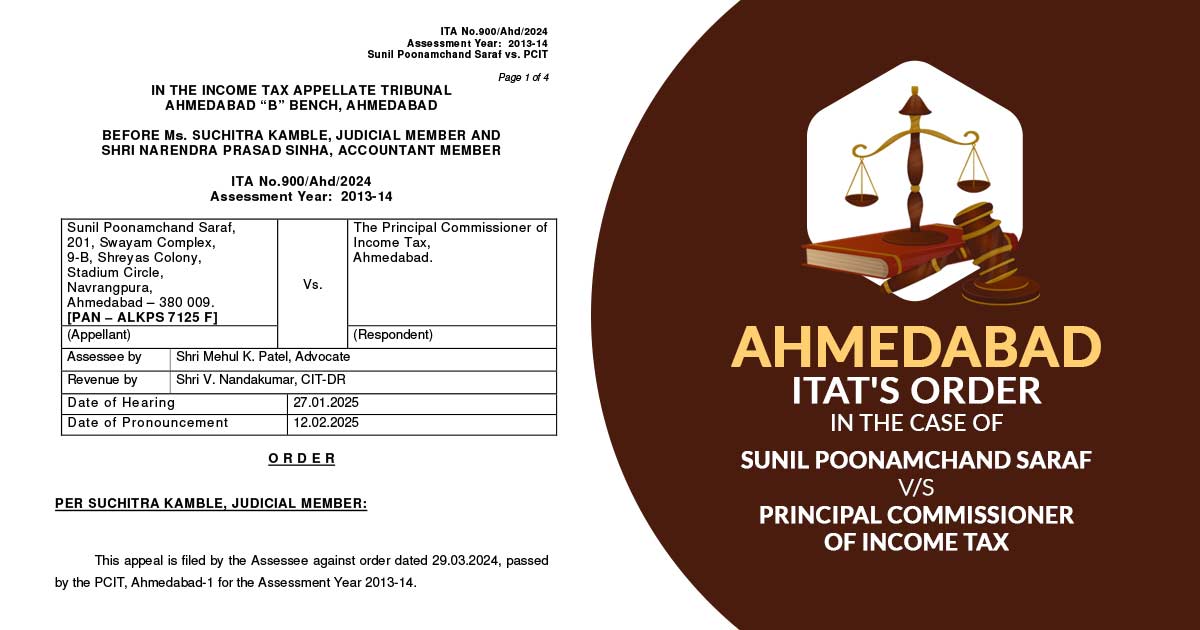

Sunil Poonamchand Saraf, applicant, furnished an appeal against the order passed by the PCIT, Ahmedabad-1, for the AY 2013-14. Originally, the appellant had filed his return of Rs. 1,99,610, which was accepted in an assessment under Section 147 read with Section ection 144B.

Later, the PCIT held that the taxpayer was recognised as an end beneficiary of accommodation entries to Rs. 4,07,97,829 (Rs. 4.07 crore) from Dishman Group.

The PCIT, when discovered that during reassessment no addition was there even after recorded reasons and proofs from the investigation, has furnished a notice u/s 263, setting aside the assessment and asking the assessing officer to file an addition of the alleged accommodation entries.

The taxpayer at the time of the hearing was represented by Mehul K. Patel, who said that the PCIT had violated jurisdiction under section 263 by asking addition rather than only setting aside the order for effective verification.

In reopening proceedings, distinct defects were there, and the taxpayer has provided the proofs before which were not acknowledged sufficiently in the reassessment. The direction of the PCIT terminated the discretion of the assessing officer, which is not allowable u/s 263.

Records and claims were been considered by the ITAT Bench comprising Suchitra Kamble (Judicial Member) and Narendra Prasad Sinha (Accountant Member). The tribunal, due to the absence of an enquiry by the assessing officer for the accommodation entries, PCIT invoked section 263; therefore, the direction to make an addition was not permissible

u/s 263.

The Tribunal, the PCIT, can direct the Assessing Officer to verify and reframe the assessment after an appropriate enquiry, but without examination of facts, it cannot instruct for addition.

Therefore, the part of the order of PCIT has been quashed by the Income Tax Appellate Tribunal (ITAT), which asks the assessing officer to make the addition and keep only the direction to pass a fresh assessment order post verification.

| Case Title | M/s. Sunil Poonamchand Saraf V/S Principal Commissioner of Income Tax |

| Case No. | ITA No.900/Ahd/2024 |

| Counsel For Assessee | Shri Mehul K. Patel, Advocate |

| Counsel For Revenue | Shri V. Nandakumar, CIT-DR |

| ITAT Ahmedabad | Read Order |