In a major shift from VAT to GST, India has supported the new indirect tax regime from the core of its heart and its capabilities. Almost all the traders and taxpayers have tried to comply with the newly incorporated tax scheme and have done whatever the new law has demanded from them. The GST act states that the supplier will be doing payments of GST whenever it supplies goods and services to the recipients.

The reason behind the introduction of reverse charge mechanism was to check the evasion of tax which is practised widely across the nation. In the cases of supply done in an unorganized sector or when the tax collection channels are not appropriately linked mainly goods transport services. As known, the reverse charge mechanism is deferred till March 2018 in the case of supply from an unregistered supplier to a registered dealer.

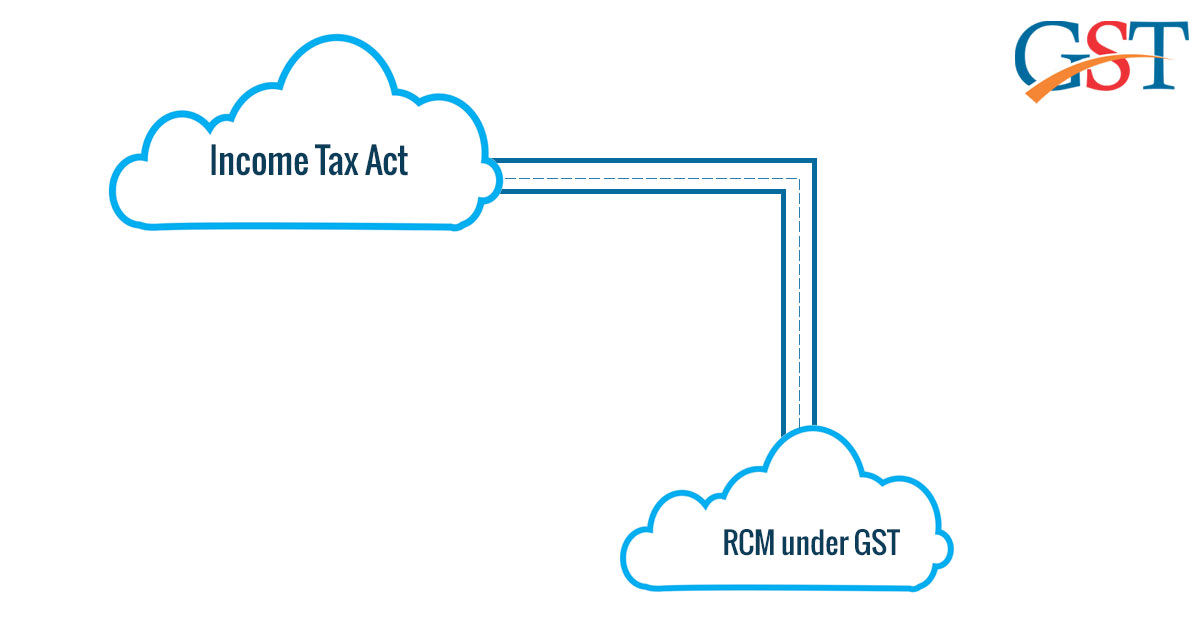

Now why we are discussing the aspects and the turning point of reverse charge mechanism here is that government is trying to figure out all the possibilities to turn reverse charge mechanism more and more strict and compilable. For this, the government also implement the provisions of income tax act which enacts that in case if a taxpayer fails to comply with the TDS provisions than there will be disallowance of expenses.

The provision included in the income tax act requires that the taxes must be deducted at source of generation at a certain percentage fixed by the authorities on the payments like interest, royalty, fees for technical services, commission etc. And in case the taxpayer fails to deduct the tax or fails to submit the taxes, there is a disallowance of taxes on some portion while the other portion can be claimed as a deduction.

Also to notice that the disallowed expense can be claimed further only if the taxpayer complies with the TDS provisions. All these steps are under the income tax act right now providing a measure to check on tax evasion. The same provision may be applicable in the GST reverse charge mechanism stating that an additional measurement will ensure the timely payment of taxes from the parties. The provision is known to be Section 40(a)(ia) which may get introduced in the reverse charge mechanism.