There is various assessee who is seeing the issues and is not able to furnish the CMP and create the challans because of shadowing the negative liability in GST CMP 08 on the GSTN portal.

What Do You Mean by Form GST CMP 08?

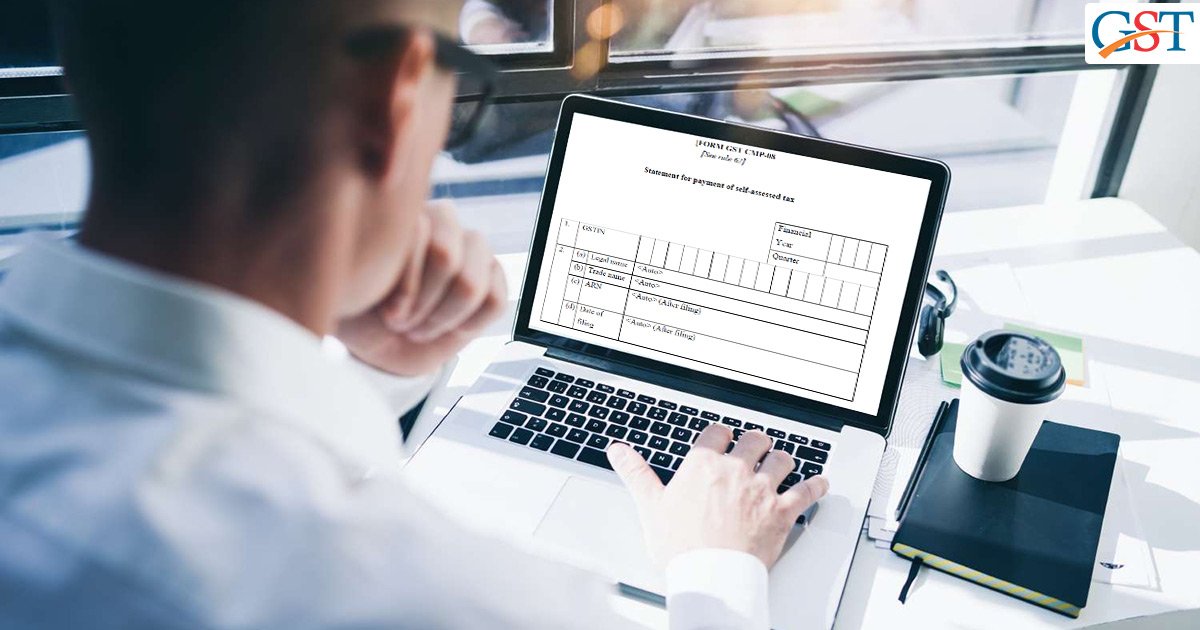

Form GST CMP-08

The assessee who either posses the enrolled as composition taxable individual via Form GST REG 01 or assessee who has chosen the composition levy through Form GST CMP-02 urged to furnish Form GST CMP 08.

Meaning of Negative Liability?

Negative Liability management reveals that any negative entry performed in the present quarter shall be carried forward to the subsequent quarter.

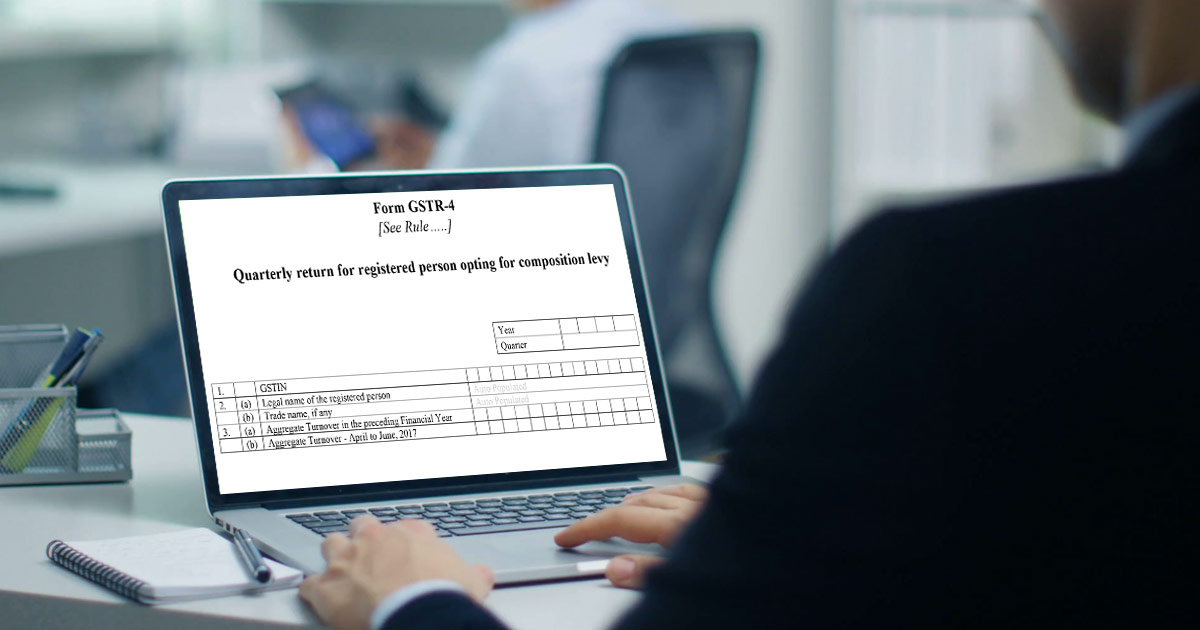

If you had furnished GSTR-4

As a result, the management shall be displayed in the ‘Adjustment of negative liability of past tax period’ Table 4 column of the GSTR-4 next quarter GST CMP-08 filing. Thus the portal is showing that you had furnished the summary of CMP-08 but as the turnover was zero so there is no liability to furnish the tax.

How to Handle the Situation?

According to the law, the assessee who has not given the information of the turnover and the tax furnish in Table No.6 GSTR-4 shall have to furnish the objection then provide in the writing to your jurisdictional officer asking him to eliminate the Negative Liability, which might be time taking. But there are various other methods that are drawn through the experienced people in the market where it is not legally prescribed anywhere:

Cash Payment

The assessee is furnishing the tax in cash by other challan and depositing that in the cash ledger and when they shall urge for that it shall be in writing to the jurisdictional officer for all the scenes that the negative liability will not permit them to file the CMP-08 who has opted this method.

A cash ledger has the deposits which an assessee had build and any GST payments

Furnish via DRC 03 Under GST

DRC-03 is the form beneath the GST law which needs to be furnished for voluntary tax payments for the demand or tax shortfall noticed after some time post to the time limit to furnish the return of the FY expires. CGST Rule 142(2) and (3) include this form.

Boost the Turnover

Individuals are suggesting that you night raise the turnover of the past year.

Extend the Tax Amount

People are recommending that they confer the same turnover but arise the tax amount according to the amount of the negative liability reason being that it will be the negative liability and the assessee is able to furnish the particular tax amount which he needs to furnish.

In 2019-20 I have paid the liability through Form GST CMP-08 then computing GSTR4, liability declared in GST CMP-08 auto-populated in Table 5. thus if nothing is declared in table 6.

and next year 2020-21 in GSTR4, I will take 2 years turnover of 2019-20 + 2020-21 in table 6. at that time cash ledger was cleared. but now from 26/04/2022 onwards cash ledger shows a negative balance. What to do now, please tell me the solution

“Please read the following advisory issued by the GST portal in this regard https://www.gst.gov.in/newsandupdates/read/536“

PLEASE SOLVE PROBLEM

In 2019-20 I have paid the liability through Form GST CMP-08 then computing GSTR4, liability declared in GST CMP-08 auto-populated in Table 5. thus if nothing is declared in table 6.

and next year 2020-21 in GSTR4, I will take 2 years turnover of 2019-20 + 2020-21 in table 6. at that time cash ledger was cleared. but now from 26/04/2022 onwards cash ledger shows a negative balance. What to do now, please tell me the solution

In 2019-20 I have paid the liability through Form GST CMP-08 then computing GSTR4, liability declared in GST CMP-08 auto-populated in Table 5. thus if nothing is declared in table 6.

and next year 2020-21 in GSTR4, I will take 2 years turnover of 2019-20 + 2020-21 in table 6. at that time cash ledger was cleared. but now from 26/04/2022 onwards cash ledger shows a negative balance. What to do now, please tell me the solution

Please read the following advisory issued by GST portal in this regard https://www.gst.gov.in/newsandupdates/read/536

sir, the problem being faced that inability to make payment through cmp08 for the period APR-JUN21 by the composition taxpayer due to negative liability appeared in pay tax column who missed to fill up outward details in table 6 of GSTR4 for the FY 2019-20,2021-21, are directed by some experts to pay cash through the challan of any other payment so that tax due credit to the GST portal and the dealer may explain later OR use DRC03 in order to surrender negative liability OR add the present period tax due with negative liability amount so as to pay present due. I tried the 3rd and filed cmp08 for apr-jun21, Now the ledger shows again the negative liability double of the previous figure.

“Please contact to GST practitioner for the same”