The Gujarat authority upon an advance ruling for goods and services tax GST specified that the owners did not require to furnish GST on electricity or the charges taken from the tenants moreover, in addition, as the value of supply as per the lease agreement of immovable property rent.

Gujarat AAR has been approached by Gujarat Narmada Valley Fertilizers Chemicals Ltd upon the concern that if the electricity dues paid through the owners to electricity supply firms for the electricity connection in the owner’s name and bills will be recovered depends on submeters varied distinct tenants must contemplate the amount redeemed as a pure agent of the tenant.

If you have furnished an expense towards the customer’s to provide services then beneath the pure agent concept one doesn’t need to furnish GST (Goods and Services Tax) on the amount that you take upon and the above the payments.

“The applicant has cast an onus on the lessee to pay the charges in respect of the electric power used by them directly to the electricity company-it cannot be said that the electricity charges would be covered by Sec. 15(2)(c) of the CGST Act, 2017 for the sole reason that the rate for renting of premises has been fixed at an amount and the electricity charges are to be borne by the lessee as per the actual usage of electric power by them in terms of the agreement.”

AAR also sees that the petitioner subjected as a pure agent. “Electricity charges collected by the landlord from the tenant at actuals based on the reading of the sub-meters are covered under the amount recovered as a pure agent in terms of the provisions of Rule 33 of the CGST Rules, 2017

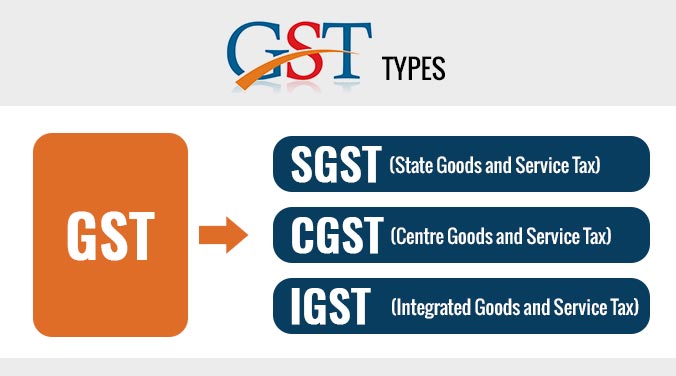

Get the brief introduction of SGST, IGST and CGST. We have mentioned their full forms, meanings and adjustments of input tax credit under GST in India in respect of the lessor – the decision would apply only in respect of the agreement under discussion and analogy of this decision would not be applicable to a different set of circumstances.”

“Hopefully, this ruling would be sagacious enough to attract the eyes of taxpayers and the authorities, as the reasoning provided for non-applicability of GST on electricity appears to be cogent.”